Advertisement

Singapore Post's (SGX:S08) Upcoming Dividend Will Be Larger Than Last Year's

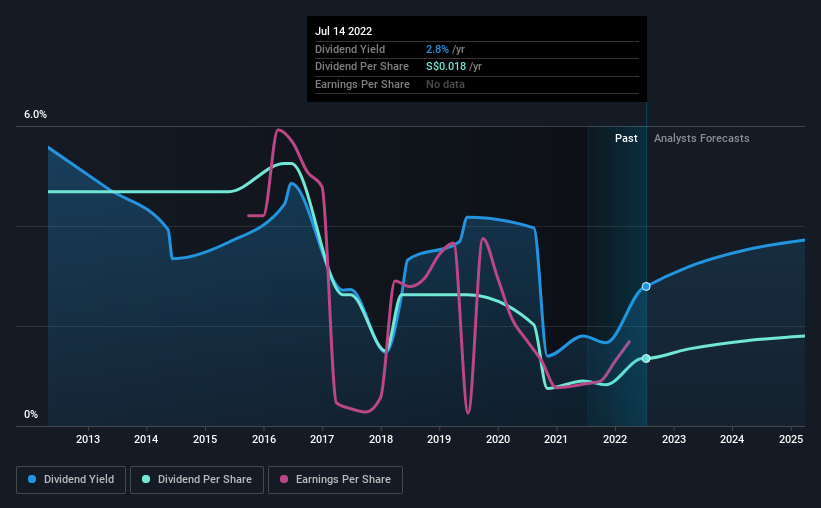

Singapore Post Limited (SGX:S08) will increase its dividend from last year's comparable payment on the 16th of August to SGD0.013. The payment will take the dividend yield to 2.8%, which is in line with the average for the industry.

See our latest analysis for Singapore Post

Singapore Post's Earnings Easily Cover the Distributions

Unless the payments are sustainable, the dividend yield doesn't mean too much. The last dividend was quite easily covered by Singapore Post's earnings. This indicates that quite a large proportion of earnings is being invested back into the business.

The next year is set to see EPS grow by 81.3%. If the dividend continues along recent trends, we estimate the payout ratio will be 25%, which is in the range that makes us comfortable with the sustainability of the dividend.

Dividend Volatility

Although the company has a long dividend history, it has been cut at least once in the last 10 years. Since 2012, the annual payment back then was SGD0.0625, compared to the most recent full-year payment of SGD0.018. The dividend has fallen 71% over that period. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

The Dividend Looks Likely To Grow

Dividends have been going in the wrong direction, so we definitely want to see a different trend in the earnings per share. We are encouraged to see that Singapore Post has grown earnings per share at 30% per year over the past five years. The company's earnings per share has grown rapidly in recent years, and it has a good balance between reinvesting and paying dividends to shareholders, so we think that Singapore Post could prove to be a strong dividend payer.

Singapore Post Looks Like A Great Dividend Stock

Overall, we think this could be an attractive income stock, and it is only getting better by paying a higher dividend this year. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. Taking this all into consideration, this looks like it could be a good dividend opportunity.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. For instance, we've picked out 1 warning sign for Singapore Post that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:S08

Singapore Post

Engages in the post and parcel, eCommerce logistics, and property businesses in Singapore and internationally.

Excellent balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|59.1% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|15.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.4% undervalued

RO

Community Contributor