Advertisement

Know This Before Buying China Petrochemical Development Corporation (TPE:1314) For Its Dividend

Could China Petrochemical Development Corporation (TPE:1314) be an attractive dividend share to own for the long haul? Investors are often drawn to strong companies with the idea of reinvesting the dividends. Unfortunately, it's common for investors to be enticed in by the seemingly attractive yield, and lose money when the company has to cut its dividend payments.

A high yield and a long history of paying dividends is an appealing combination for China Petrochemical Development. It would not be a surprise to discover that many investors buy it for the dividends. Some simple research can reduce the risk of buying China Petrochemical Development for its dividend - read on to learn more.

Explore this interactive chart for our latest analysis on China Petrochemical Development!

Payout ratios

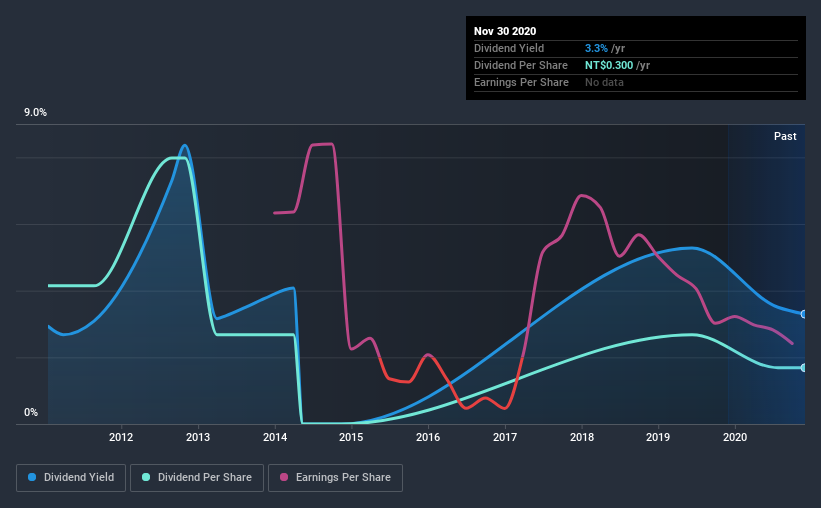

Dividends are usually paid out of company earnings. If a company is paying more than it earns, then the dividend might become unsustainable - hardly an ideal situation. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. In the last year, China Petrochemical Development paid out 145% of its profit as dividends. Unless there are extenuating circumstances, from the perspective of an investor who hopes to own the company for many years, a payout ratio of above 100% is definitely a concern.

We also measure dividends paid against a company's levered free cash flow, to see if enough cash was generated to cover the dividend. Unfortunately, while China Petrochemical Development pays a dividend, it also reported negative free cash flow last year. While there may be a good reason for this, it's not ideal from a dividend perspective.

Consider getting our latest analysis on China Petrochemical Development's financial position here.

Dividend Volatility

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. For the purpose of this article, we only scrutinise the last decade of China Petrochemical Development's dividend payments. The dividend has been cut on at least one occasion historically. During the past 10-year period, the first annual payment was NT$0.7 in 2010, compared to NT$0.3 last year. This works out to be a decline of approximately 8.6% per year over that time. China Petrochemical Development's dividend hasn't shrunk linearly at 8.6% per annum, but the CAGR is a useful estimate of the historical rate of change.

When a company's per-share dividend falls we question if this reflects poorly on either external business conditions, or the company's capital allocation decisions. Either way, we find it hard to get excited about a company with a declining dividend.

Dividend Growth Potential

With a relatively unstable dividend, and a poor history of shrinking dividends, it's even more important to see if EPS are growing. It's good to see China Petrochemical Development has been growing its earnings per share at 11% a year over the past five years. Paying out more in dividends than was reported as profit can make sense in some cases, we would be inclined to avoid a company doing this, unless there were a solid reason.

We'd also point out that China Petrochemical Development issued a meaningful number of new shares in the past year. Regularly issuing new shares can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

Conclusion

To summarise, shareholders should always check that China Petrochemical Development's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. China Petrochemical Development paid out almost all of its cash flow and profit as dividends, leaving little to reinvest in the business. We were also glad to see it growing earnings, but it was concerning to see the dividend has been cut at least once in the past. In summary, China Petrochemical Development has a number of shortcomings that we'd find it hard to get past. Things could change, but we think there are likely more attractive alternatives out there.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. To that end, China Petrochemical Development has 3 warning signs (and 1 which is concerning) we think you should know about.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

If you’re looking to trade China Petrochemical Development, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TWSE:1314

China Petrochemical Development

Produces and sells petrochemical intermediates and related engineering plastics, synthetic resins, chemical fiber, and other derivative products in Taiwan, rest of Asia, and internationally.

Mediocre balance sheet low.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor