Advertisement

- Sweden

- /

- Specialty Stores

- /

- OM:CLAS B

Clas Ohlson AB (publ)'s (STO:CLAS B) 25% Jump Shows Its Popularity With Investors

Clas Ohlson AB (publ) (STO:CLAS B) shares have continued their recent momentum with a 25% gain in the last month alone. The annual gain comes to 125% following the latest surge, making investors sit up and take notice.

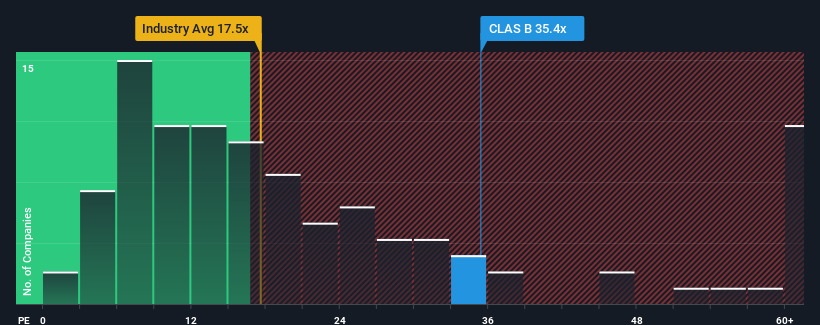

Since its price has surged higher, Clas Ohlson may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 35.4x, since almost half of all companies in Sweden have P/E ratios under 21x and even P/E's lower than 12x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

While the market has experienced earnings growth lately, Clas Ohlson's earnings have gone into reverse gear, which is not great. One possibility is that the P/E is high because investors think this poor earnings performance will turn the corner. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Clas Ohlson

What Are Growth Metrics Telling Us About The High P/E?

In order to justify its P/E ratio, Clas Ohlson would need to produce outstanding growth well in excess of the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 11%. This means it has also seen a slide in earnings over the longer-term as EPS is down 38% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 27% per annum during the coming three years according to the two analysts following the company. Meanwhile, the rest of the market is forecast to only expand by 13% per year, which is noticeably less attractive.

With this information, we can see why Clas Ohlson is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Clas Ohlson's P/E?

Shares in Clas Ohlson have built up some good momentum lately, which has really inflated its P/E. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Clas Ohlson's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Having said that, be aware Clas Ohlson is showing 1 warning sign in our investment analysis, you should know about.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:CLAS B

Clas Ohlson

A retail company, sells building, electrical, multimedia, home, and leisure products in Sweden, Norway, Finland, and internationally.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor