- Taiwan

- /

- Basic Materials

- /

- TWSE:2504

Declining Stock and Solid Fundamentals: Is The Market Wrong About Goldsun Building Materials Co., Ltd. (TWSE:2504)?

It is hard to get excited after looking at Goldsun Building Materials' (TWSE:2504) recent performance, when its stock has declined 18% over the past three months. But if you pay close attention, you might gather that its strong financials could mean that the stock could potentially see an increase in value in the long-term, given how markets usually reward companies with good financial health. In this article, we decided to focus on Goldsun Building Materials' ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

How Do You Calculate Return On Equity?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Goldsun Building Materials is:

17% = NT$4.6b ÷ NT$28b (Based on the trailing twelve months to December 2024).

The 'return' is the amount earned after tax over the last twelve months. Another way to think of that is that for every NT$1 worth of equity, the company was able to earn NT$0.17 in profit.

See our latest analysis for Goldsun Building Materials

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

A Side By Side comparison of Goldsun Building Materials' Earnings Growth And 17% ROE

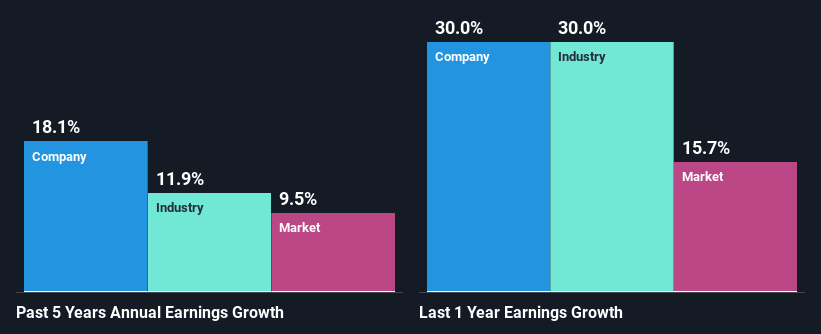

To start with, Goldsun Building Materials' ROE looks acceptable. Especially when compared to the industry average of 6.3% the company's ROE looks pretty impressive. This probably laid the ground for Goldsun Building Materials' moderate 18% net income growth seen over the past five years.

We then compared Goldsun Building Materials' net income growth with the industry and we're pleased to see that the company's growth figure is higher when compared with the industry which has a growth rate of 12% in the same 5-year period.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. Is Goldsun Building Materials fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Goldsun Building Materials Making Efficient Use Of Its Profits?

Goldsun Building Materials has a significant three-year median payout ratio of 70%, meaning that it is left with only 30% to reinvest into its business. This implies that the company has been able to achieve decent earnings growth despite returning most of its profits to shareholders.

Additionally, Goldsun Building Materials has paid dividends over a period of at least ten years which means that the company is pretty serious about sharing its profits with shareholders. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 75%. Regardless, Goldsun Building Materials' ROE is speculated to decline to 13% despite there being no anticipated change in its payout ratio.

Summary

Overall, we are quite pleased with Goldsun Building Materials' performance. In particular, its high ROE is quite noteworthy and also the probable explanation behind its considerable earnings growth. Yet, the company is retaining a small portion of its profits. Which means that the company has been able to grow its earnings in spite of it, so that's not too bad. Having said that, on studying current analyst estimates, we were concerned to see that while the company has grown its earnings in the past, analysts expect its earnings to shrink in the future. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you're looking to trade Goldsun Building Materials, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:2504

Goldsun Building Materials

Engages in the production and sale of premixed concrete, cement, and calcium silicate board in Taiwan and Mainland China.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Community Narratives