Global markets have shown resilience recently, with U.S. stocks recovering from an early August sell-off and European indices posting strong gains amid hopes for interest rate cuts. This positive sentiment is underpinned by encouraging inflation data and robust retail sales, suggesting that the economy might achieve a “soft landing.” In this context, identifying undervalued stocks can be particularly rewarding as they offer potential for growth in a market that is stabilizing and showing signs of recovery. Here are three stocks estimated to be undervalued in August 2024.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Italian Sea Group (BIT:TISG) | €8.68 | €17.35 | 50% |

| Apollo Pipes (BSE:531761) | ₹576.25 | ₹1148.54 | 49.8% |

| Mader Group (ASX:MAD) | A$5.29 | A$10.55 | 49.8% |

| Singapore Technologies Engineering (SGX:S63) | SGD4.50 | SGD8.96 | 49.8% |

| Trisul (BOVESPA:TRIS3) | R$4.64 | R$9.25 | 49.9% |

| Visional (TSE:4194) | ¥8610.00 | ¥17155.52 | 49.8% |

| Shanghai INT Medical Instruments (SEHK:1501) | HK$28.20 | HK$56.25 | 49.9% |

| QuinStreet (NasdaqGS:QNST) | US$17.09 | US$33.99 | 49.7% |

| Vertex Pharmaceuticals (NasdaqGS:VRTX) | US$479.89 | US$958.94 | 50% |

| Nxera Pharma (TSE:4565) | ¥1731.00 | ¥3461.43 | 50% |

Let's review some notable picks from our screened stocks.

Endesa (BME:ELE)

Overview: Endesa, S.A. is involved in the generation, distribution, and sale of electricity across various countries including Spain, Portugal, France, Germany, Morocco, Italy, the United Kingdom, and Singapore with a market cap of €19.60 billion.

Operations: Endesa's revenue segments include €2.47 billion from distribution, €17.48 billion from retail, €357 million from Endesa X, €466 million from structure, €1.25 billion from renewables, and €9.11 billion from conventional generation.

Estimated Discount To Fair Value: 36%

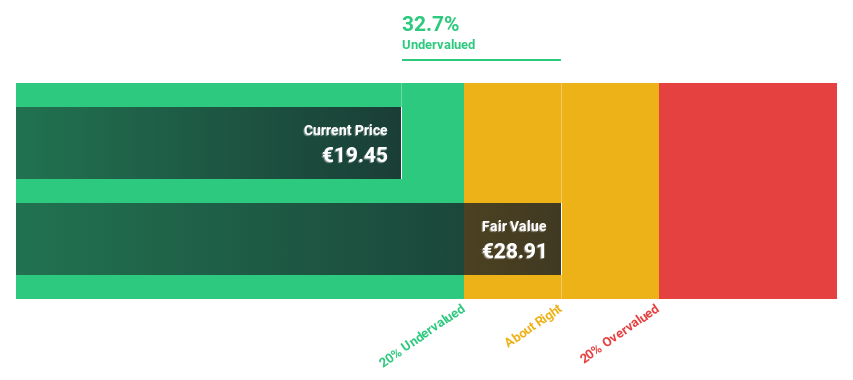

Endesa, S.A. reported a decline in sales and revenue for the half year ended June 30, 2024, with net income dropping to €800 million from €879 million a year ago. Despite this, Endesa is trading at 36% below its estimated fair value of €28.91 per share (€18.52 currently). The company's earnings are forecast to grow annually by 18.22%, outpacing the Spanish market's growth rate of 9.6%. However, it has a high level of debt and an unstable dividend track record.

- Upon reviewing our latest growth report, Endesa's projected financial performance appears quite optimistic.

- Take a closer look at Endesa's balance sheet health here in our report.

Yapi ve Kredi Bankasi (IBSE:YKBNK)

Overview: Yapi ve Kredi Bankasi A.S., with a market cap of TRY263.04 billion, offers a range of banking products and services in Turkey and internationally through its subsidiaries.

Operations: Yapi ve Kredi Bankasi A.S. generates revenue from several segments, including Retail Banking (TRY77.46 billion), Commercial and SME Banking (TRY52.24 billion), Corporate Banking (TRY13.70 billion), Other Domestic Operations (TRY11.36 billion), Other Foreign Operations (TRY4.50 billion), and Treasury, Asset Liability Management and Other (TRY4.47 billion).

Estimated Discount To Fair Value: 34.2%

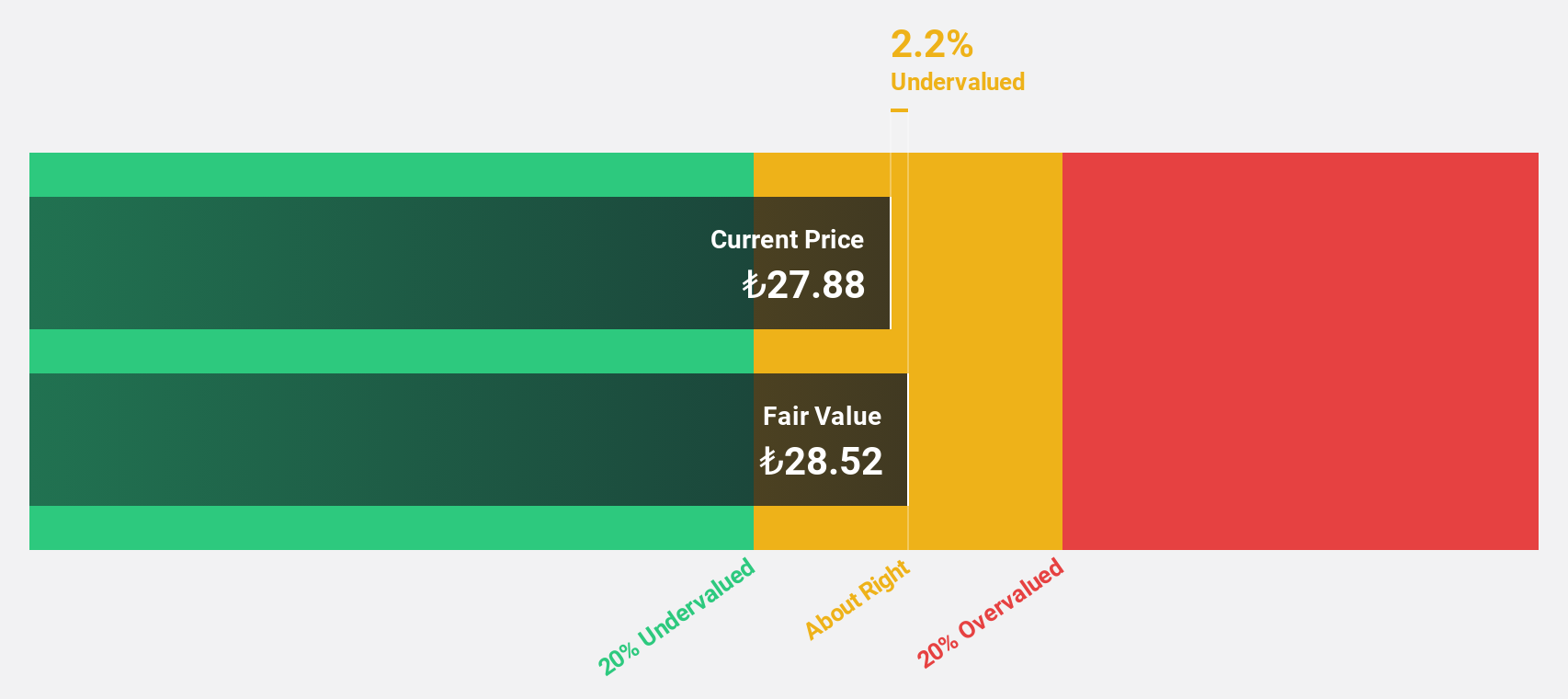

Yapi ve Kredi Bankasi's recent earnings report shows a substantial increase in net interest income, rising to TRY 20.22 billion for Q2 2024 from TRY 8.92 billion a year ago. Despite this, net income fell to TRY 7.10 billion from TRY 11.48 billion due to higher expenses and provisions. The bank is trading at approximately 34% below its estimated fair value of TRY47.36 per share (TRY31.14 currently), with significant expected earnings growth of over 20% annually for the next three years, making it potentially undervalued based on cash flows despite an unstable dividend track record and high bad loans ratio of 2.6%.

- The analysis detailed in our Yapi ve Kredi Bankasi growth report hints at robust future financial performance.

- Click here and access our complete balance sheet health report to understand the dynamics of Yapi ve Kredi Bankasi.

Pantai Indah Kapuk Dua (IDX:PANI)

Overview: PT Pantai Indah Kapuk Dua Tbk, with a market cap of IDR95.20 trillion, operates as a property developer in Indonesia through its subsidiaries.

Operations: The company generates revenue primarily from its Real Estate segment, amounting to IDR1.92 trillion.

Estimated Discount To Fair Value: 35.5%

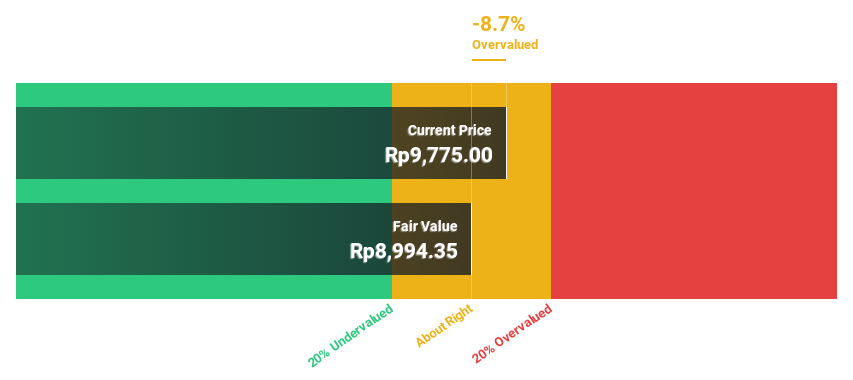

Pantai Indah Kapuk Dua is trading at IDR5800, significantly below its estimated fair value of IDR8989.53. Despite a recent reduction in profit margins to 11% from 23.5%, the company is forecast to grow earnings by 47.7% per year and revenue by 29.6% annually, outpacing the Indonesian market's growth rates of 27.2% and 9.3%, respectively. However, shareholders have experienced dilution in the past year, which could be a concern for potential investors evaluating its undervaluation based on cash flows.

- According our earnings growth report, there's an indication that Pantai Indah Kapuk Dua might be ready to expand.

- Get an in-depth perspective on Pantai Indah Kapuk Dua's balance sheet by reading our health report here.

Seize The Opportunity

- Explore the 932 names from our Undervalued Stocks Based On Cash Flows screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About IBSE:YKBNK

Yapi ve Kredi Bankasi

Provides commercial banking and financial products and services in Turkey and internationally.

Exceptional growth potential with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives