As global markets navigate a complex landscape, major U.S. stock indexes have shown mixed results, with growth stocks outperforming value stocks significantly. In this context, penny stocks—often seen as smaller or newer companies—remain an intriguing investment area due to their potential for growth at lower price points. Despite being considered a somewhat outdated term, the opportunities they represent are still relevant today, especially when these companies exhibit strong balance sheets and solid fundamentals.

Top 10 Penny Stocks

| Name | Share Price | Market Cap | Financial Health Rating |

| DXN Holdings Bhd (KLSE:DXN) | MYR0.515 | MYR2.56B | ★★★★★★ |

| Tristel (AIM:TSTL) | £3.65 | £174.08M | ★★★★★★ |

| Embark Early Education (ASX:EVO) | A$0.785 | A$144.03M | ★★★★☆☆ |

| Hil Industries Berhad (KLSE:HIL) | MYR0.90 | MYR298.75M | ★★★★★★ |

| ME Group International (LSE:MEGP) | £2.16 | £813.81M | ★★★★★★ |

| Lever Style (SEHK:1346) | HK$0.87 | HK$552.27M | ★★★★★★ |

| Bosideng International Holdings (SEHK:3998) | HK$4.05 | HK$44.6B | ★★★★★★ |

| LaserBond (ASX:LBL) | A$0.56 | A$65.64M | ★★★★★★ |

| Datasonic Group Berhad (KLSE:DSONIC) | MYR0.405 | MYR1.13B | ★★★★★★ |

| Secure Trust Bank (LSE:STB) | £3.53 | £67.32M | ★★★★☆☆ |

Click here to see the full list of 5,696 stocks from our Penny Stocks screener.

Let's take a closer look at a couple of our picks from the screened companies.

Oiltek International (Catalist:HQU)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Oiltek International Limited is an investment holding company that supplies and provides engineering design and commissioning services for oil extraction equipment and plants across Asia, America, and Africa, with a market cap of SGD137.28 million.

Operations: The company's revenue is primarily derived from Edible & Non-Edible Oil Refinery at MYR188.17 million, followed by Product Sales and Trading at MYR19.68 million, and Renewable Energy at MYR16.99 million.

Market Cap: SGD137.28M

Oiltek International, with a market cap of SGD137.28 million, derives substantial revenue from its Edible & Non-Edible Oil Refinery operations (MYR188.17 million). The company exhibits strong financial health with short-term assets exceeding both short and long-term liabilities and is debt-free for the past five years. Earnings have grown significantly by 52.5% over the past year, outpacing industry averages, while maintaining high-quality earnings and improved profit margins at 10%. Despite these strengths, its share price remains highly volatile over recent months. The board is experienced; however, management tenure data is insufficient to assess experience levels fully.

- Unlock comprehensive insights into our analysis of Oiltek International stock in this financial health report.

- Examine Oiltek International's earnings growth report to understand how analysts expect it to perform.

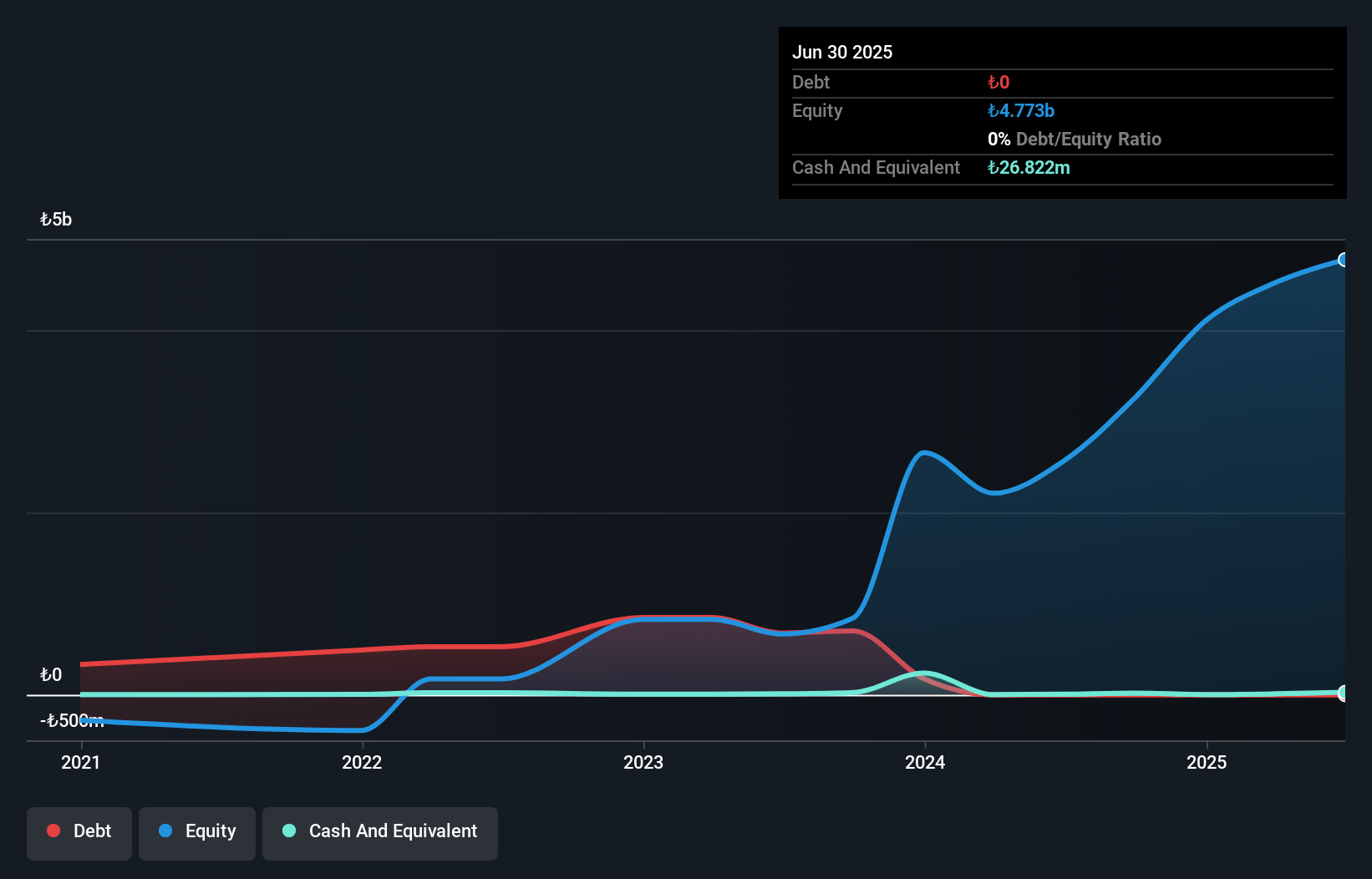

Bati Ege Gayrimenkul Yatirim Ortakligi (IBSE:BEGYO)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Bati Ege Gayrimenkul Yatirim Ortakligi A.S. is an investment company focusing on the real estate sector in Denizli and the broader Aegean Region, with a market cap of TRY3.58 billion.

Operations: The company generates revenue of TRY301.89 million from its operations in Turkey.

Market Cap: TRY3.58B

Bati Ege Gayrimenkul Yatirim Ortakligi, with a market cap of TRY3.58 billion, has shown robust financial performance recently. The company reported substantial revenue growth to TRY254.19 million in Q3 2024 from TRY29.58 million the previous year, alongside significant net income increases to TRY460.52 million from TRY40.9 million. Despite negative earnings growth over the past year, its five-year earnings have grown significantly by 41.3% annually and it remains debt-free with short-term assets exceeding liabilities by a wide margin (TRY1 billion vs TRY371.7 million). However, profit margins have declined compared to last year and return on equity is considered low at 15.8%.

- Click here to discover the nuances of Bati Ege Gayrimenkul Yatirim Ortakligi with our detailed analytical financial health report.

- Review our historical performance report to gain insights into Bati Ege Gayrimenkul Yatirim Ortakligi's track record.

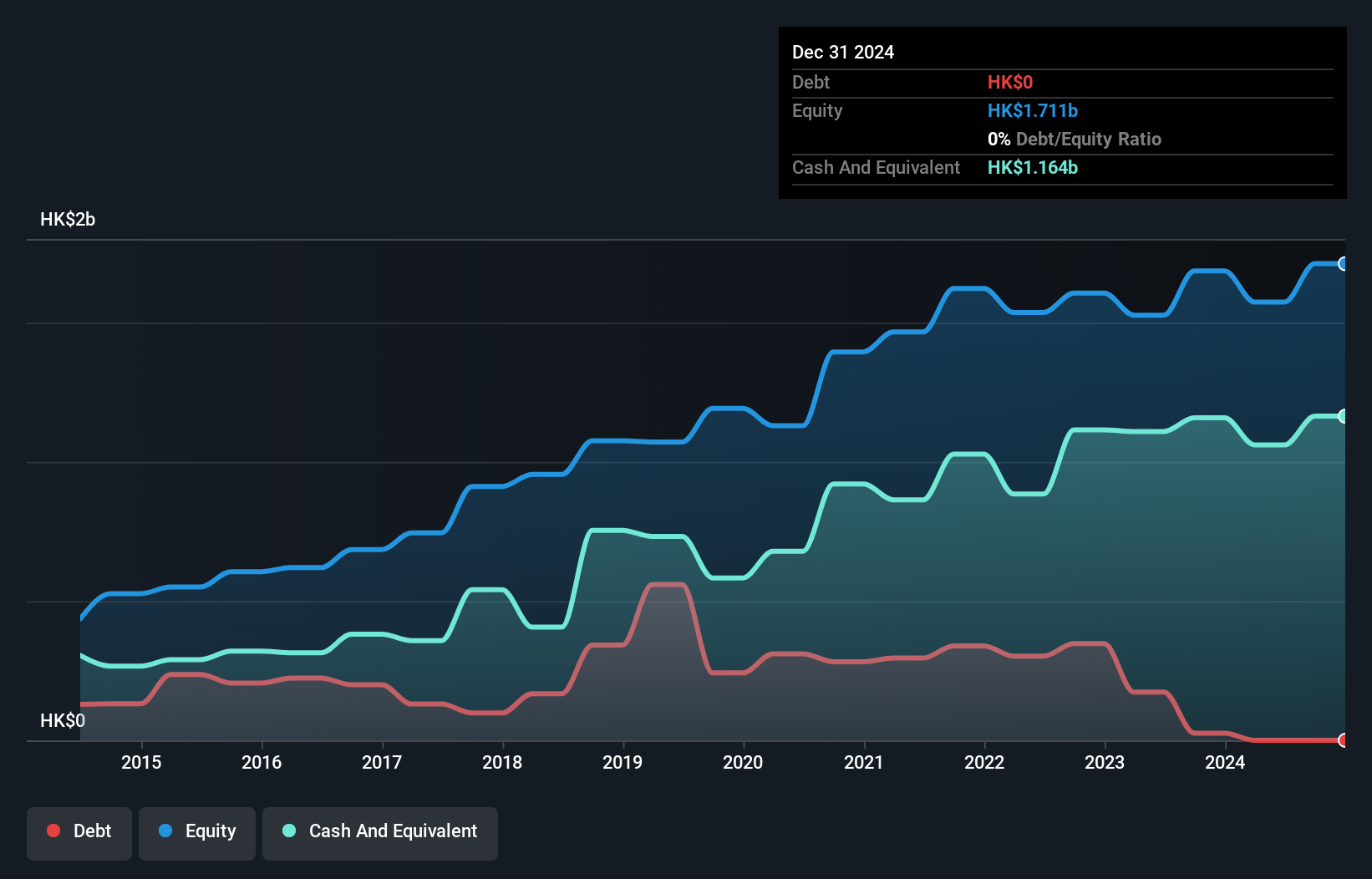

TK Group (Holdings) (SEHK:2283)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: TK Group (Holdings) Limited is an investment holding company involved in the manufacture, sale, subcontracting, fabrication, and modification of molds and plastic components, with a market capitalization of approximately HK$1.61 billion.

Operations: The company's revenue is derived from two main segments: Mold Fabrication, contributing HK$767.37 million, and Plastic Components Manufacturing, generating HK$1.47 billion.

Market Cap: HK$1.61B

TK Group (Holdings) Limited, with a market cap of HK$1.61 billion, demonstrates financial stability with short-term assets of HK$2.0 billion surpassing both its short-term and long-term liabilities. The company is debt-free, eliminating concerns over interest payments and improving from a previous debt to equity ratio of 52.2%. Its net profit margins have slightly improved to 10.9%, while earnings growth is forecasted at 19.11% per year despite past declines averaging -6.5% annually over five years. However, the company's dividend track record remains unstable and its Return on Equity is considered low at 14.6%.

- Dive into the specifics of TK Group (Holdings) here with our thorough balance sheet health report.

- Explore TK Group (Holdings)'s analyst forecasts in our growth report.

Where To Now?

- Dive into all 5,696 of the Penny Stocks we have identified here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bati Ege Gayrimenkul Yatirim Ortakligi might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About IBSE:BEGYO

Bati Ege Gayrimenkul Yatirim Ortakligi

An investment company, invests in the real estate sector in Denizli and the rest of Aegean Region.

Flawless balance sheet low.

Market Insights

Community Narratives