- Taiwan

- /

- Trade Distributors

- /

- TWSE:8374

Optimistic Investors Push Ace Pillar Co., Ltd. (TWSE:8374) Shares Up 33% But Growth Is Lacking

Despite an already strong run, Ace Pillar Co., Ltd. (TWSE:8374) shares have been powering on, with a gain of 33% in the last thirty days. The last 30 days bring the annual gain to a very sharp 34%.

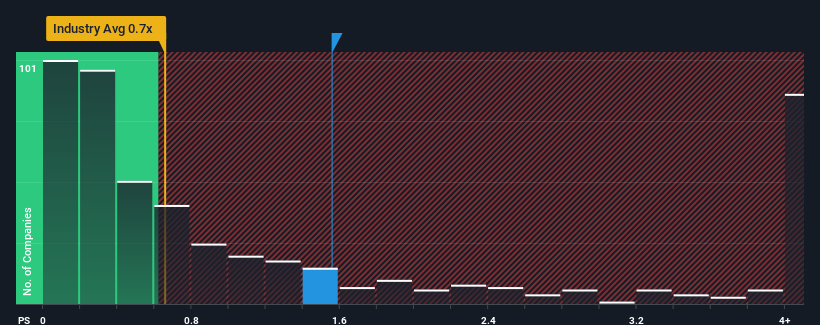

In spite of the firm bounce in price, it's still not a stretch to say that Ace Pillar's price-to-sales (or "P/S") ratio of 1.6x right now seems quite "middle-of-the-road" compared to the Trade Distributors industry in Taiwan, where the median P/S ratio is around 1.2x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Ace Pillar

How Ace Pillar Has Been Performing

For example, consider that Ace Pillar's financial performance has been poor lately as its revenue has been in decline. Perhaps investors believe the recent revenue performance is enough to keep in line with the industry, which is keeping the P/S from dropping off. If not, then existing shareholders may be a little nervous about the viability of the share price.

Although there are no analyst estimates available for Ace Pillar, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.How Is Ace Pillar's Revenue Growth Trending?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Ace Pillar's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 18% decrease to the company's top line. This means it has also seen a slide in revenue over the longer-term as revenue is down 1.5% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

In contrast to the company, the rest of the industry is expected to grow by 7.5% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this in mind, we find it worrying that Ace Pillar's P/S exceeds that of its industry peers. Apparently many investors in the company are way less bearish than recent times would indicate and aren't willing to let go of their stock right now. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

The Key Takeaway

Its shares have lifted substantially and now Ace Pillar's P/S is back within range of the industry median. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our look at Ace Pillar revealed its shrinking revenues over the medium-term haven't impacted the P/S as much as we anticipated, given the industry is set to grow. When we see revenue heading backwards in the context of growing industry forecasts, it'd make sense to expect a possible share price decline on the horizon, sending the moderate P/S lower. Unless the recent medium-term conditions improve markedly, investors will have a hard time accepting the share price as fair value.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for Ace Pillar with six simple checks on some of these key factors.

If these risks are making you reconsider your opinion on Ace Pillar, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TWSE:8374

Ace Pillar

An industrial automation company, distributes automatic mechatronics components in Taiwan and internationally.

Excellent balance sheet with acceptable track record.

Similar Companies

Market Insights

Community Narratives