- Sweden

- /

- Life Sciences

- /

- OM:PRO

Here's Why We're Not Too Worried About Promimic's (STO:PRO) Cash Burn Situation

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, Promimic (STO:PRO) shareholders have done very well over the last year, with the share price soaring by 149%. But while the successes are well known, investors should not ignore the very many unprofitable companies that simply burn through all their cash and collapse.

Given its strong share price performance, we think it's worthwhile for Promimic shareholders to consider whether its cash burn is concerning. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

See our latest analysis for Promimic

Does Promimic Have A Long Cash Runway?

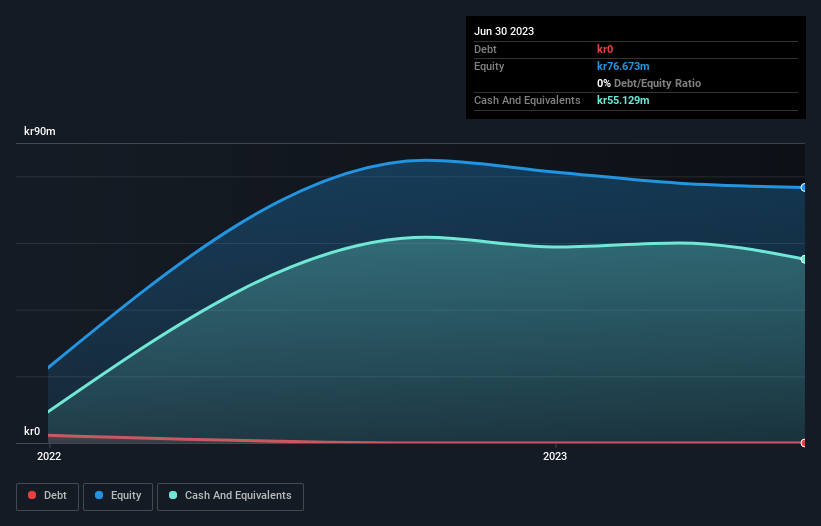

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. When Promimic last reported its balance sheet in June 2023, it had zero debt and cash worth kr55m. Looking at the last year, the company burnt through kr20m. That means it had a cash runway of about 2.8 years as of June 2023. Arguably, that's a prudent and sensible length of runway to have. Depicted below, you can see how its cash holdings have changed over time.

How Well Is Promimic Growing?

Some investors might find it troubling that Promimic is actually increasing its cash burn, which is up 30% in the last year. Given that its operating revenue increased 102% in that time, it seems the company has reason to think its expenditure is working well to drive growth. If that revenue does keep flowing reliably, then the company could see a strong improvement in free cash flow simply by reducing growth expenditure. It seems to be growing nicely. Of course, we've only taken a quick look at the stock's growth metrics, here. You can take a look at how Promimic is growing revenue over time by checking this visualization of past revenue growth.

How Easily Can Promimic Raise Cash?

There's no doubt Promimic seems to be in a fairly good position, when it comes to managing its cash burn, but even if it's only hypothetical, it's always worth asking how easily it could raise more money to fund growth. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Commonly, a business will sell new shares in itself to raise cash and drive growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of kr551m, Promimic's kr20m in cash burn equates to about 3.6% of its market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

So, Should We Worry About Promimic's Cash Burn?

As you can probably tell by now, we're not too worried about Promimic's cash burn. In particular, we think its revenue growth stands out as evidence that the company is well on top of its spending. While its increasing cash burn wasn't great, the other factors mentioned in this article more than make up for weakness on that measure. Looking at all the measures in this article, together, we're not worried about its rate of cash burn; the company seems well on top of its medium-term spending needs. Readers need to have a sound understanding of business risks before investing in a stock, and we've spotted 4 warning signs for Promimic that potential shareholders should take into account before putting money into a stock.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

If you're looking to trade Promimic, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:PRO

Promimic

Manufactures, markets, and sells biomaterials for improved osseointegration for orthopedic and dental implants markets.

Flawless balance sheet low.

Market Insights

Community Narratives