Advertisement

- Taiwan

- /

- Medical Equipment

- /

- TWSE:4771

Market Participants Recognise Vizionfocus Inc.'s (TWSE:4771) Earnings Pushing Shares 29% Higher

Vizionfocus Inc. (TWSE:4771) shares have continued their recent momentum with a 29% gain in the last month alone. The annual gain comes to 127% following the latest surge, making investors sit up and take notice.

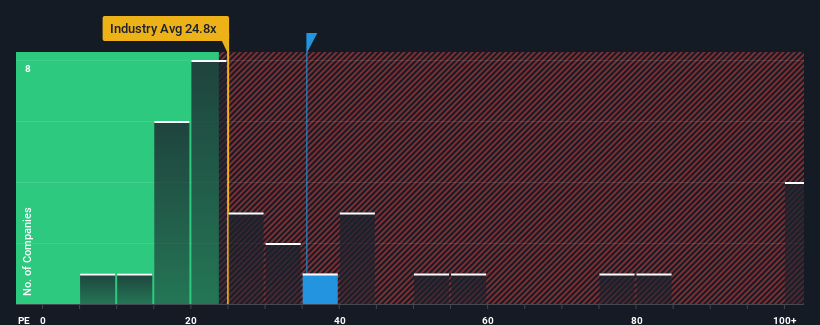

Following the firm bounce in price, Vizionfocus may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 35.5x, since almost half of all companies in Taiwan have P/E ratios under 22x and even P/E's lower than 15x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

Vizionfocus certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for Vizionfocus

How Is Vizionfocus' Growth Trending?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Vizionfocus' to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 79% last year. The strong recent performance means it was also able to grow EPS by 265% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 40% during the coming year according to the only analyst following the company. Meanwhile, the rest of the market is forecast to only expand by 25%, which is noticeably less attractive.

With this information, we can see why Vizionfocus is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Vizionfocus' P/E?

Shares in Vizionfocus have built up some good momentum lately, which has really inflated its P/E. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Vizionfocus' analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Before you take the next step, you should know about the 1 warning sign for Vizionfocus that we have uncovered.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:4771

Vizionfocus

Engages in the manufacturing of medical equipment in Taiwan, China, Japan, and the United States.

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor