- China

- /

- Life Sciences

- /

- SHSE:688621

Uncovering Beijing Sun-Novo Pharmaceutical Research And 2 Other Promising Small Caps With Growth Potential

Reviewed by Simply Wall St

In a week marked by cautious sentiment following the Federal Reserve's rate cut and tempered expectations for future reductions, small-cap stocks have faced notable challenges, with indices like the S&P 600 experiencing significant declines. Despite these headwinds, strong economic indicators such as robust consumer spending and job growth offer a backdrop of resilience that can be promising for small-cap companies poised to capitalize on niche markets or innovative solutions. In this environment, identifying potential growth opportunities often involves looking beyond immediate market volatility to find companies with unique value propositions or strategic positioning. This article explores three such small-cap stocks, including Beijing Sun-Novo Pharmaceutical Research, which may hold promise in navigating the current economic landscape.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Lion Rock Group | 16.91% | 14.33% | 10.15% | ★★★★★★ |

| Mildef Crete | NA | 0.93% | 9.96% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Forest Packaging GroupLtd | 17.72% | 2.87% | -6.03% | ★★★★★★ |

| Nofoth Food Products | NA | 14.41% | 31.88% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| PBA Holdings Bhd | 1.86% | 7.41% | 40.17% | ★★★★★☆ |

| Lee's Pharmaceutical Holdings | 14.22% | -1.39% | -14.93% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Waja | 23.81% | 98.44% | 14.54% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

