Advertisement

Cheffelo AB (publ) (STO:CHEF) Stock Rockets 28% But Many Are Still Ignoring The Company

Despite an already strong run, Cheffelo AB (publ) (STO:CHEF) shares have been powering on, with a gain of 28% in the last thirty days. The annual gain comes to 234% following the latest surge, making investors sit up and take notice.

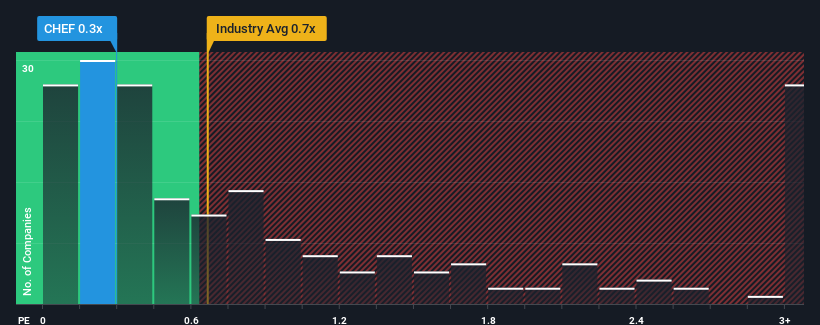

In spite of the firm bounce in price, you could still be forgiven for feeling indifferent about Cheffelo's P/S ratio of 0.3x, since the median price-to-sales (or "P/S") ratio for the Food industry in Sweden is also close to 0.5x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

See our latest analysis for Cheffelo

What Does Cheffelo's Recent Performance Look Like?

The recently shrinking revenue for Cheffelo has been in line with the industry. It seems that few are expecting the company's revenue performance to deviate much from most other companies, which has held the P/S back. You'd much rather the company improve its revenue if you still believe in the business. In saying that, existing shareholders probably aren't too pessimistic about the share price if the company's revenue continues tracking the industry.

Keen to find out how analysts think Cheffelo's future stacks up against the industry? In that case, our free report is a great place to start.Is There Some Revenue Growth Forecasted For Cheffelo?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Cheffelo's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 7.3% decrease to the company's top line. The last three years don't look nice either as the company has shrunk revenue by 18% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 6.5% per year during the coming three years according to the two analysts following the company. Meanwhile, the rest of the industry is forecast to only expand by 1.6% each year, which is noticeably less attractive.

In light of this, it's curious that Cheffelo's P/S sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Final Word

Cheffelo appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Looking at Cheffelo's analyst forecasts revealed that its superior revenue outlook isn't giving the boost to its P/S that we would've expected. Perhaps uncertainty in the revenue forecasts are what's keeping the P/S ratio consistent with the rest of the industry. At least the risk of a price drop looks to be subdued, but investors seem to think future revenue could see some volatility.

Plus, you should also learn about this 1 warning sign we've spotted with Cheffelo.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:CHEF

Cheffelo

Engages in the supply and delivery of meal kits to various customers in Sweden, Norway, and Denmark.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor