- Sweden

- /

- Electronic Equipment and Components

- /

- OM:LAGR B

Lagercrantz Group's (STO:LAGR B) Shareholders Will Receive A Bigger Dividend Than Last Year

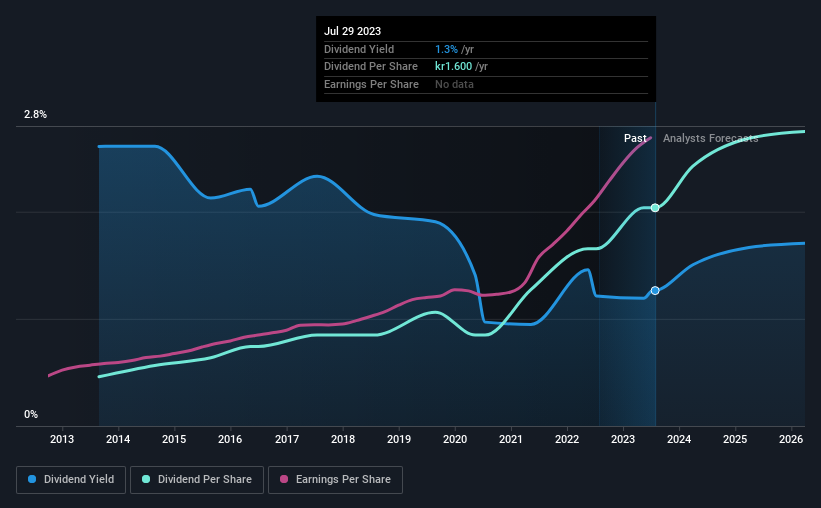

Lagercrantz Group AB (publ) (STO:LAGR B) will increase its dividend from last year's comparable payment on the 5th of September to SEK1.60. This makes the dividend yield about the same as the industry average at 1.3%.

See our latest analysis for Lagercrantz Group

Lagercrantz Group's Dividend Is Well Covered By Earnings

We like to see a healthy dividend yield, but that is only helpful to us if the payment can continue. The last dividend was quite easily covered by Lagercrantz Group's earnings. This means that a large portion of its earnings are being retained to grow the business.

Looking forward, earnings per share is forecast to rise by 40.2% over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 34%, which is in the range that makes us comfortable with the sustainability of the dividend.

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. The dividend has gone from an annual total of SEK0.361 in 2013 to the most recent total annual payment of SEK1.60. This means that it has been growing its distributions at 16% per annum over that time. Lagercrantz Group has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend Looks Likely To Grow

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. It's encouraging to see that Lagercrantz Group has been growing its earnings per share at 21% a year over the past five years. Lagercrantz Group is clearly able to grow rapidly while still returning cash to shareholders, positioning it to become a strong dividend payer in the future.

We Really Like Lagercrantz Group's Dividend

Overall, a dividend increase is always good, and we think that Lagercrantz Group is a strong income stock thanks to its track record and growing earnings. Earnings are easily covering distributions, and the company is generating plenty of cash. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Earnings growth generally bodes well for the future value of company dividend payments. See if the 5 Lagercrantz Group analysts we track are forecasting continued growth with our free report on analyst estimates for the company. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:LAGR B

Lagercrantz Group

Operates as a technology company in Sweden, Denmark, Norway, Finland, Germany, the United Kingdom, Benelux, Poland, rest of Europe, North America, Asia, and internationally.

Proven track record with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion