- Singapore

- /

- Medical Equipment

- /

- SGX:AP4

Don't Race Out To Buy Riverstone Holdings Limited (SGX:AP4) Just Because It's Going Ex-Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Riverstone Holdings Limited (SGX:AP4) is about to go ex-dividend in just two days. Typically, the ex-dividend date is two business days before the record date, which is the date on which a company determines the shareholders eligible to receive a dividend. The ex-dividend date is an important date to be aware of as any purchase of the stock made on or after this date might mean a late settlement that doesn't show on the record date. This means that investors who purchase Riverstone Holdings' shares on or after the 8th of May will not receive the dividend, which will be paid on the 16th of May.

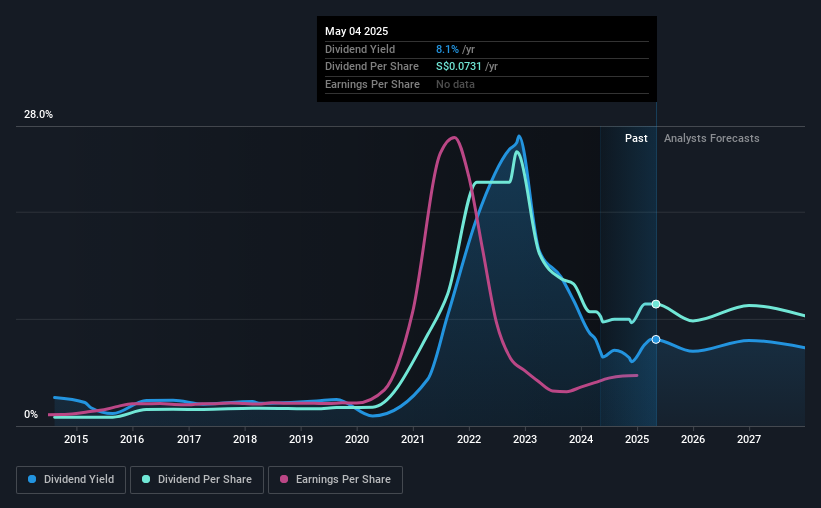

The company's next dividend payment will be RM00.08 per share. Last year, in total, the company distributed RM0.20 to shareholders. Based on the last year's worth of payments, Riverstone Holdings stock has a trailing yield of around 8.1% on the current share price of S$0.905. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! We need to see whether the dividend is covered by earnings and if it's growing.

Our free stock report includes 1 warning sign investors should be aware of before investing in Riverstone Holdings. Read for free now.Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Riverstone Holdings paid out 103% of its earnings, which is more than we're comfortable with, unless there are mitigating circumstances. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Over the past year it paid out 127% of its free cash flow as dividends, which is uncomfortably high. We're curious about why the company paid out more cash than it generated last year, since this can be one of the early signs that a dividend may be unsustainable.

Riverstone Holdings does have a large net cash position on the balance sheet, which could fund large dividends for a time, if the company so chose. Still, smart investors know that it is better to assess dividends relative to the cash and profit generated by the business. Paying dividends out of cash on the balance sheet is not long-term sustainable.

Cash is slightly more important than profit from a dividend perspective, but given Riverstone Holdings's payouts were not well covered by either earnings or cash flow, we would be concerned about the sustainability of this dividend.

Check out our latest analysis for Riverstone Holdings

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. For this reason, we're glad to see Riverstone Holdings's earnings per share have risen 17% per annum over the last five years. We're a bit put out by the fact that Riverstone Holdings paid out virtually all of its earnings and cashflow as dividends over the last year. Earnings are growing at a decent clip, so this payout ratio may prove sustainable, but it's not great to see.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the last 10 years, Riverstone Holdings has lifted its dividend by approximately 30% a year on average. Both per-share earnings and dividends have both been growing rapidly in recent times, which is great to see.

Final Takeaway

From a dividend perspective, should investors buy or avoid Riverstone Holdings? While it's nice to see earnings per share growing, we're curious about how Riverstone Holdings intends to continue growing, or maintain the dividend in a downturn given that it's paying out such a high percentage of its earnings and cashflow. Overall it doesn't look like the most suitable dividend stock for a long-term buy and hold investor.

So if you're still interested in Riverstone Holdings despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. Every company has risks, and we've spotted 1 warning sign for Riverstone Holdings you should know about.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:AP4

Riverstone Holdings

An investment holding company, engages in the manufacture and distribution of cleanroom and healthcare gloves in Malaysia, Thailand, and China.

Very undervalued with flawless balance sheet.

Market Insights

Community Narratives