- Sweden

- /

- Household Products

- /

- OM:ESGR B

The Price Is Right For ES Energy Save Holding AB (publ) (STO:ESGR B) Even After Diving 25%

The ES Energy Save Holding AB (publ) (STO:ESGR B) share price has fared very poorly over the last month, falling by a substantial 25%. For any long-term shareholders, the last month ends a year to forget by locking in a 76% share price decline.

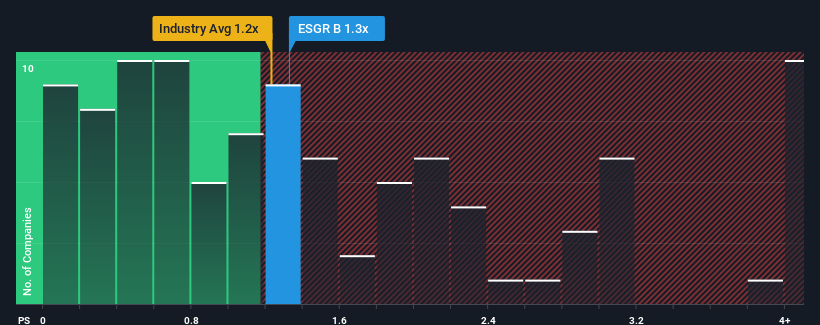

Although its price has dipped substantially, when almost half of the companies in Sweden's Household Products industry have price-to-sales ratios (or "P/S") below 0.6x, you may still consider ES Energy Save Holding as a stock probably not worth researching with its 1.3x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for ES Energy Save Holding

What Does ES Energy Save Holding's P/S Mean For Shareholders?

ES Energy Save Holding could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the market is expecting the poor revenue to reverse, justifying it's current high P/S.. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Keen to find out how analysts think ES Energy Save Holding's future stacks up against the industry? In that case, our free report is a great place to start.Is There Enough Revenue Growth Forecasted For ES Energy Save Holding?

In order to justify its P/S ratio, ES Energy Save Holding would need to produce impressive growth in excess of the industry.

Retrospectively, the last year delivered a frustrating 41% decrease to the company's top line. However, a few very strong years before that means that it was still able to grow revenue by an impressive 189% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

Shifting to the future, estimates from the one analyst covering the company suggest revenue growth will be highly resilient over the next year growing by 127%. With the rest of the industry predicted to shrink by 0.1%, that would be a fantastic result.

In light of this, it's understandable that ES Energy Save Holding's P/S sits above the majority of other companies. Right now, investors are willing to pay more for a stock that is shaping up to buck the trend of the broader industry going backwards.

What We Can Learn From ES Energy Save Holding's P/S?

ES Energy Save Holding's P/S remain high even after its stock plunged. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We can see that ES Energy Save Holding maintains its high P/S on the strength of its forecast growth potentially beating a struggling industry, as expected. Outperforming the industry in this manner looks to have provided investors with a bit of confidence that the future will be bright, bolstering the P/S. Questions could still raised over whether this level of outperformance can continue in the context of a a tumultuous industry climate. Although, if the company's prospects don't change they will continue to provide strong support to the share price.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for ES Energy Save Holding that you should be aware of.

If these risks are making you reconsider your opinion on ES Energy Save Holding, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if ES Energy Save Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:ESGR B

Flawless balance sheet with high growth potential.

Market Insights

Community Narratives