Advertisement

- Taiwan

- /

- Semiconductors

- /

- TPEX:6182

Wafer Works Corporation's (GTSM:6182) Stock On An Uptrend: Could Fundamentals Be Driving The Momentum?

Wafer Works (GTSM:6182) has had a great run on the share market with its stock up by a significant 14% over the last month. As most would know, fundamentals are what usually guide market price movements over the long-term, so we decided to look at the company's key financial indicators today to determine if they have any role to play in the recent price movement. Specifically, we decided to study Wafer Works' ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

Check out our latest analysis for Wafer Works

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Wafer Works is:

5.1% = NT$646m ÷ NT$13b (Based on the trailing twelve months to September 2020).

The 'return' is the yearly profit. Another way to think of that is that for every NT$1 worth of equity, the company was able to earn NT$0.05 in profit.

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

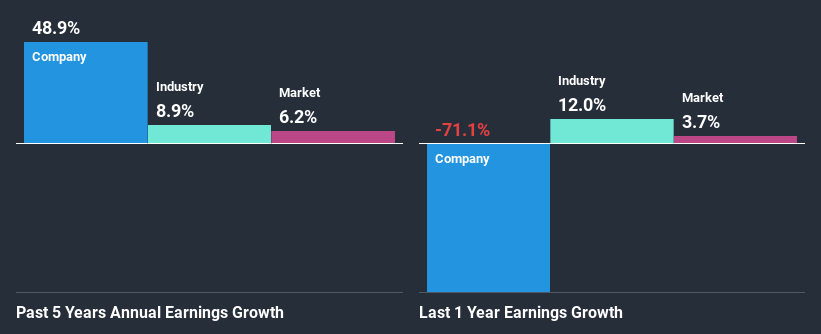

Wafer Works' Earnings Growth And 5.1% ROE

When you first look at it, Wafer Works' ROE doesn't look that attractive. We then compared the company's ROE to the broader industry and were disappointed to see that the ROE is lower than the industry average of 11%. However, we we're pleasantly surprised to see that Wafer Works grew its net income at a significant rate of 49% in the last five years. Therefore, there could be other reasons behind this growth. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

As a next step, we compared Wafer Works' net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 8.9%.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. If you're wondering about Wafer Works''s valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Wafer Works Making Efficient Use Of Its Profits?

Wafer Works has a significant three-year median payout ratio of 64%, meaning the company only retains 36% of its income. This implies that the company has been able to achieve high earnings growth despite returning most of its profits to shareholders.

Moreover, Wafer Works is determined to keep sharing its profits with shareholders which we infer from its long history of nine years of paying a dividend. Existing analyst estimates suggest that the company's future payout ratio is expected to drop to 7.1% over the next three years. The fact that the company's ROE is expected to rise to 19% over the same period is explained by the drop in the payout ratio.

Summary

Overall, we feel that Wafer Works certainly does have some positive factors to consider. That is, quite an impressive growth in earnings. However, the low profit retention means that the company's earnings growth could have been higher, had it been reinvesting a higher portion of its profits. So far, we've only made a quick discussion around the company's earnings growth. To gain further insights into Wafer Works' past profit growth, check out this visualization of past earnings, revenue and cash flows.

If you’re looking to trade Wafer Works, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Wafer Works might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TPEX:6182

Wafer Works

Engages in the research, design, development, manufacturing, trading, and distribution of semiconductor materials in Taiwan, Mainland China, the United States, and Internationally.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor