Advertisement

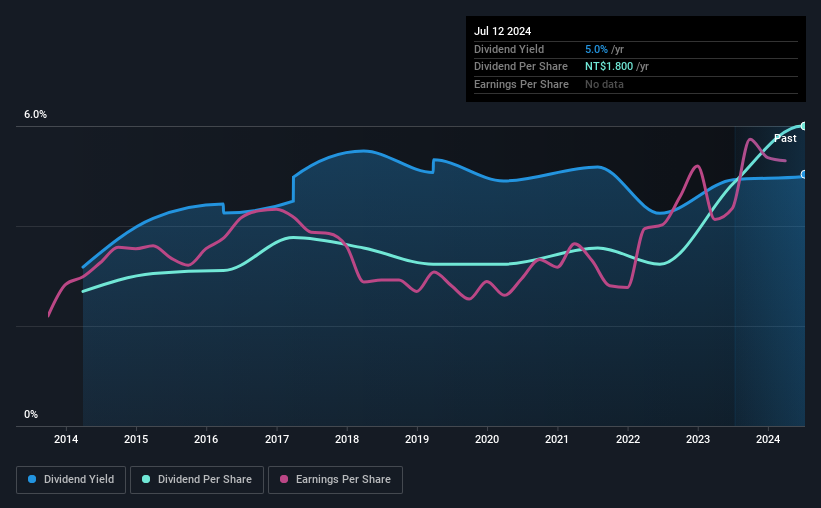

Universal Cement Corporation's (TWSE:1104) dividend will be increasing from last year's payment of the same period to NT$1.80 on 21st of August. This makes the dividend yield 5.0%, which is above the industry average.

Check out our latest analysis for Universal Cement

Universal Cement's Payment Has Solid Earnings Coverage

A big dividend yield for a few years doesn't mean much if it can't be sustained. Universal Cement was earning enough to cover the previous dividend, but it was paying out quite a large proportion of its free cash flows. By paying out so much of its cash flows, this could indicate that the company has limited opportunities for investment and growth.

If the trend of the last few years continues, EPS will grow by 11.5% over the next 12 months. If the dividend continues on this path, the payout ratio could be 55% by next year, which we think can be pretty sustainable going forward.

Universal Cement Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. The dividend has gone from an annual total of NT$0.807 in 2014 to the most recent total annual payment of NT$1.80. This implies that the company grew its distributions at a yearly rate of about 8.3% over that duration. The dividend has been growing very nicely for a number of years, and has given its shareholders some nice income in their portfolios.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. It's encouraging to see that Universal Cement has been growing its earnings per share at 11% a year over the past five years. Earnings are on the uptrend, and it is only paying a small portion of those earnings to shareholders.

In Summary

Overall, this is a reasonable dividend, and it being raised is an added bonus. On the plus side, the dividend looks sustainable by most measures but it is let down by the lack of cash flows. This looks like it could be a good dividend stock going forward, but we would note that the payout ratio has been at higher levels in the past so it could happen again.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 1 warning sign for Universal Cement that investors should take into consideration. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:1104

Universal Cement

Manufactures and sells cement, ready-mixed concrete, gypsum board panels, and other building materials in Taiwan.

Flawless balance sheet 6 star dividend payer.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor