- Singapore

- /

- Hospitality

- /

- SGX:M04

With Mandarin Oriental International Limited (SGX:M04) It Looks Like You'll Get What You Pay For

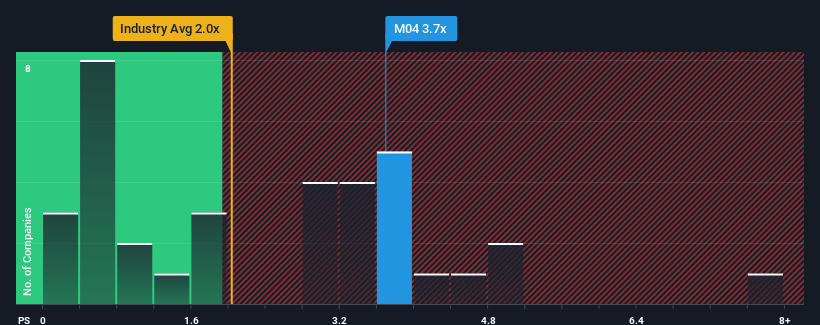

Mandarin Oriental International Limited's (SGX:M04) price-to-sales (or "P/S") ratio of 3.7x may not look like an appealing investment opportunity when you consider close to half the companies in the Hospitality industry in Singapore have P/S ratios below 2x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

Check out our latest analysis for Mandarin Oriental International

How Has Mandarin Oriental International Performed Recently?

Mandarin Oriental International has been doing a good job lately as it's been growing revenue at a solid pace. One possibility is that the P/S ratio is high because investors think this respectable revenue growth will be enough to outperform the broader industry in the near future. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Mandarin Oriental International will help you shine a light on its historical performance.How Is Mandarin Oriental International's Revenue Growth Trending?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Mandarin Oriental International's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 23% last year. Pleasingly, revenue has also lifted 204% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

When compared to the industry's one-year growth forecast of 17%, the most recent medium-term revenue trajectory is noticeably more alluring

With this in consideration, it's not hard to understand why Mandarin Oriental International's P/S is high relative to its industry peers. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

What We Can Learn From Mandarin Oriental International's P/S?

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

It's no surprise that Mandarin Oriental International can support its high P/S given the strong revenue growth its experienced over the last three-year is superior to the current industry outlook. In the eyes of shareholders, the probability of a continued growth trajectory is great enough to prevent the P/S from pulling back. Barring any significant changes to the company's ability to make money, the share price should continue to be propped up.

Plus, you should also learn about these 2 warning signs we've spotted with Mandarin Oriental International (including 1 which makes us a bit uncomfortable).

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SGX:M04

Mandarin Oriental International

Engages in the ownership and operation of hotels, resorts, and residences in Asia, Europe, the Middle East, Africa, and the Americas.

Excellent balance sheet unattractive dividend payer.

Similar Companies

Market Insights

Community Narratives