Advertisement

- Taiwan

- /

- Electrical

- /

- TWSE:1529

Klingon Aerospace Inc.'s (TPE:1529) Stock Has Seen Strong Momentum: Does That Call For Deeper Study Of Its Financial Prospects?

Klingon Aerospace's (TPE:1529) stock is up by a considerable 14% over the past three months. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to study its financial indicators more closely to see if they had a hand to play in the recent price move. Particularly, we will be paying attention to Klingon Aerospace's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for Klingon Aerospace

How To Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Klingon Aerospace is:

8.3% = NT$89m ÷ NT$1.1b (Based on the trailing twelve months to September 2020).

The 'return' is the income the business earned over the last year. That means that for every NT$1 worth of shareholders' equity, the company generated NT$0.08 in profit.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

A Side By Side comparison of Klingon Aerospace's Earnings Growth And 8.3% ROE

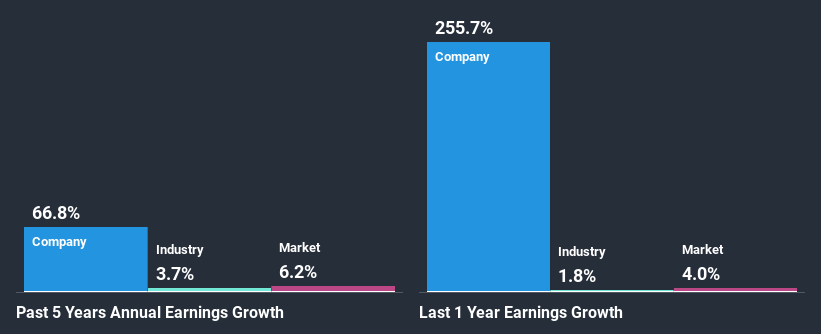

On the face of it, Klingon Aerospace's ROE is not much to talk about. Yet, a closer study shows that the company's ROE is similar to the industry average of 7.9%. Particularly, the exceptional 67% net income growth seen by Klingon Aerospace over the past five years is pretty remarkable. Considering the moderately low ROE, it is quite possible that there might be some other aspects that are positively influencing the company's earnings growth. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

As a next step, we compared Klingon Aerospace's net income growth with the industry, and pleasingly, we found that the growth seen by the company is higher than the average industry growth of 3.7%.

Earnings growth is an important metric to consider when valuing a stock. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. This then helps them determine if the stock is placed for a bright or bleak future. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Klingon Aerospace is trading on a high P/E or a low P/E, relative to its industry.

Is Klingon Aerospace Making Efficient Use Of Its Profits?

Klingon Aerospace has a significant three-year median payout ratio of 66%, meaning the company only retains 34% of its income. This implies that the company has been able to achieve high earnings growth despite returning most of its profits to shareholders.

While Klingon Aerospace has seen growth in its earnings, it only recently started to pay a dividend. It is most likely that the company decided to impress new and existing shareholders with a dividend.

Conclusion

In total, it does look like Klingon Aerospace has some positive aspects to its business. While no doubt its earnings growth is pretty substantial, we do feel that the reinvestment rate is pretty low, meaning, the earnings growth number could have been significantly higher had the company been retaining more of its profits. So far, we've only made a quick discussion around the company's earnings growth. To gain further insights into Klingon Aerospace's past profit growth, check out this visualization of past earnings, revenue and cash flows.

If you decide to trade Klingon Aerospace, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TWSE:1529

Luxe Green Energy Technology

Engages in the design, manufacture, installation, and sale of high and low voltage distribution panels and various electrical and electronic equipment in Taiwan.

Low with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|43.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|51.3% undervalued

TO

Community Contributor