Advertisement

Is Cathay Consolidated, Inc.'s(TPE:1342) Recent Stock Performance Tethered To Its Strong Fundamentals?

Cathay Consolidated (TPE:1342) has had a great run on the share market with its stock up by a significant 6.5% over the last month. Given that the market rewards strong financials in the long-term, we wonder if that is the case in this instance. Particularly, we will be paying attention to Cathay Consolidated's ROE today.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. Put another way, it reveals the company's success at turning shareholder investments into profits.

Check out our latest analysis for Cathay Consolidated

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Cathay Consolidated is:

13% = NT$196m ÷ NT$1.5b (Based on the trailing twelve months to December 2020).

The 'return' is the income the business earned over the last year. Another way to think of that is that for every NT$1 worth of equity, the company was able to earn NT$0.13 in profit.

What Has ROE Got To Do With Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

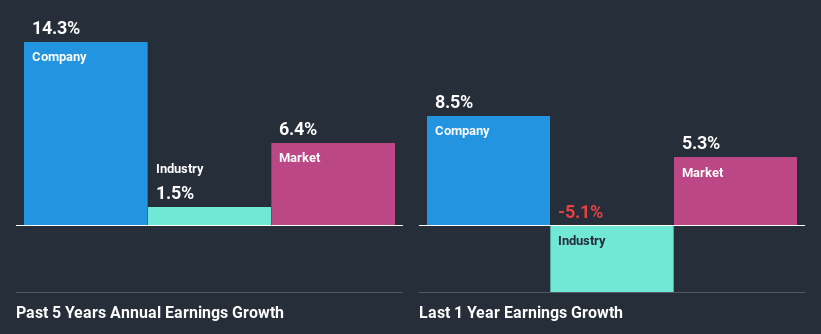

Cathay Consolidated's Earnings Growth And 13% ROE

To begin with, Cathay Consolidated seems to have a respectable ROE. On comparing with the average industry ROE of 7.1% the company's ROE looks pretty remarkable. This probably laid the ground for Cathay Consolidated's moderate 14% net income growth seen over the past five years.

Next, on comparing with the industry net income growth, we found that Cathay Consolidated's growth is quite high when compared to the industry average growth of 1.5% in the same period, which is great to see.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is Cathay Consolidated fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Cathay Consolidated Making Efficient Use Of Its Profits?

Cathay Consolidated has a three-year median payout ratio of 44%, which implies that it retains the remaining 56% of its profits. This suggests that its dividend is well covered, and given the decent growth seen by the company, it looks like management is reinvesting its earnings efficiently.

While Cathay Consolidated has seen growth in its earnings, it only recently started to pay a dividend. It is most likely that the company decided to impress new and existing shareholders with a dividend.

Conclusion

In total, we are pretty happy with Cathay Consolidated's performance. In particular, it's great to see that the company is investing heavily into its business and along with a high rate of return, that has resulted in a sizeable growth in its earnings. If the company continues to grow its earnings the way it has, that could have a positive impact on its share price given how earnings per share influence long-term share prices. Not to forget, share price outcomes are also dependent on the potential risks a company may face. So it is important for investors to be aware of the risks involved in the business. You can see the 2 risks we have identified for Cathay Consolidated by visiting our risks dashboard for free on our platform here.

When trading Cathay Consolidated or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:1342

Cathay Consolidated

Operates as a contract manufacturer of technical fabrics and finished goods in Taiwan.

Flawless balance sheet second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

932 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative