Stock Analysis

Swedish Exchange Highlights: Three Stocks Estimated To Be Undervalued In July 2024

Reviewed by Simply Wall St

Amidst a backdrop of global economic fluctuations and trade tensions, the Swedish stock market presents unique opportunities for investors looking for value. As markets worldwide show mixed responses to macroeconomic signals, understanding the intrinsic worth of stocks becomes crucial in identifying potential investment opportunities in Sweden.

Top 10 Undervalued Stocks Based On Cash Flows In Sweden

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Gränges (OM:GRNG) | SEK135.40 | SEK262.03 | 48.3% |

| Husqvarna (OM:HUSQ B) | SEK73.30 | SEK143.16 | 48.8% |

| Nordic Waterproofing Holding (OM:NWG) | SEK160.60 | SEK314.20 | 48.9% |

| Scandi Standard (OM:SCST) | SEK78.20 | SEK145.57 | 46.3% |

| Volati (OM:VOLO) | SEK120.00 | SEK236.12 | 49.2% |

| RaySearch Laboratories (OM:RAY B) | SEK141.40 | SEK278.06 | 49.1% |

| TF Bank (OM:TFBANK) | SEK267.00 | SEK519.05 | 48.6% |

| Cavotec (OM:CCC) | SEK20.90 | SEK37.94 | 44.9% |

| Nordisk Bergteknik (OM:NORB B) | SEK16.70 | SEK30.80 | 45.8% |

| Bactiguard Holding (OM:BACTI B) | SEK70.20 | SEK132.35 | 47% |

Let's dive into some prime choices out of from the screener.

Billerud (OM:BILL)

Overview: Billerud AB (publ) is a global provider of paper and packaging materials, with a market capitalization of approximately SEK 26.91 billion.

Operations: Billerud's revenue is primarily generated from Europe and North America, totaling SEK 27.08 billion and SEK 11.35 billion respectively, along with an additional SEK 2.77 billion from various solutions and services excluding currency hedging activities.

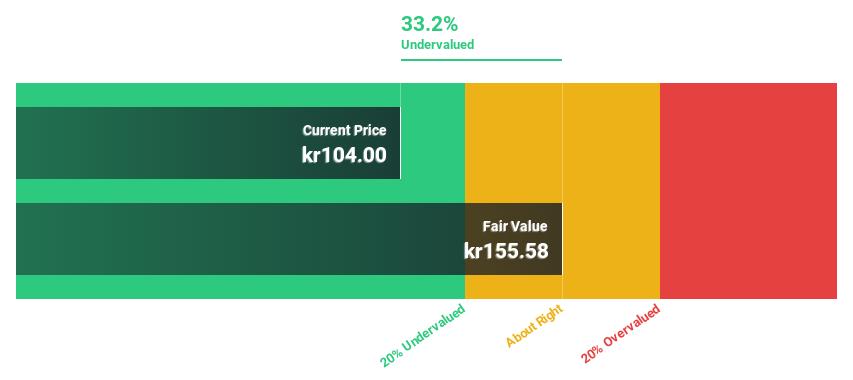

Estimated Discount To Fair Value: 22.4%

Billerud is currently priced at SEK108.2, which is 22.4% below our calculated fair value of SEK139.48, indicating that it may be undervalued. Despite a low return on equity forecast of 8.6%, Billerud's earnings are expected to grow by 32.3% annually over the next three years, outpacing the Swedish market's average of 15.3%. Recent financials show a rebound with second-quarter sales up to SEK10.76 billion from SEK9.95 billion last year and a net income turnaround to SEK63 million from a loss of SEK481 million in the same period last year.

- Our earnings growth report unveils the potential for significant increases in Billerud's future results.

- Click here to discover the nuances of Billerud with our detailed financial health report.

Lindab International (OM:LIAB)

Overview: Lindab International AB, a company based in Europe, specializes in manufacturing and selling products and solutions for ventilation systems, with a market capitalization of approximately SEK 19.87 billion.

Operations: The company generates revenue primarily through two segments: Profile Systems, which brought in SEK 3.28 billion, and Ventilation Systems, contributing SEK 9.95 billion.

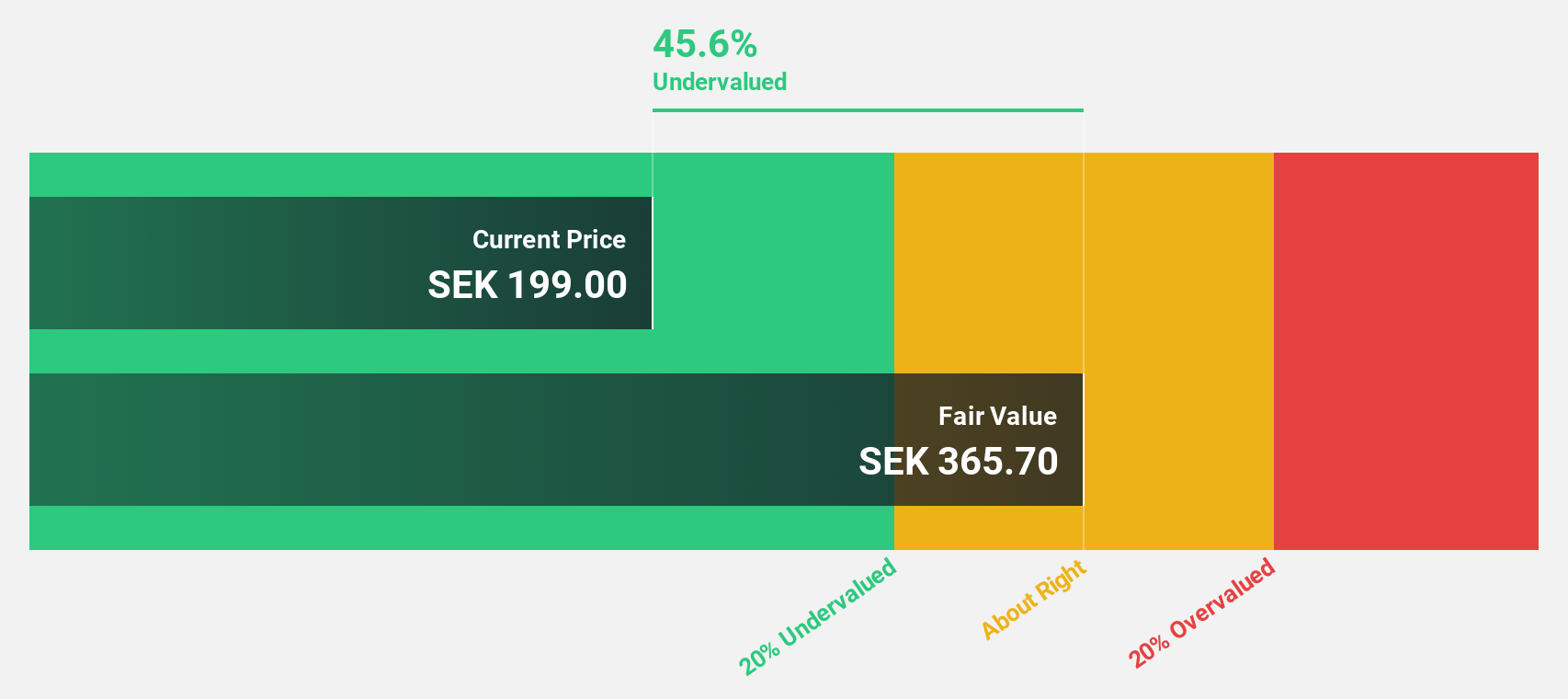

Estimated Discount To Fair Value: 44.9%

Lindab International, with a current trading price of SEK258.6 against a fair value estimate of SEK468.93, appears significantly undervalued based on discounted cash flow analysis, suggesting over 44.9% potential upside. Despite this, its recent performance shows a dip in net income and EPS in the latest quarters compared to the previous year. However, earnings are projected to grow by 25.73% annually over the next three years, outstripping the Swedish market's growth forecast of 15.3%. This robust earnings growth outlook coupled with a strategic sales target of SEK 20 billion by 2027 underscores potential despite recent underwhelming profit figures and an unstable dividend track record.

- Our expertly prepared growth report on Lindab International implies its future financial outlook may be stronger than recent results.

- Click here and access our complete balance sheet health report to understand the dynamics of Lindab International.

Sweco (OM:SWEC B)

Overview: Sweco AB (publ) offers architecture and engineering consultancy services globally, with a market capitalization of approximately SEK 61.14 billion.

Operations: Sweco's revenue is generated from various regional segments, with Sweden contributing SEK 8.74 billion, Norway SEK 3.50 billion, Belgium SEK 3.97 billion, Denmark SEK 3.24 billion, Finland SECk 3.67 billion, the Netherlands SEK 3.00 billion, and Germany & Central Europe providing SEK 2.71 billion.

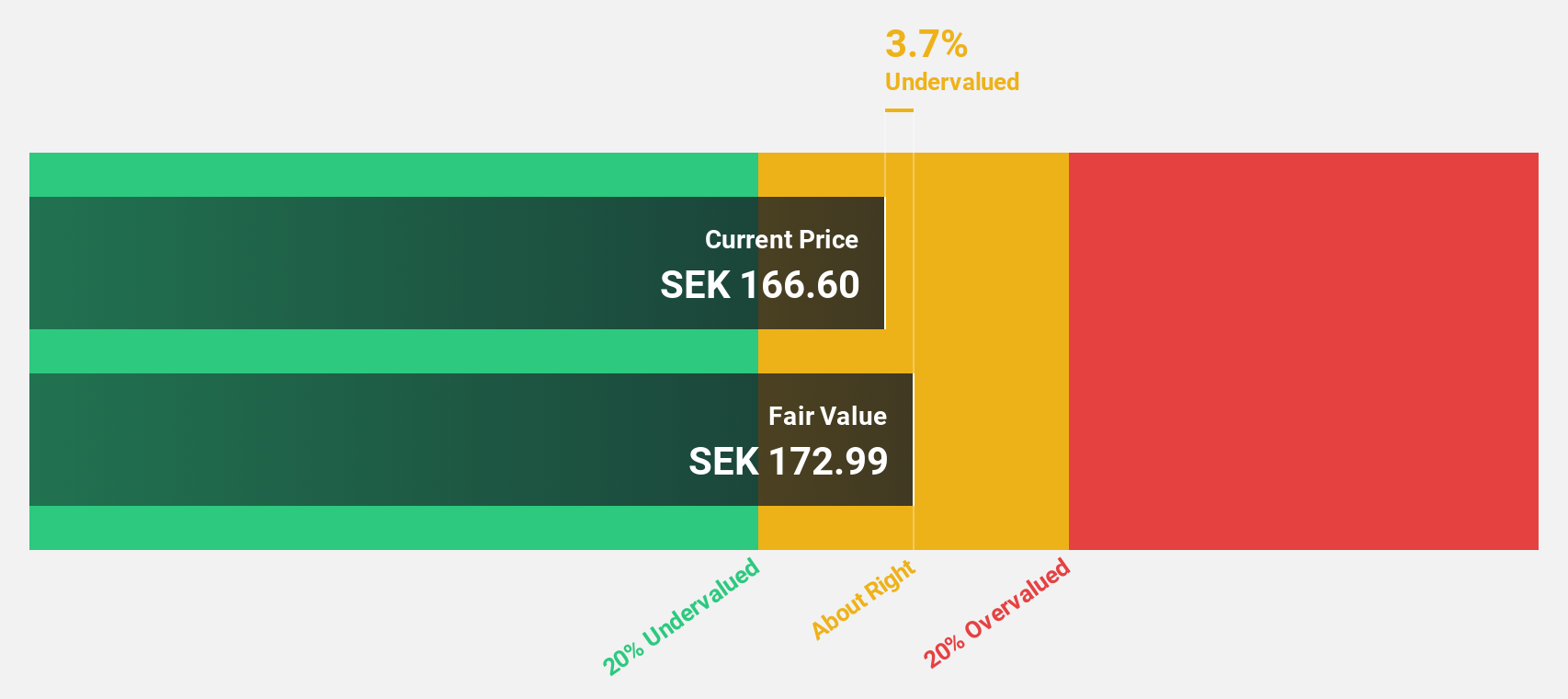

Estimated Discount To Fair Value: 17.5%

Sweco, trading at SEK 169.90, is valued below its fair value of SEK 205.89, reflecting a modest undervaluation based on discounted cash flow analysis. Recent earnings show a solid increase with Q2 net income rising to SEK 540 million from SEK 357 million year-over-year and significant contracts like the SEK 400 million East Coast Line expansion enhancing future revenue prospects. While Sweco's earnings are expected to grow by 17.31% annually, surpassing the Swedish market's forecast of 15.3%, its dividend track record remains unstable, posing a caution for yield-focused investors.

- Our growth report here indicates Sweco may be poised for an improving outlook.

- Navigate through the intricacies of Sweco with our comprehensive financial health report here.

Where To Now?

- Get an in-depth perspective on all 46 Undervalued Swedish Stocks Based On Cash Flows by using our screener here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Billerud might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:BILL

Flawless balance sheet with reasonable growth potential.