- Taiwan

- /

- Hospitality

- /

- TWSE:2739

We Think My Humble House Hospitality Management Consulting's (TPE:2739) Statutory Profit Might Understate Its Earnings Potential

Many investors consider it preferable to invest in profitable companies over unprofitable ones, because profitability suggests a business is sustainable. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. This article will consider whether My Humble House Hospitality Management Consulting's (TPE:2739) statutory profits are a good guide to its underlying earnings.

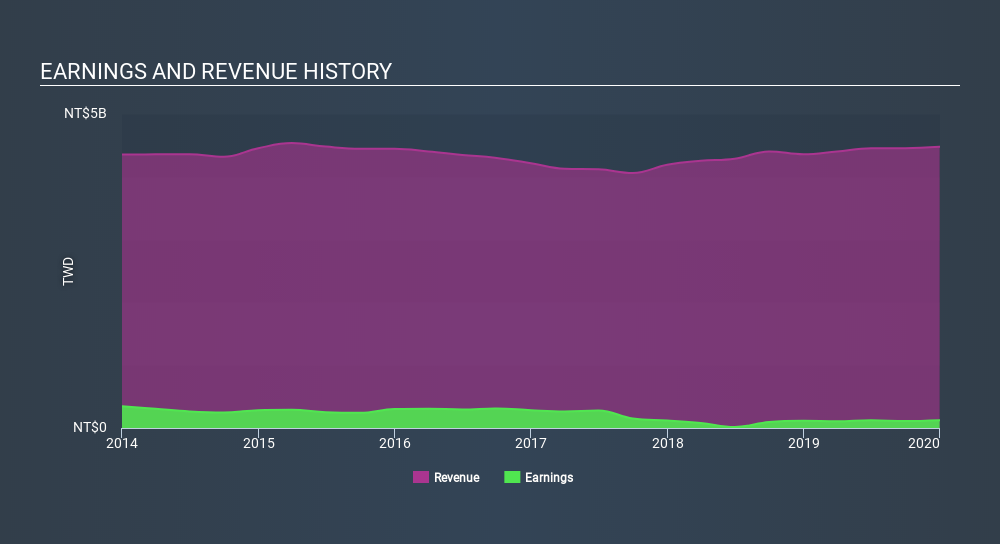

We like the fact that My Humble House Hospitality Management Consulting made a profit of NT$123.4m on its revenue of NT$4.48b, in the last year. The chart below shows how it has grown revenue over the last three years, but that profit has declined.

Check out our latest analysis for My Humble House Hospitality Management Consulting

Not all profits are equal, and we can learn more about the nature of a company's past profitability by diving deeper into the financial statements. Today, we'll discuss My Humble House Hospitality Management Consulting's free cashflow relative to its earnings, and consider what that tells us about the company. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of My Humble House Hospitality Management Consulting.

Zooming In On My Humble House Hospitality Management Consulting's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

For the year to December 2019, My Humble House Hospitality Management Consulting had an accrual ratio of -0.56. That indicates that its free cash flow quite significantly exceeded its statutory profit. Indeed, in the last twelve months it reported free cash flow of NT$862m, well over the NT$123.4m it reported in profit. Given that My Humble House Hospitality Management Consulting had negative free cash flow in the prior corresponding period, the trailing twelve month resul of NT$862m would seem to be a step in the right direction.

Our Take On My Humble House Hospitality Management Consulting's Profit Performance

As we discussed above, My Humble House Hospitality Management Consulting's accrual ratio indicates strong conversion of profit to free cash flow, which is a positive for the company. Because of this, we think My Humble House Hospitality Management Consulting's underlying earnings potential is as good as, or possibly even better, than the statutory profit makes it seem! And the EPS is up 8.6% over the last twelve months. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. When we did our research, we found 3 warning signs for My Humble House Hospitality Management Consulting (1 is concerning!) that we believe deserve your full attention.

Today we've zoomed in on a single data point to better understand the nature of My Humble House Hospitality Management Consulting's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TWSE:2739

My Humble House Hospitality Management Consulting

My Humble House Hospitality Management Consulting Co., Ltd.

Undervalued with solid track record.