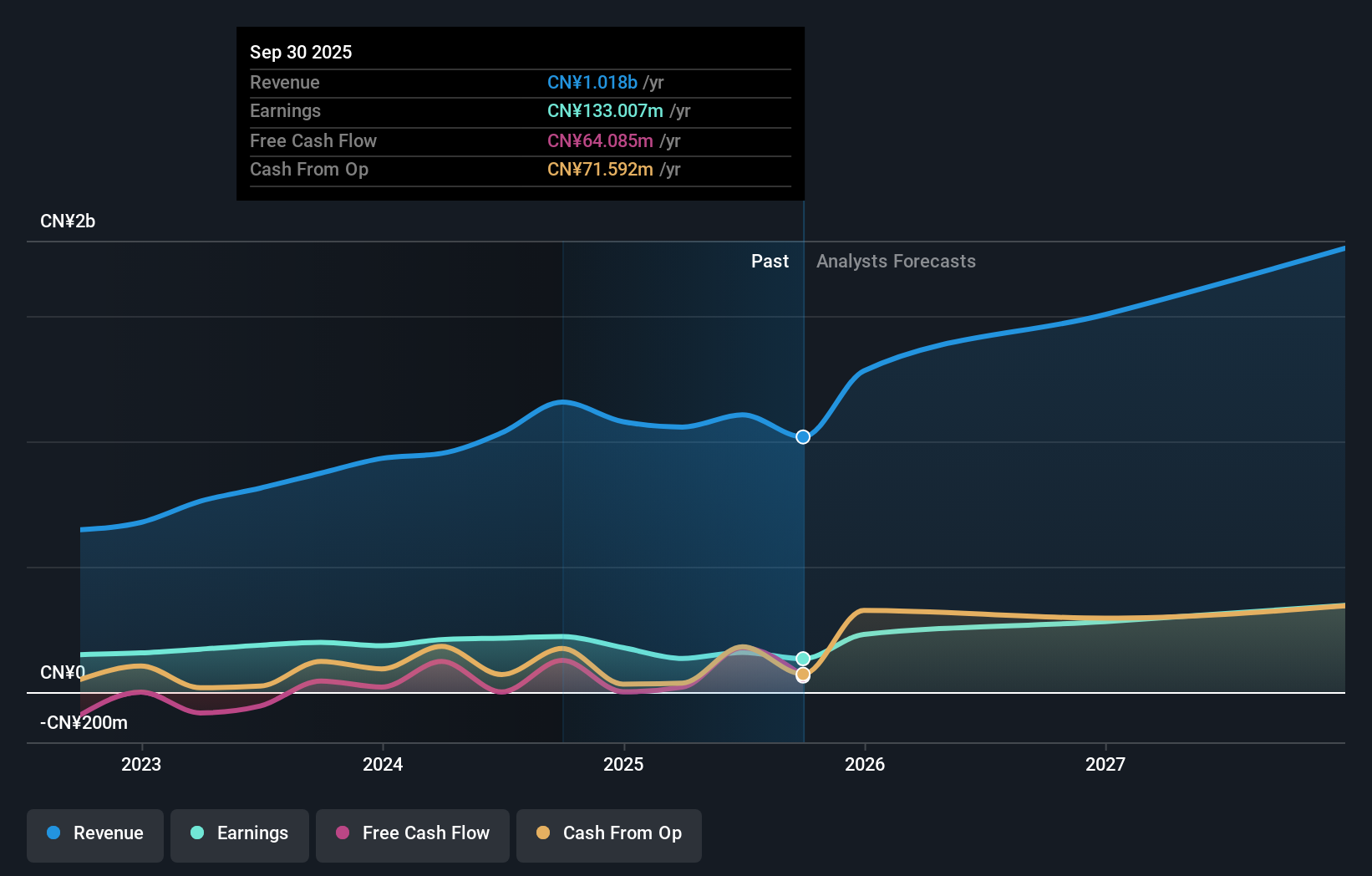

Beijing Sun-Novo Pharmaceutical Research (SHSE:688621)

Simply Wall St Value Rating: ★★★★★☆

Overview: Beijing Sun-Novo Pharmaceutical Research Co., Ltd. is a contract research company focused on drug research and development in China, with a market cap of CN¥4.37 billion.

Operations: Sun-Novo Pharmaceutical generates revenue primarily from its contract research services in drug development. The company's net profit margin has consistently shown an upward trend, reaching a notable percentage over recent periods.

Beijing Sun-Novo Pharmaceutical Research, a smaller player in the pharmaceutical sector, has shown promising financial health with earnings increasing by 11.4% over the past year, outpacing the Life Sciences industry. The company's price-to-earnings ratio of 20.4x is below the CN market average of 35.3x, suggesting potential value for investors. Despite an increased debt-to-equity ratio from 9.3% to 41.3% over five years, it holds more cash than total debt and maintains high-quality earnings. Recently announced share repurchase plans worth up to CNY100 million further underline its strategic initiatives to enhance shareholder value through employee incentives and stock ownership plans.

Compucase Enterprise (TWSE:3032)

Simply Wall St Value Rating: ★★★★★★

Overview: Compucase Enterprise Co., Ltd. is a global designer and manufacturer of PC cases, power supplies, rackmount chassis, and cabinets with a market capitalization of NT$10.55 billion.

Operations: Compucase Enterprise generates revenue primarily from its Operation Headquarters, Server Casing Segment, and Manufacturing, with the Operation Headquarters contributing NT$5.88 billion. The company faces an adjustment and write-off of NT$8.21 billion impacting overall financials. Notably, the Medical Equipment Segment adds NT$479.87 million to its revenue streams.

Compucase Enterprise, with a market presence that often flies under the radar, recently reported a mixed bag of financial results. November 2024 saw an 8% revenue bump to TWD 720.13 million compared to last year, yet January-November figures showed a 9% dip from the previous year. The third quarter reflected challenges with sales at TWD 1,632.08 million and net income at TWD 69.93 million, both lower than the prior year's figures of TWD 2,067.97 million and TWD 181.43 million respectively. Despite high-quality past earnings and positive free cash flow standing at over TWD 1 billion in recent quarters, Compucase's share price has been highly volatile recently while trading below its estimated fair value by about one-third suggests potential undervaluation opportunities for investors keeping an eye on this tech player amidst industry dynamics where its growth rate lags behind broader trends.

- Unlock comprehensive insights into our analysis of Compucase Enterprise stock in this health report.

Understand Compucase Enterprise's track record by examining our Past report.

LINE Pay Taiwan (TWSE:7722)

Simply Wall St Value Rating: ★★★★★★

Overview: LINE Pay Taiwan Limited operates in the third-party payment sector in Taiwan with a market capitalization of NT$26.34 billion.

Operations: The company generates revenue primarily from data processing, amounting to NT$5.88 billion.

LINE Pay Taiwan, a nimble player in the financial sector, has demonstrated robust earnings growth of 26% over the past year, outpacing the industry average of 19%. The company remains debt-free, which enhances its financial stability and positions it well for future expansion. Despite experiencing a volatile share price recently, LINE Pay Taiwan's high-quality earnings provide confidence in its operational strength. Recent earnings announcements revealed sales of TWD 1.59 billion for Q3 2024, up from TWD 1.23 billion last year, though net income dipped slightly to TWD 112 million from TWD 133 million previously.

- Take a closer look at LINE Pay Taiwan's potential here in our health report.

Examine LINE Pay Taiwan's past performance report to understand how it has performed in the past.

Next Steps

- Access the full spectrum of 4632 Undiscovered Gems With Strong Fundamentals by clicking on this link.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Sun-Novo Pharmaceutical Research might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688621

Beijing Sun-Novo Pharmaceutical Research

A contract research company, engages in the research and development of drugs in China.

Excellent balance sheet with acceptable track record.