Advertisement

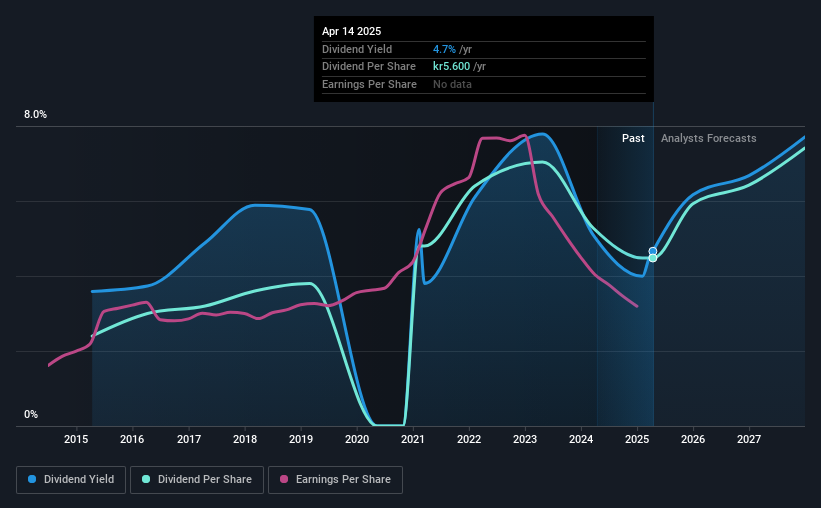

Bilia AB (publ)'s (STO:BILI A) dividend is being reduced from last year's payment covering the same period to SEK1.40 on the 5th of May. Despite the cut, the dividend yield of 4.7% will still be comparable to other companies in the industry.

Bilia's Projected Earnings Seem Likely To Cover Future Distributions

Solid dividend yields are great, but they only really help us if the payment is sustainable. Prior to this announcement, Bilia's dividend was making up a very large proportion of earnings and perhaps more concerning was that it was 156% of cash flows. Paying out such a high proportion of cash flows certainly exposes the company to cutting the dividend if cash flows were to reduce.

Over the next year, EPS is forecast to expand by 82.8%. Assuming the dividend continues along the course it has been charting recently, our estimates show the payout ratio being 53% which brings it into quite a comfortable range.

Check out our latest analysis for Bilia

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. Since 2015, the dividend has gone from SEK3.00 total annually to SEK5.60. This implies that the company grew its distributions at a yearly rate of about 6.4% over that duration. It's good to see the dividend growing at a decent rate, but the dividend has been cut at least once in the past. Bilia might have put its house in order since then, but we remain cautious.

Dividend Growth May Be Hard To Achieve

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. It's not great to see that Bilia's earnings per share has fallen at approximately 2.2% per year over the past five years. Declining earnings will inevitably lead to the company paying a lower dividend in line with lower profits. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

The Dividend Could Prove To Be Unreliable

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The payments are bit high to be considered sustainable, and the track record isn't the best. Overall, we don't think this company has the makings of a good income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. As an example, we've identified 3 warning signs for Bilia that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if Bilia might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:BILI A

Bilia

Operates as a full-service supplier for car ownership in Sweden, Norway, Luxemburg, and Belgium.

Good value with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor