Advertisement

Does KMC (Kuei Meng) International (TWSE:5306) Have A Healthy Balance Sheet?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies KMC (Kuei Meng) International Inc. (TWSE:5306) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for KMC (Kuei Meng) International

What Is KMC (Kuei Meng) International's Net Debt?

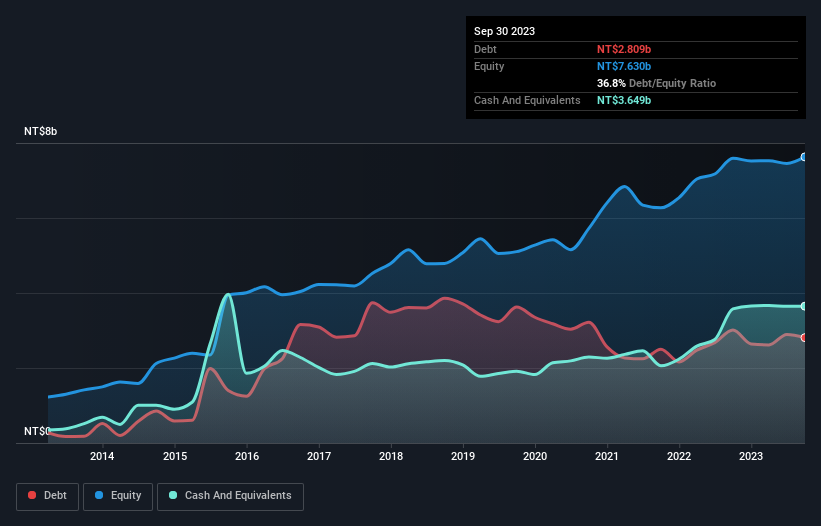

You can click the graphic below for the historical numbers, but it shows that KMC (Kuei Meng) International had NT$2.81b of debt in September 2023, down from NT$3.01b, one year before. But on the other hand it also has NT$3.65b in cash, leading to a NT$839.5m net cash position.

How Strong Is KMC (Kuei Meng) International's Balance Sheet?

According to the last reported balance sheet, KMC (Kuei Meng) International had liabilities of NT$2.69b due within 12 months, and liabilities of NT$1.65b due beyond 12 months. Offsetting these obligations, it had cash of NT$3.65b as well as receivables valued at NT$939.2m due within 12 months. So it can boast NT$242.4m more liquid assets than total liabilities.

Having regard to KMC (Kuei Meng) International's size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the NT$17.6b company is short on cash, but still worth keeping an eye on the balance sheet. Succinctly put, KMC (Kuei Meng) International boasts net cash, so it's fair to say it does not have a heavy debt load!

It is just as well that KMC (Kuei Meng) International's load is not too heavy, because its EBIT was down 56% over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if KMC (Kuei Meng) International can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While KMC (Kuei Meng) International has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the most recent three years, KMC (Kuei Meng) International recorded free cash flow worth 72% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that KMC (Kuei Meng) International has net cash of NT$839.5m, as well as more liquid assets than liabilities. And it impressed us with free cash flow of NT$1.3b, being 72% of its EBIT. So we don't have any problem with KMC (Kuei Meng) International's use of debt. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 2 warning signs for KMC (Kuei Meng) International you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if KMC (Kuei Meng) International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:5306

KMC (Kuei Meng) International

Manufactures and sells various types of chains, motorcycle components, and vehicle components in Asia, Europe, and the United States.

Flawless balance sheet, undervalued and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor