Advertisement

- Singapore

- /

- Oil and Gas

- /

- SGX:AUE

Why The 43% Return On Capital At Golden Energy and Resources (SGX:AUE) Should Have Your Attention

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Speaking of which, we noticed some great changes in Golden Energy and Resources' (SGX:AUE) returns on capital, so let's have a look.

Return On Capital Employed (ROCE): What is it?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Golden Energy and Resources is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

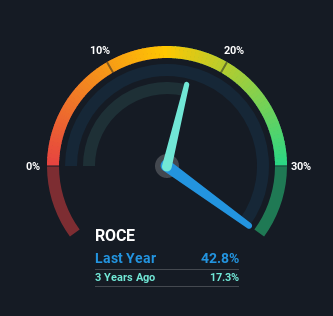

0.43 = US$473m ÷ (US$1.6b - US$464m) (Based on the trailing twelve months to December 2021).

So, Golden Energy and Resources has an ROCE of 43%. In absolute terms that's a great return and it's even better than the Oil and Gas industry average of 19%.

View our latest analysis for Golden Energy and Resources

In the above chart we have measured Golden Energy and Resources' prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Golden Energy and Resources here for free.

What The Trend Of ROCE Can Tell Us

Investors would be pleased with what's happening at Golden Energy and Resources. The numbers show that in the last five years, the returns generated on capital employed have grown considerably to 43%. The amount of capital employed has increased too, by 146%. So we're very much inspired by what we're seeing at Golden Energy and Resources thanks to its ability to profitably reinvest capital.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. Effectively this means that suppliers or short-term creditors are now funding 30% of the business, which is more than it was five years ago. Keep an eye out for future increases because when the ratio of current liabilities to total assets gets particularly high, this can introduce some new risks for the business.

In Conclusion...

All in all, it's terrific to see that Golden Energy and Resources is reaping the rewards from prior investments and is growing its capital base. Given the stock has declined 18% in the last five years, this could be a good investment if the valuation and other metrics are also appealing. With that in mind, we believe the promising trends warrant this stock for further investigation.

If you want to continue researching Golden Energy and Resources, you might be interested to know about the 1 warning sign that our analysis has discovered.

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:AUE

Golden Energy and Resources

Golden Energy and Resources Limited, an investment holding company, engages in the provision of management services, coal mining and trading, and forestry activities.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor