Rock star Growth Puts Hansa Biopharma (STO:HNSA) In A Position To Use Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Hansa Biopharma AB (publ) (STO:HNSA) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Hansa Biopharma

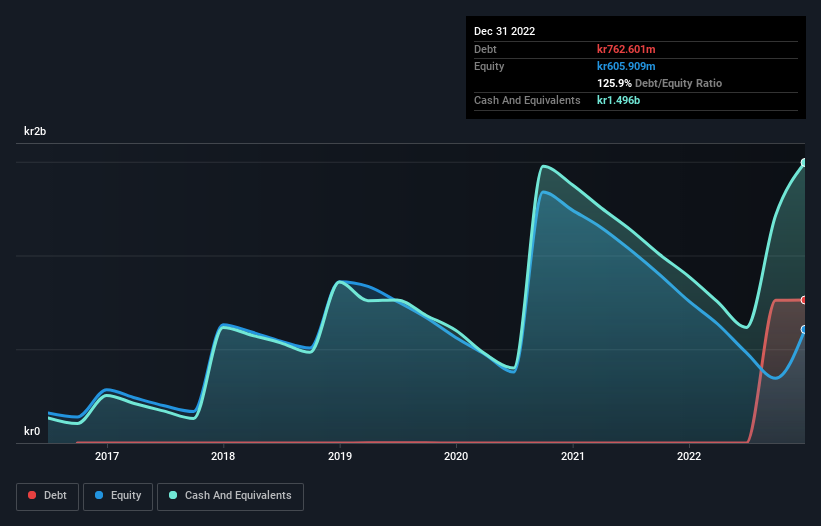

What Is Hansa Biopharma's Net Debt?

You can click the graphic below for the historical numbers, but it shows that as of December 2022 Hansa Biopharma had kr762.6m of debt, an increase on none, over one year. But on the other hand it also has kr1.50b in cash, leading to a kr733.6m net cash position.

A Look At Hansa Biopharma's Liabilities

Zooming in on the latest balance sheet data, we can see that Hansa Biopharma had liabilities of kr261.7m due within 12 months and liabilities of kr819.8m due beyond that. Offsetting these obligations, it had cash of kr1.50b as well as receivables valued at kr107.6m due within 12 months. So it actually has kr522.2m more liquid assets than total liabilities.

This excess liquidity suggests that Hansa Biopharma is taking a careful approach to debt. Because it has plenty of assets, it is unlikely to have trouble with its lenders. Simply put, the fact that Hansa Biopharma has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Hansa Biopharma's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Hansa Biopharma wasn't profitable at an EBIT level, but managed to grow its revenue by 356%, to kr155m. That's virtually the hole-in-one of revenue growth!

So How Risky Is Hansa Biopharma?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Hansa Biopharma had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of kr508m and booked a kr610m accounting loss. However, it has net cash of kr733.6m, so it has a bit of time before it will need more capital. The good news for shareholders is that Hansa Biopharma has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. High growth pre-profit companies may well be risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 3 warning signs with Hansa Biopharma , and understanding them should be part of your investment process.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you're looking to trade Hansa Biopharma, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hansa Biopharma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:HNSA

Hansa Biopharma

A biopharmaceutical company, engages in development and commercialization of treatments for patients with rare immunological conditions in Europe and the United States.

Moderate and slightly overvalued.