Advertisement

- Sweden

- /

- Healthcare Services

- /

- OM:EQL

EQL Pharma AB (publ) (STO:EQL) Shares Slammed 26% But Getting In Cheap Might Be Difficult Regardless

EQL Pharma AB (publ) (STO:EQL) shareholders that were waiting for something to happen have been dealt a blow with a 26% share price drop in the last month. Indeed, the recent drop has reduced its annual gain to a relatively sedate 8.8% over the last twelve months.

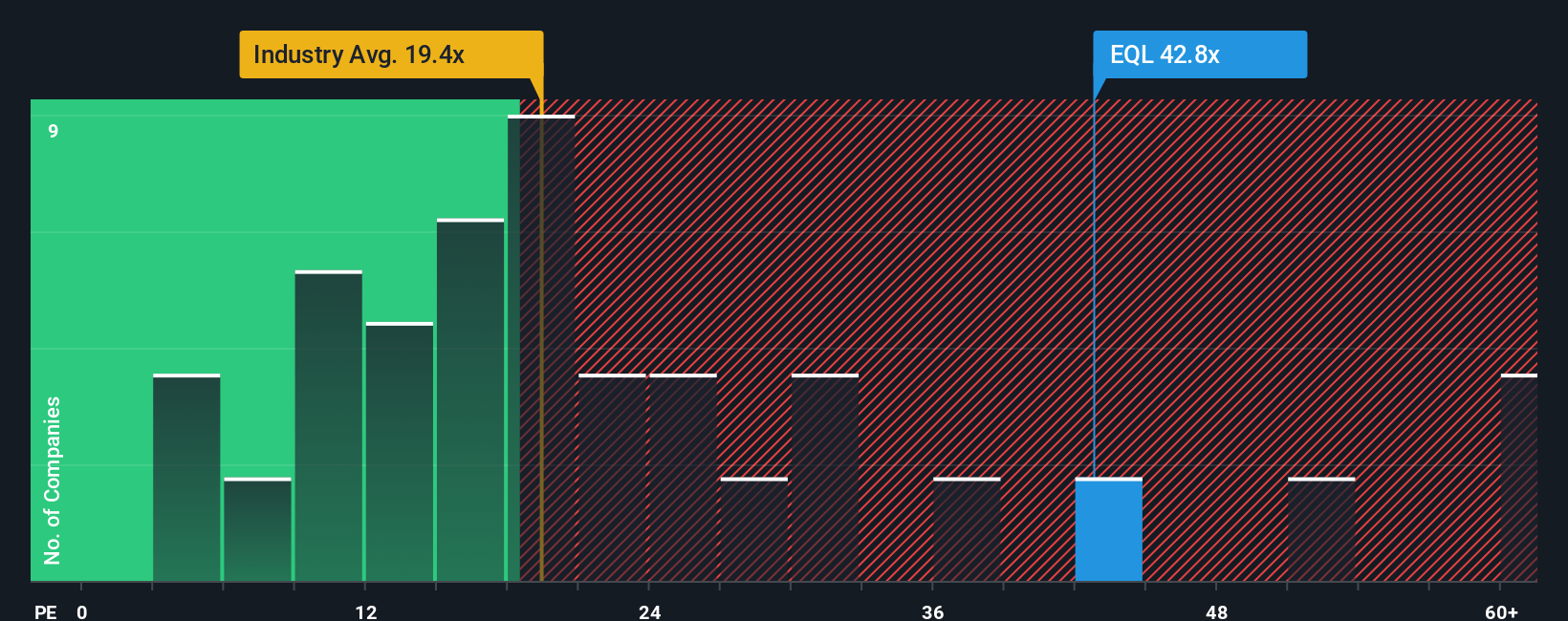

Even after such a large drop in price, EQL Pharma's price-to-earnings (or "P/E") ratio of 42.8x might still make it look like a strong sell right now compared to the market in Sweden, where around half of the companies have P/E ratios below 23x and even P/E's below 14x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

EQL Pharma certainly has been doing a good job lately as it's been growing earnings more than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for EQL Pharma

Does Growth Match The High P/E?

In order to justify its P/E ratio, EQL Pharma would need to produce outstanding growth well in excess of the market.

If we review the last year of earnings growth, the company posted a terrific increase of 62%. The latest three year period has also seen a 15% overall rise in EPS, aided extensively by its short-term performance. Therefore, it's fair to say the earnings growth recently has been respectable for the company.

Turning to the outlook, the next three years should generate growth of 36% per year as estimated by the lone analyst watching the company. That's shaping up to be materially higher than the 17% per year growth forecast for the broader market.

With this information, we can see why EQL Pharma is trading at such a high P/E compared to the market. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On EQL Pharma's P/E

A significant share price dive has done very little to deflate EQL Pharma's very lofty P/E. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of EQL Pharma's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Having said that, be aware EQL Pharma is showing 3 warning signs in our investment analysis, and 2 of those can't be ignored.

If these risks are making you reconsider your opinion on EQL Pharma, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if EQL Pharma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:EQL

EQL Pharma

Engages in the development, marketing, and sale of generic medicines to pharmacies and hospitals in Sweden, Denmark, Norway, Finland, and the rest of Europe.

Exceptional growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor