Advertisement

Here's What Analysts Are Forecasting For Lime Technologies AB (publ) (STO:LIME) After Its Second-Quarter Results

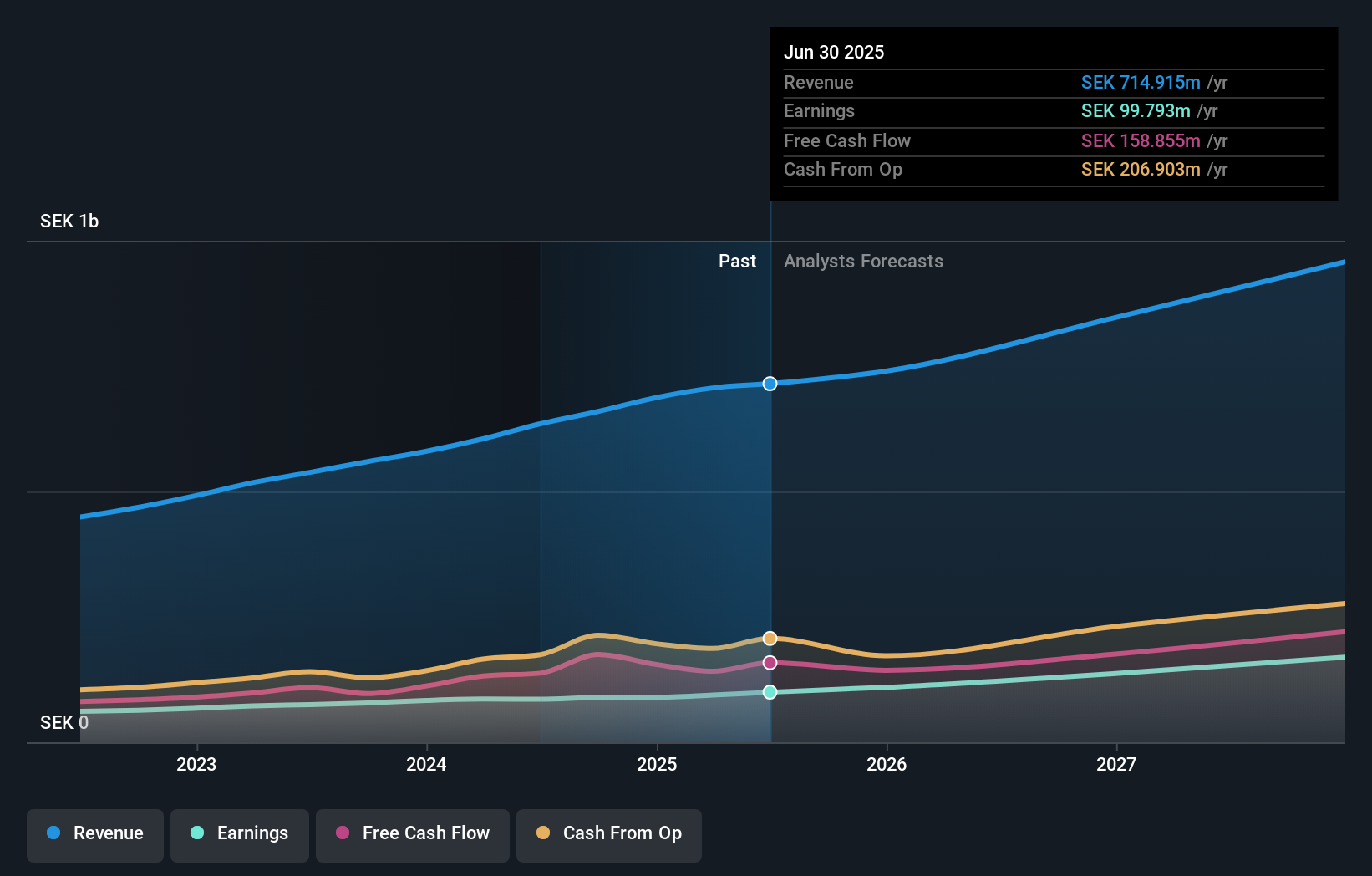

It's shaping up to be a tough period for Lime Technologies AB (publ) (STO:LIME), which a week ago released some disappointing quarterly results that could have a notable impact on how the market views the stock. Lime Technologies missed analyst forecasts, with revenues of kr183m and statutory earnings per share (EPS) of kr1.95, falling short by 3.3% and 3.8% respectively. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

Taking into account the latest results, the most recent consensus for Lime Technologies from five analysts is for revenues of kr740.0m in 2025. If met, it would imply a credible 3.5% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to increase 9.8% to kr8.25. Before this earnings report, the analysts had been forecasting revenues of kr756.4m and earnings per share (EPS) of kr8.37 in 2025. The consensus seems maybe a little more pessimistic, trimming their revenue forecasts after the latest results even though there was no change to its EPS estimates.

Check out our latest analysis for Lime Technologies

The average price target was steady at kr400even though revenue estimates declined; likely suggesting the analysts place a higher value on earnings. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values Lime Technologies at kr430 per share, while the most bearish prices it at kr380. This is a very narrow spread of estimates, implying either that Lime Technologies is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Lime Technologies' past performance and to peers in the same industry. It's pretty clear that there is an expectation that Lime Technologies' revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 7.1% growth on an annualised basis. This is compared to a historical growth rate of 17% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 13% annually. Factoring in the forecast slowdown in growth, it seems obvious that Lime Technologies is also expected to grow slower than other industry participants.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Unfortunately, they also downgraded their revenue estimates, and our data indicates underperformance compared to the wider industry. Even so, earnings per share are more important to the intrinsic value of the business. Even so, long term profitability is more important for the value creation process. The consensus price target held steady at kr400, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on Lime Technologies. Long-term earnings power is much more important than next year's profits. At Simply Wall St, we have a full range of analyst estimates for Lime Technologies going out to 2027, and you can see them free on our platform here..

It might also be worth considering whether Lime Technologies' debt load is appropriate, using our debt analysis tools on the Simply Wall St platform, here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:LIME

Lime Technologies

Lime Technologies AB (publ) software as a service (SaaS) based customer relationship management (CRM) solutions in the Nordic region.

Outstanding track record and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

31 followersusers have followed this narrative

2 commentsusers have commented on this narrative

15 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.2% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Vulcan Minerals ·

Uncovering The Hidden Annuity: Why Vulcan Minerals (TSXV:VUL) Trades At A Massive Discount To Its Sum-Of-The-Parts

Fair Value:CA$2.2378.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Rog on CTT - Correios De Portugal ·

Why CTT benefits in multiple ways right now

Fair Value:€7.6721.6% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Adecoagro ·

Why a "2026 Super El Nino" is the Ultimate Hedge for Tech-Heavy Portfolios

Fair Value:US$18.2849.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

60 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative