Advertisement

Does Alcadon Group (STO:ALCA) Have A Healthy Balance Sheet?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Alcadon Group AB (publ) (STO:ALCA) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Alcadon Group

What Is Alcadon Group's Debt?

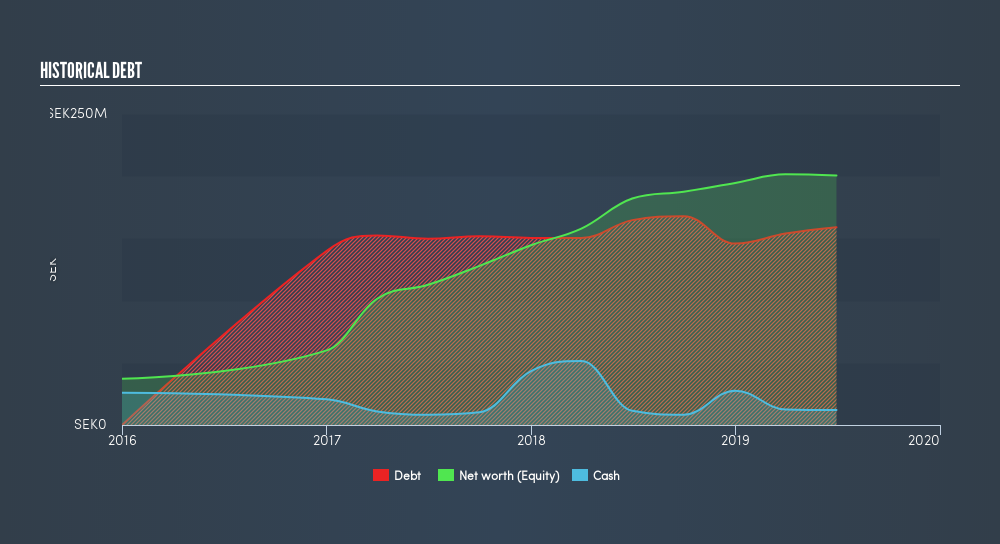

As you can see below, Alcadon Group had kr159.0m of debt, at June 2019, which is about the same the year before. You can click the chart for greater detail. However, it does have kr12.0m in cash offsetting this, leading to net debt of about kr147.0m.

A Look At Alcadon Group's Liabilities

Zooming in on the latest balance sheet data, we can see that Alcadon Group had liabilities of kr151.5m due within 12 months and liabilities of kr144.5m due beyond that. On the other hand, it had cash of kr12.0m and kr75.2m worth of receivables due within a year. So it has liabilities totalling kr208.8m more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of kr345.6m. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Alcadon Group has a debt to EBITDA ratio of 3.0 and its EBIT covered its interest expense 6.0 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Shareholders should be aware that Alcadon Group's EBIT was down 40% last year. If that decline continues then paying off debt will be harder than selling foie gras at a vegan convention. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Alcadon Group's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Alcadon Group produced sturdy free cash flow equating to 64% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Alcadon Group's struggle to grow its EBIT had us second guessing its balance sheet strength, but the other data-points we considered were relatively redeeming. For example, its conversion of EBIT to free cash flow is relatively strong. Taking the abovementioned factors together we do think Alcadon Group's debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. In light of our reservations about the company's balance sheet, it seems sensible to check if insiders have been selling shares recently.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About OM:ALCA

Alcadon Group

Provides data and telecommunication products and systems in Sweden, Norway, Denmark, Germany, the United Kingdom, and the Benelux.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.9% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|21.3% undervalued

TI

Community Contributor