There's Reason For Concern Over Bonny Worldwide Limited's (TWSE:8467) Massive 27% Price Jump

Despite an already strong run, Bonny Worldwide Limited (TWSE:8467) shares have been powering on, with a gain of 27% in the last thirty days. The annual gain comes to 271% following the latest surge, making investors sit up and take notice.

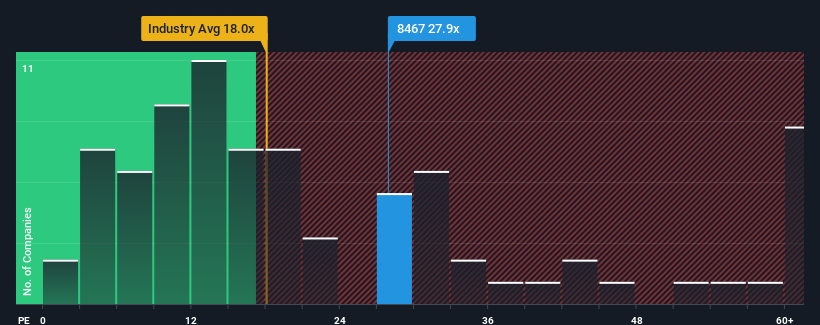

Following the firm bounce in price, given around half the companies in Taiwan have price-to-earnings ratios (or "P/E's") below 20x, you may consider Bonny Worldwide as a stock to potentially avoid with its 27.9x P/E ratio. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Recent times have been quite advantageous for Bonny Worldwide as its earnings have been rising very briskly. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. If not, then existing shareholders might be a little nervous about the viability of the share price.

See our latest analysis for Bonny Worldwide

Does Growth Match The High P/E?

In order to justify its P/E ratio, Bonny Worldwide would need to produce impressive growth in excess of the market.

If we review the last year of earnings growth, the company posted a terrific increase of 42%. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Comparing that to the market, which is predicted to deliver 24% growth in the next 12 months, the company's momentum is weaker based on recent medium-term annualised earnings results.

In light of this, it's alarming that Bonny Worldwide's P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with recent growth rates.

The Bottom Line On Bonny Worldwide's P/E

Bonny Worldwide's P/E is getting right up there since its shares have risen strongly. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Bonny Worldwide currently trades on a much higher than expected P/E since its recent three-year growth is lower than the wider market forecast. When we see weak earnings with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Bonny Worldwide (of which 1 is a bit concerning!) you should know about.

If you're unsure about the strength of Bonny Worldwide's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Bonny Worldwide might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:8467

Bonny Worldwide

Engages in the manufacture and sale of OEM and ODM carbon fiber rackets and related sporting goods.

Outstanding track record with flawless balance sheet.

Market Insights

Community Narratives