Advertisement

SBS Transit Ltd (SGX:S61) will increase its dividend from last year's comparable payment on the 13th of May to SGD0.231. This will take the annual payment to 7.2% of the stock price, which is above what most companies in the industry pay.

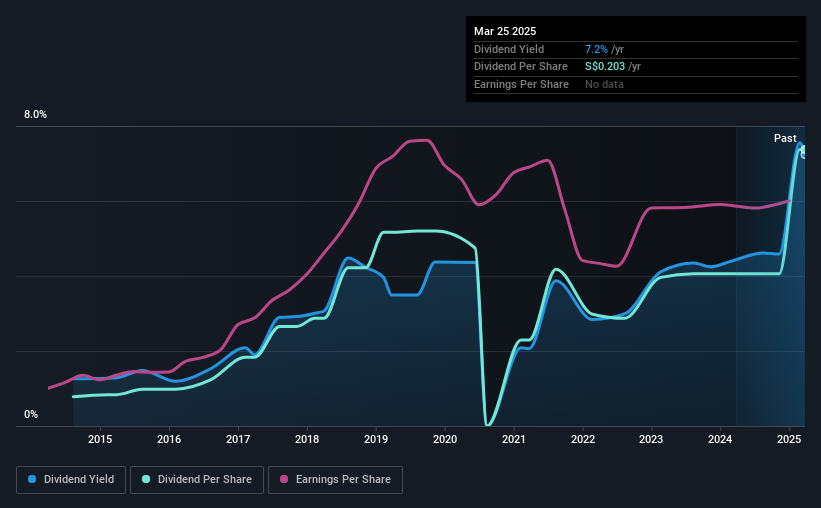

Estimates Indicate SBS Transit's Could Struggle to Maintain Dividend Payments In The Future

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Prior to this announcement, SBS Transit's dividend was making up a very large proportion of earnings and perhaps more concerning was that it was 290% of cash flows. Paying out such a high proportion of cash flows can expose the business to needing to cut the dividend if the business runs into some challenges.

If the company can't turn things around, EPS could fall by 2.9% over the next year. If the dividend continues along recent trends, we estimate the payout ratio could reach 147%, which could put the dividend in jeopardy if the company's earnings don't improve.

View our latest analysis for SBS Transit

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. The dividend has gone from an annual total of SGD0.0215 in 2015 to the most recent total annual payment of SGD0.203. This means that it has been growing its distributions at 25% per annum over that time. SBS Transit has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend's Growth Prospects Are Limited

With a relatively unstable dividend, it's even more important to evaluate if earnings per share is growing, which could point to a growing dividend in the future. In the last five years, SBS Transit's earnings per share has shrunk at approximately 2.9% per annum. If the company is making less over time, it naturally follows that it will also have to pay out less in dividends.

The Dividend Could Prove To Be Unreliable

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The track record isn't great, and the payments are a bit high to be considered sustainable. This company is not in the top tier of income providing stocks.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. As an example, we've identified 2 warning signs for SBS Transit that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:S61

SBS Transit

Provides bus and rail public transportation services, and consultancy services relating to land transport in Singapore.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor