Ho Tung Chemical's (TWSE:1714) Shareholders Have More To Worry About Than Only Soft Earnings

The subdued market reaction suggests that Ho Tung Chemical Corp.'s (TWSE:1714) recent earnings didn't contain any surprises. We think that investors are worried about some weaknesses underlying the earnings.

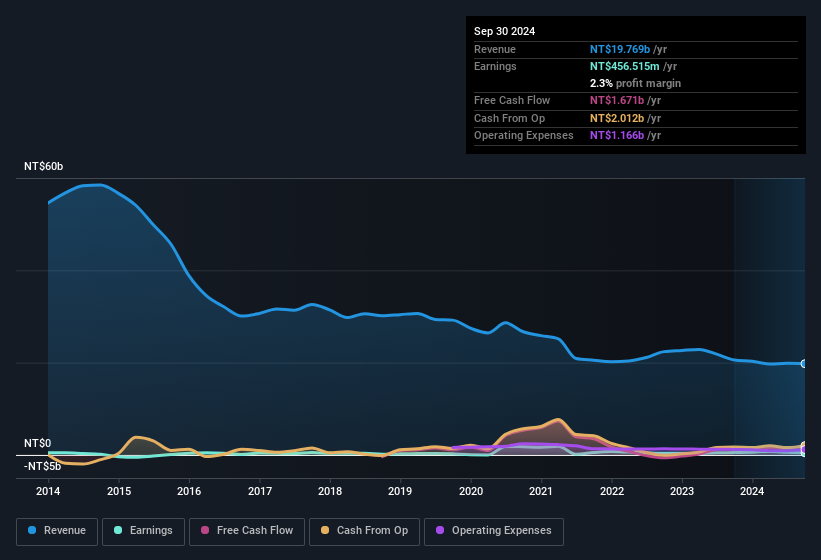

See our latest analysis for Ho Tung Chemical

Zooming In On Ho Tung Chemical's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. The ratio shows us how much a company's profit exceeds its FCF.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

For the year to September 2024, Ho Tung Chemical had an accrual ratio of -0.10. That indicates that its free cash flow was a fair bit more than its statutory profit. Indeed, in the last twelve months it reported free cash flow of NT$1.7b, well over the NT$456.5m it reported in profit. Ho Tung Chemical shareholders are no doubt pleased that free cash flow improved over the last twelve months. However, that's not all there is to consider. We can see that unusual items have impacted its statutory profit, and therefore the accrual ratio.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Ho Tung Chemical.

The Impact Of Unusual Items On Profit

Surprisingly, given Ho Tung Chemical's accrual ratio implied strong cash conversion, its paper profit was actually boosted by NT$224m in unusual items. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. Which is hardly surprising, given the name. Ho Tung Chemical had a rather significant contribution from unusual items relative to its profit to September 2024. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

Our Take On Ho Tung Chemical's Profit Performance

In conclusion, Ho Tung Chemical's accrual ratio suggests its statutory earnings are of good quality, but on the other hand the profits were boosted by unusual items. Having considered these factors, we don't think Ho Tung Chemical's statutory profits give an overly harsh view of the business. If you'd like to know more about Ho Tung Chemical as a business, it's important to be aware of any risks it's facing. To that end, you should learn about the 3 warning signs we've spotted with Ho Tung Chemical (including 1 which shouldn't be ignored).

Our examination of Ho Tung Chemical has focussed on certain factors that can make its earnings look better than they are. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

Valuation is complex, but we're here to simplify it.

Discover if Ho Tung Chemical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:1714

Ho Tung Chemical

Develops, manufactures, processes, and sells various chemical products in Taiwan, China, Southeast Asia, and internationally.

Flawless balance sheet and good value.