Advertisement

The Compensation For Hanza AB (publ)'s (STO:HANZA) CEO Looks Deserved And Here's Why

Key Insights

- Hanza to hold its Annual General Meeting on 14th of May

- Salary of kr2.95m is part of CEO Erik Stenfors's total remuneration

- The overall pay is comparable to the industry average

- Hanza's EPS grew by 384% over the past three years while total shareholder return over the past three years was 189%

The performance at Hanza AB (publ) (STO:HANZA) has been quite strong recently and CEO Erik Stenfors has played a role in it. Shareholders will have this at the front of their minds in the upcoming AGM on 14th of May. The focus will probably be on the future company strategy as shareholders cast their votes on resolutions such as executive remuneration and other matters. Here is our take on why we think CEO compensation is not extravagant.

Check out our latest analysis for Hanza

Comparing Hanza AB (publ)'s CEO Compensation With The Industry

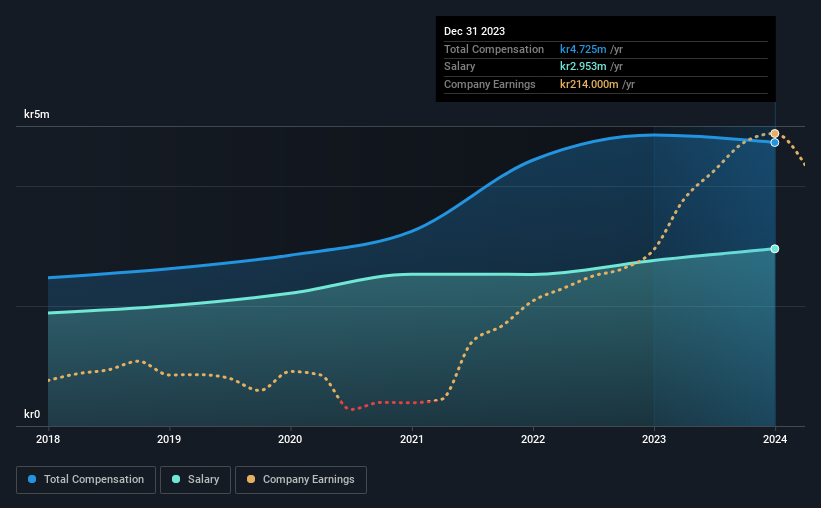

Our data indicates that Hanza AB (publ) has a market capitalization of kr2.5b, and total annual CEO compensation was reported as kr4.7m for the year to December 2023. That is, the compensation was roughly the same as last year. Notably, the salary which is kr2.95m, represents most of the total compensation being paid.

On examining similar-sized companies in the Swedish Electronic industry with market capitalizations between kr1.1b and kr4.3b, we discovered that the median CEO total compensation of that group was kr6.1m. This suggests that Hanza remunerates its CEO largely in line with the industry average. Furthermore, Erik Stenfors directly owns kr35m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | kr3.0m | kr2.8m | 62% |

| Other | kr1.8m | kr2.1m | 38% |

| Total Compensation | kr4.7m | kr4.8m | 100% |

Talking in terms of the industry, salary represented approximately 61% of total compensation out of all the companies we analyzed, while other remuneration made up 39% of the pie. There isn't a significant difference between Hanza and the broader market, in terms of salary allocation in the overall compensation package. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Hanza AB (publ)'s Growth

Hanza AB (publ) has seen its earnings per share (EPS) increase by 384% a year over the past three years. Its revenue is up 14% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Hanza AB (publ) Been A Good Investment?

Boasting a total shareholder return of 189% over three years, Hanza AB (publ) has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Seeing that the company has put in a relatively good performance, the CEO remuneration policy may not be the focus at the AGM. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 3 warning signs for Hanza that you should be aware of before investing.

Switching gears from Hanza, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Hanza might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:HANZA

Hanza

Provides contract manufacturing solutions in Sweden, Finland, Estonia, Germany, Poland, the Czech Republic, rest of the European Union, Norway, rest of Europe, North America, and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative