- Turkey

- /

- Industrial REITs

- /

- IBSE:RYGYO

Undiscovered Gems To Watch This September 2024

Reviewed by Simply Wall St

As global markets navigate a period of recovery and anticipation of potential interest rate cuts, small-cap stocks have shown resilience and promise. With the S&P 600 Index reflecting a positive trend, it's an opportune time to explore undiscovered gems that could benefit from these favorable conditions. In this article, we'll highlight three small-cap stocks that stand out for their unique strengths and potential in the current economic landscape.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Petrol d.d | 42.18% | 17.56% | -0.49% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Amana Cooperative Insurance | NA | -1.95% | 20.64% | ★★★★★★ |

| MOBI Industry | 28.24% | 6.15% | 18.49% | ★★★★★☆ |

| Saudi Azm for Communication and Information Technology | 8.57% | 6.93% | 21.97% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| Capricorn Group | 67.47% | 9.63% | 12.07% | ★★★★☆☆ |

We'll examine a selection from our screener results.

Kardemir Karabük Demir Çelik Sanayi Ve Ticaret (IBSE:KRDMD)

Simply Wall St Value Rating: ★★★★★☆

Overview: Kardemir Karabük Demir Çelik Sanayi Ve Ticaret A.S. (ticker: IBSE:KRDMD) is a Turkish company engaged in the production and sale of iron and steel products, with a market cap of TRY25.09 billion.

Operations: Kardemir generates revenue primarily from the sale of iron and steel products. The company's net profit margin stands at 12.45%.

Kardemir Karabük Demir Çelik Sanayi Ve Ticaret, a small cap player in the metals and mining sector, has seen its debt to equity ratio drop significantly from 46.5% to 3.8% over five years. Despite reporting a net loss of TRY 927 million for Q2 2024 and TRY 1,829 million for the first half of the year, it trades at nearly 69% below its estimated fair value. The company's earnings are forecasted to grow by an impressive 74.58% annually going forward.

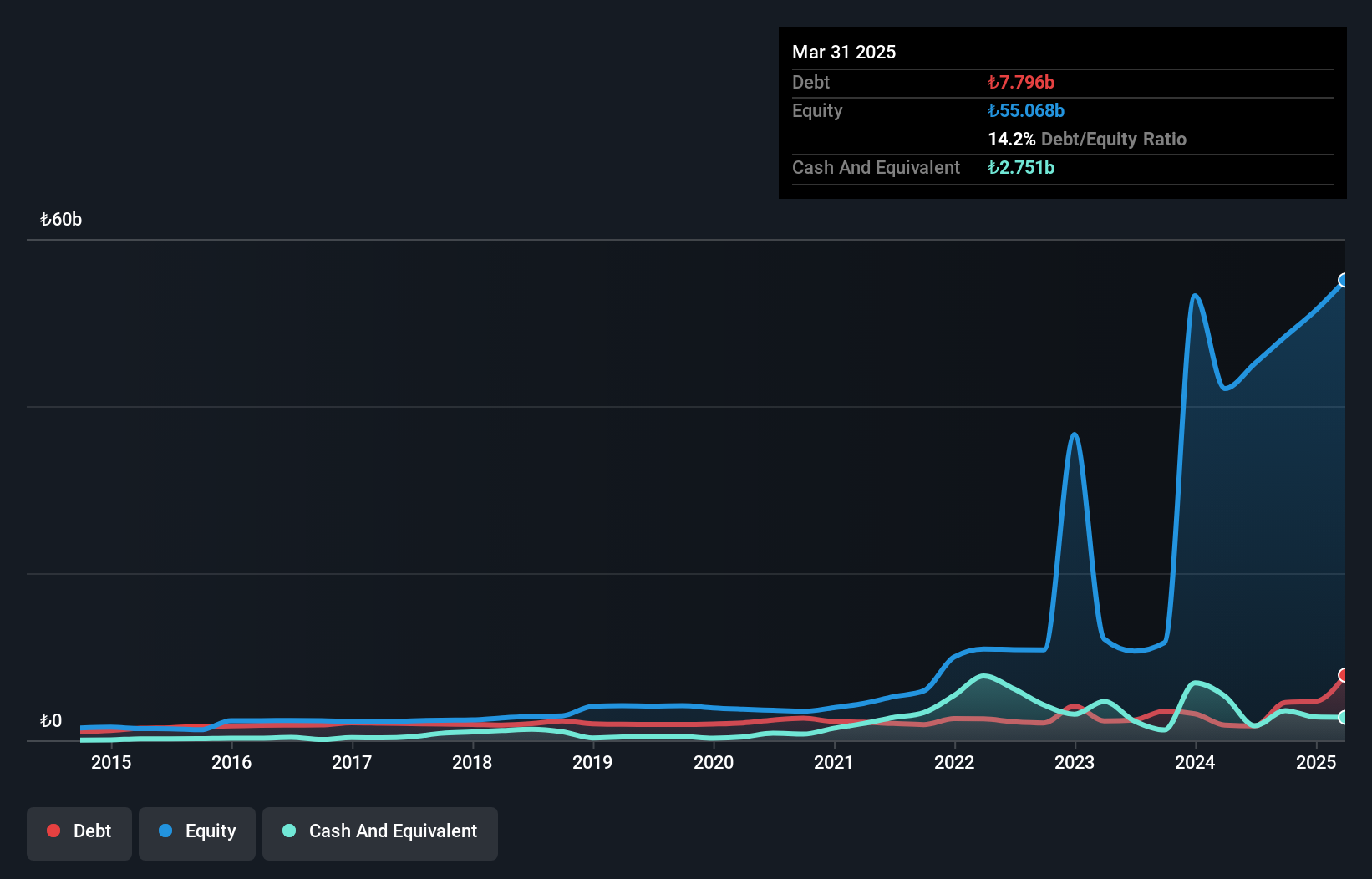

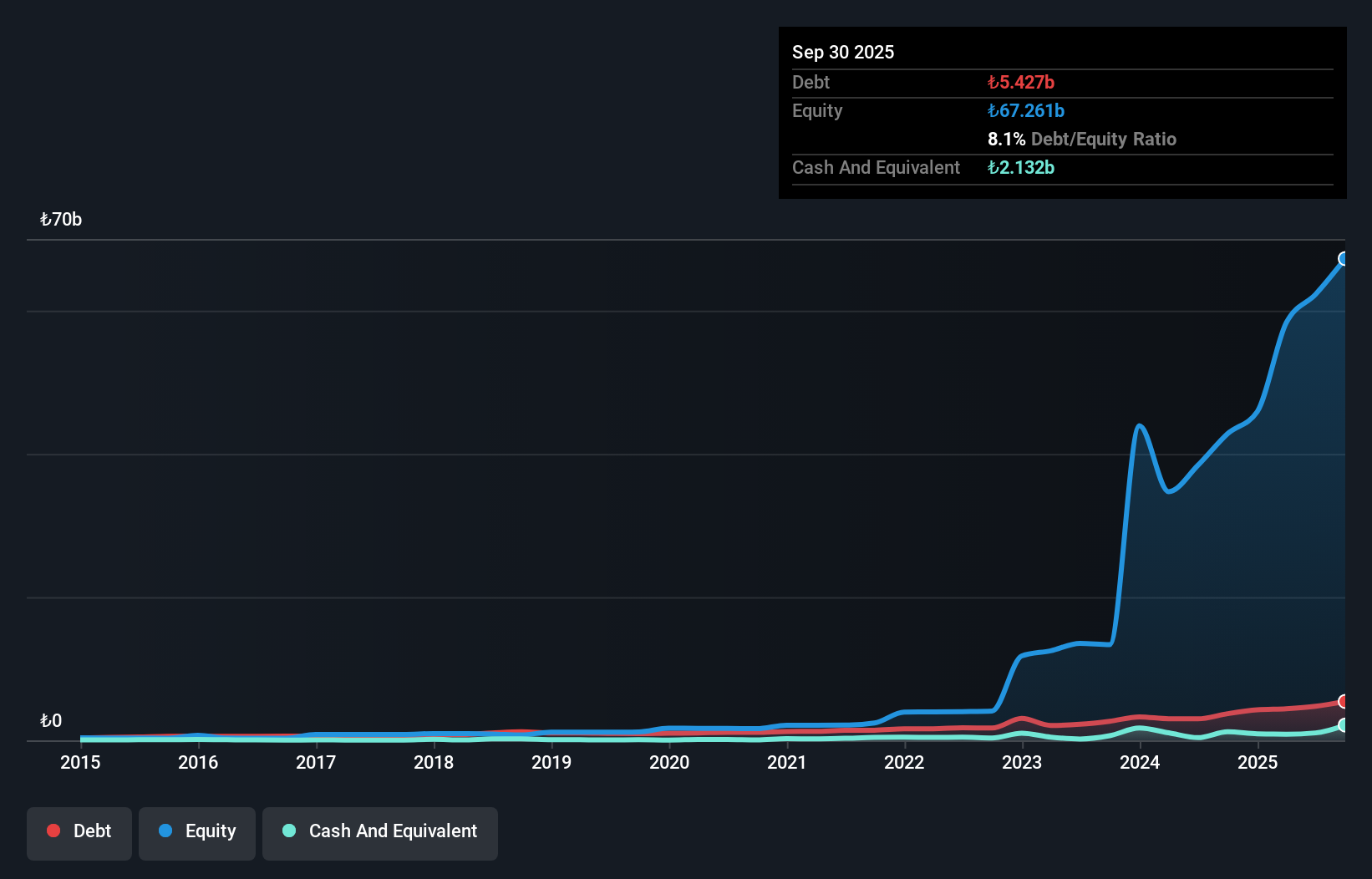

Reysas Gayrimenkul Yatirim Ortakligi (IBSE:RYGYO)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Reysas Gayrimenkul Yatirim Ortakligi A.S. (IBSE:RYGYO) operates in the real estate investment sector with a market cap of TRY24.70 billion.

Operations: Reysas Gayrimenkul Yatirim Ortakligi A.S. generates revenue primarily from its real estate investments. The company has a net profit margin of 22.50%.

Reysas Gayrimenkul Yatirim Ortakligi (RYGYO) has seen remarkable growth, with earnings surging by 107.6% over the past year, significantly outpacing the Industrial REITs industry average of 4.6%. The company's net debt to equity ratio stands at a satisfactory 6.9%, and its price-to-earnings ratio is an attractive 1.4x compared to the TR market's 16.1x. Additionally, RYGYO's debt to equity ratio has improved from 86.2% to 7.9% over five years, indicating robust financial health and effective management strategies.

Protector Forsikring (OB:PROT)

Simply Wall St Value Rating: ★★★★★☆

Overview: Protector Forsikring ASA operates as a non-life insurance company offering various insurance products to the commercial and public sectors, as well as grouped insurance schemes markets in Norway, Denmark, Sweden, the United Kingdom, and Finland, with a market cap of NOK19.54 billion.

Operations: Protector Forsikring ASA's primary revenue stream comes from its non-life insurance products, generating NOK11.18 billion. The company's net profit margin is a key financial metric to consider.

Protector Forsikring, a smaller insurance player, has shown mixed performance recently. Despite its debt to equity ratio improving from 62.5% to 40.4% over five years, earnings growth was negative at -23.8%, contrasting sharply with the industry average of 18.8%. The company reported net income of NOK 254 million for Q2 2024, up from NOK 219 million last year, and basic earnings per share rising to NOK 3.1 from NOK 2.7 in the same period. Interest coverage remains robust at an impressive EBIT multiple of 24.7x.

- Click here and access our complete health analysis report to understand the dynamics of Protector Forsikring.

Explore historical data to track Protector Forsikring's performance over time in our Past section.

Taking Advantage

- Investigate our full lineup of 4744 Undiscovered Gems With Strong Fundamentals right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About IBSE:RYGYO

Reysas Gayrimenkul Yatirim Ortakligi

Reysas Gayrimenkul Yatirim Ortakligi A.S.

Proven track record with adequate balance sheet.