- Sweden

- /

- Real Estate

- /

- OM:NYF

3 Undervalued Small Caps With Insider Action To Enhance Your Portfolio

Reviewed by Simply Wall St

As global markets continue to navigate geopolitical tensions and economic uncertainties, smaller-cap indexes have shown resilience by outperforming their larger counterparts. With the U.S. indexes approaching record highs and a strong labor market driving positive sentiment, small-cap stocks present intriguing opportunities for investors seeking diversification in their portfolios. In this environment, identifying stocks with solid fundamentals and potential insider action can be key to enhancing portfolio performance amidst fluctuating market conditions.

Top 10 Undervalued Small Caps With Insider Buying

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Paradeep Phosphates | 23.5x | 0.8x | 29.70% | ★★★★★☆ |

| Maharashtra Seamless | 9.8x | 1.7x | 36.49% | ★★★★★☆ |

| Calfrac Well Services | 12.2x | 0.2x | 33.62% | ★★★★★☆ |

| Nexus Industrial REIT | 13.0x | 3.3x | 25.73% | ★★★★★☆ |

| Avia Avian | 16.8x | 3.8x | 8.06% | ★★★★☆☆ |

| USCB Financial Holdings | 19.9x | 5.7x | 46.45% | ★★★☆☆☆ |

| Semen Indonesia (Persero) | 20.6x | 0.7x | 29.04% | ★★★☆☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

| THG | NA | 0.3x | -906.94% | ★★★☆☆☆ |

| Tilray Brands | NA | 1.5x | -80.99% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

UIE (CPSE:UIE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: UIE is an investment holding company primarily engaged in the palm oil industry through its significant ownership in United Plantations Berhad, with a market cap of DKK 8.65 billion.

Operations: The primary revenue stream is from UP, with recent quarterly revenue reaching $462.25 million. Notably, the gross profit margin has shown fluctuations, peaking at 78.82% in September 2023 and standing at 70.52% in September 2024. Operating expenses are a significant cost component, with general and administrative expenses consistently around $53.70 million in recent periods.

PE: 8.6x

UIE, a lesser-known player in its sector, showcases promising potential with recent financial improvements. The company reported third-quarter sales of US$128.52 million, up from US$115.36 million the previous year, and net income of US$32.2 million compared to a net loss previously. This growth reflects high-quality earnings despite one-off items affecting results. Insider confidence is evident with share purchases made throughout 2024, signaling optimism amidst higher-risk external borrowing as their sole funding source.

- Click here to discover the nuances of UIE with our detailed analytical valuation report.

Gain insights into UIE's historical performance by reviewing our past performance report.

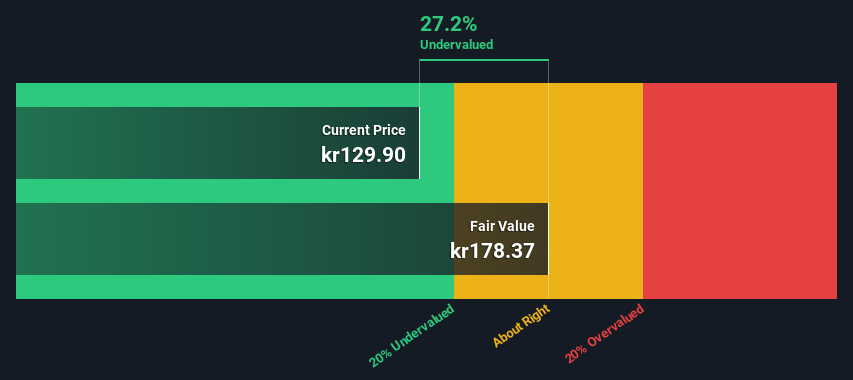

NOTE (OM:NOTE)

Simply Wall St Value Rating: ★★★★★☆

Overview: NOTE is a company engaged in manufacturing and supplying electronics to various industries, with a market cap of SEK 4.43 billion.

Operations: Revenue primarily comes from Western Europe (SEK 3.02 billion) and the Rest of World (SEK 988.44 million). The company's gross profit margin has shown variability, reaching a high of 13.48% in September 2023 before declining to 12.08% by December 2024. Operating expenses include significant allocations to sales and marketing as well as general and administrative functions, impacting overall profitability.

PE: 13.9x

NOTE, a company operating in a niche market, has seen its sales dip to SEK 809 million for Q3 2024 from SEK 1,034 million the previous year. Despite this decline, earnings are projected to grow by over 20% annually. The company relies entirely on external borrowing for funding, which introduces higher risk compared to customer deposits. Insider confidence is evident with recent share purchases in September and October 2024, suggesting potential growth optimism despite current challenges.

- Get an in-depth perspective on NOTE's performance by reading our valuation report here.

Assess NOTE's past performance with our detailed historical performance reports.

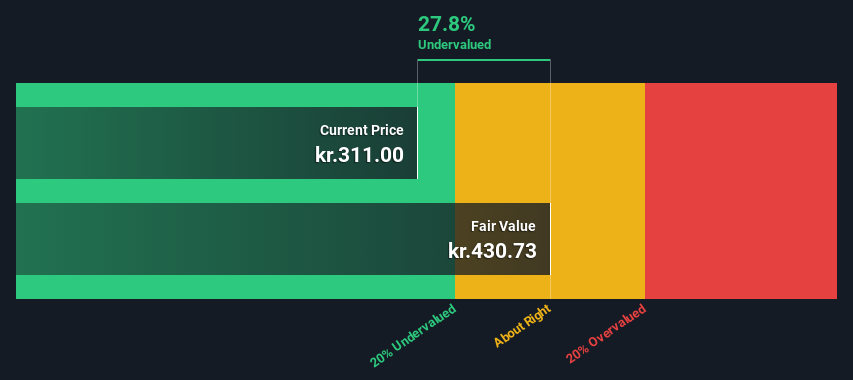

Nyfosa (OM:NYF)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Nyfosa is a real estate company focused on acquiring, managing, and developing commercial properties in Sweden and Finland with a market cap of SEK 15.25 billion.

Operations: The company generates revenue primarily from its Sweden and Kielo segments, with the Sweden segment contributing a larger share. Over recent periods, the gross profit margin has fluctuated, reaching 71.15% as of September 2024. Operating expenses and non-operating expenses have significantly impacted net income margins, which have been negative in several recent quarters.

PE: -23.7x

Nyfosa, a real estate company, is navigating transitional phases with a new CEO set to take charge in January 2025. Recent financial results show increased sales and revenue for the third quarter of 2024 compared to the previous year, despite reporting a net loss of SEK 122 million. The company has been active in debt financing, issuing SEK 500 million in green bonds while redeeming older bonds. These moves reflect strategic positioning amid leadership changes and challenging earnings coverage for interest payments.

- Click here and access our complete valuation analysis report to understand the dynamics of Nyfosa.

Explore historical data to track Nyfosa's performance over time in our Past section.

Seize The Opportunity

- Delve into our full catalog of 177 Undervalued Small Caps With Insider Buying here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Nyfosa, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nyfosa might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:NYF

Nyfosa

A transaction-intensive real estate company, invests, manages, develops, and sells properties in Sweden, Norway, and Finland.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Community Narratives