Analysts Expect Xbrane Biopharma AB (publ) (STO:XBRANE) To Breakeven Soon

We feel now is a pretty good time to analyse Xbrane Biopharma AB (publ)'s (STO:XBRANE) business as it appears the company may be on the cusp of a considerable accomplishment. Xbrane Biopharma AB (publ), a biotechnology company, engages in the development, manufacture, and sale of biosimilars. The kr271m market-cap company’s loss lessened since it announced a kr322m loss in the full financial year, compared to the latest trailing-twelve-month loss of kr305m, as it approaches breakeven. The most pressing concern for investors is Xbrane Biopharma's path to profitability – when will it breakeven? In this article, we will touch on the expectations for the company's growth and when analysts expect it to become profitable.

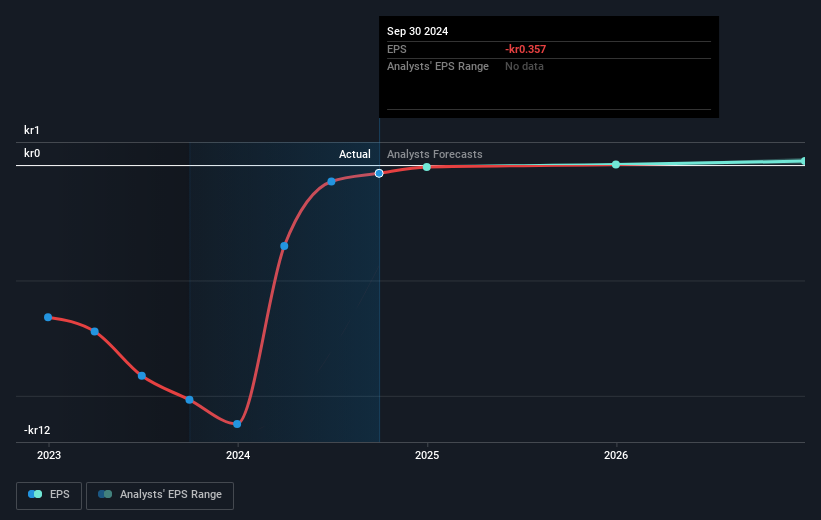

See our latest analysis for Xbrane Biopharma

According to the 2 industry analysts covering Xbrane Biopharma, the consensus is that breakeven is near. They expect the company to post a final loss in 2024, before turning a profit of kr40m in 2025. Therefore, the company is expected to breakeven roughly 12 months from now or less. How fast will the company have to grow to reach the consensus forecasts that anticipate breakeven by 2025? Working backwards from analyst estimates, it turns out that they expect the company to grow 128% year-on-year, on average, which signals high confidence from analysts. If this rate turns out to be too aggressive, the company may become profitable much later than analysts predict.

Underlying developments driving Xbrane Biopharma's growth isn’t the focus of this broad overview, but, take into account that typically a biotech has lumpy cash flows which are contingent on the product type and stage of development the company is in. This means, large upcoming growth rates are not abnormal as the company is beginning to reap the benefits of earlier investments.

Before we wrap up, there’s one issue worth mentioning. Xbrane Biopharma currently has a relatively high level of debt. Typically, debt shouldn’t exceed 40% of your equity, which in Xbrane Biopharma's case is 48%. A higher level of debt requires more stringent capital management which increases the risk in investing in the loss-making company.

Next Steps:

There are too many aspects of Xbrane Biopharma to cover in one brief article, but the key fundamentals for the company can all be found in one place – Xbrane Biopharma's company page on Simply Wall St. We've also compiled a list of pertinent factors you should further examine:

- Historical Track Record: What has Xbrane Biopharma's performance been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Xbrane Biopharma's board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

If you're looking to trade Xbrane Biopharma, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:XBRANE

Xbrane Biopharma

A biotechnology company, engages in the development, manufacture, and sale of biosimilars.

Exceptional growth potential and fair value.

Similar Companies

Market Insights

Community Narratives