Advertisement

- Taiwan

- /

- Construction

- /

- TWSE:2543

Market Participants Recognise Hwang Chang General Contractor Co., Ltd's (TWSE:2543) Earnings Pushing Shares 32% Higher

Hwang Chang General Contractor Co., Ltd (TWSE:2543) shares have continued their recent momentum with a 32% gain in the last month alone. The last 30 days were the cherry on top of the stock's 614% gain in the last year, which is nothing short of spectacular.

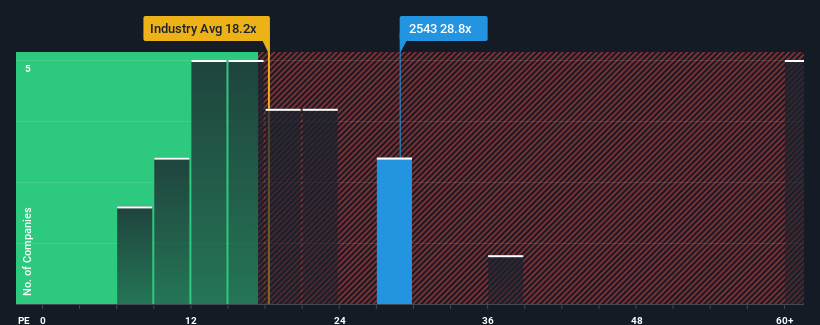

Following the firm bounce in price, given around half the companies in Taiwan have price-to-earnings ratios (or "P/E's") below 23x, you may consider Hwang Chang General Contractor as a stock to potentially avoid with its 28.8x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

With earnings growth that's exceedingly strong of late, Hwang Chang General Contractor has been doing very well. The P/E is probably high because investors think this strong earnings growth will be enough to outperform the broader market in the near future. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for Hwang Chang General Contractor

Is There Enough Growth For Hwang Chang General Contractor?

The only time you'd be truly comfortable seeing a P/E as high as Hwang Chang General Contractor's is when the company's growth is on track to outshine the market.

Retrospectively, the last year delivered an exceptional 135% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 1,602% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 24% shows it's noticeably more attractive on an annualised basis.

In light of this, it's understandable that Hwang Chang General Contractor's P/E sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Key Takeaway

Hwang Chang General Contractor's P/E is getting right up there since its shares have risen strongly. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Hwang Chang General Contractor maintains its high P/E on the strength of its recent three-year growth being higher than the wider market forecast, as expected. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. If recent medium-term earnings trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

It is also worth noting that we have found 2 warning signs for Hwang Chang General Contractor (1 can't be ignored!) that you need to take into consideration.

If you're unsure about the strength of Hwang Chang General Contractor's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Hwang Chang General Contractor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2543

Hwang Chang General Contractor

Engages in the contracting business of civil engineering projects in Taiwan.

Solid track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor