- Taiwan

- /

- Specialty Stores

- /

- TWSE:2207

These 4 Measures Indicate That Hotai MotorLtd (TPE:2207) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Hotai Motor Co.,Ltd. (TPE:2207) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Hotai MotorLtd

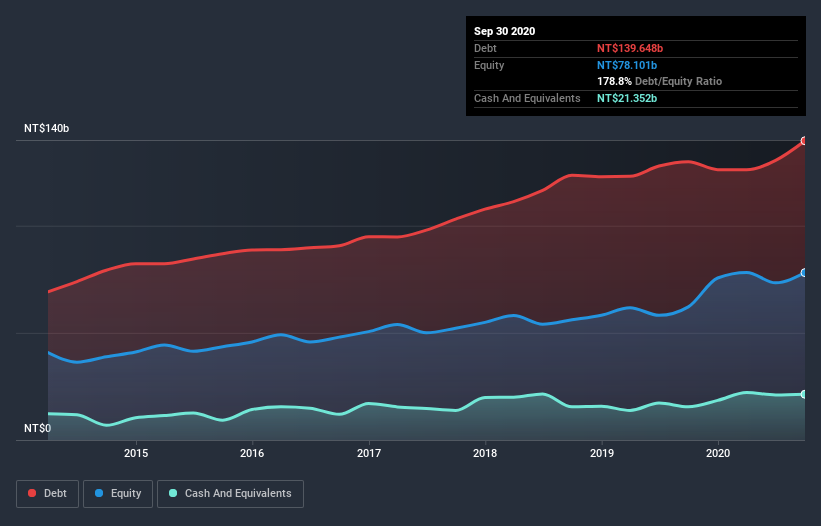

What Is Hotai MotorLtd's Net Debt?

The image below, which you can click on for greater detail, shows that at September 2020 Hotai MotorLtd had debt of NT$139.6b, up from NT$129.8b in one year. However, because it has a cash reserve of NT$21.4b, its net debt is less, at about NT$118.3b.

How Healthy Is Hotai MotorLtd's Balance Sheet?

According to the last reported balance sheet, Hotai MotorLtd had liabilities of NT$172.1b due within 12 months, and liabilities of NT$21.1b due beyond 12 months. Offsetting this, it had NT$21.4b in cash and NT$146.3b in receivables that were due within 12 months. So it has liabilities totalling NT$25.7b more than its cash and near-term receivables, combined.

Since publicly traded Hotai MotorLtd shares are worth a very impressive total of NT$322.8b, it seems unlikely that this level of liabilities would be a major threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Hotai MotorLtd's net debt is 3.9 times its EBITDA, which is a significant but still reasonable amount of leverage. But its EBIT was about 11.2 times its interest expense, implying the company isn't really paying a high cost to maintain that level of debt. Even were the low cost to prove unsustainable, that is a good sign. If Hotai MotorLtd can keep growing EBIT at last year's rate of 16% over the last year, then it will find its debt load easier to manage. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Hotai MotorLtd's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Considering the last three years, Hotai MotorLtd actually recorded a cash outflow, overall. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

When it comes to the balance sheet, the standout positive for Hotai MotorLtd was the fact that it seems able to cover its interest expense with its EBIT confidently. However, our other observations weren't so heartening. In particular, conversion of EBIT to free cash flow gives us cold feet. When we consider all the factors mentioned above, we do feel a bit cautious about Hotai MotorLtd's use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 1 warning sign with Hotai MotorLtd , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

When trading Hotai MotorLtd or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Hotai MotorLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:2207

Hotai MotorLtd

Hotai Motor Co.,Ltd., together with its subsidiaries, exports and imports, trades, and sells vehicles, automobile air conditioners, and related parts in Taiwan and Mainland China.

Mediocre balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Community Narratives