- South Korea

- /

- Electronic Equipment and Components

- /

- KOSDAQ:A025320

Synopex And 2 Other Undiscovered Gems To Enhance Your Portfolio

Reviewed by Simply Wall St

As global markets show signs of recovery with smaller-cap indexes outperforming their larger counterparts, investors are keenly observing the economic indicators that could impact small-cap companies. Amidst this backdrop, discovering lesser-known stocks with strong fundamentals and growth potential can be a strategic move to diversify and enhance a portfolio.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Canal Shipping Agencies | NA | 8.92% | 22.01% | ★★★★★★ |

| Zambia Sugar | 1.04% | 20.60% | 44.34% | ★★★★★★ |

| Suez Canal Company for Technology Settling (S.A.E) | NA | 22.31% | 13.60% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| La Forestière Equatoriale | NA | -58.49% | 45.78% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Infinity Capital Investments | NA | 9.92% | 22.16% | ★★★★★☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

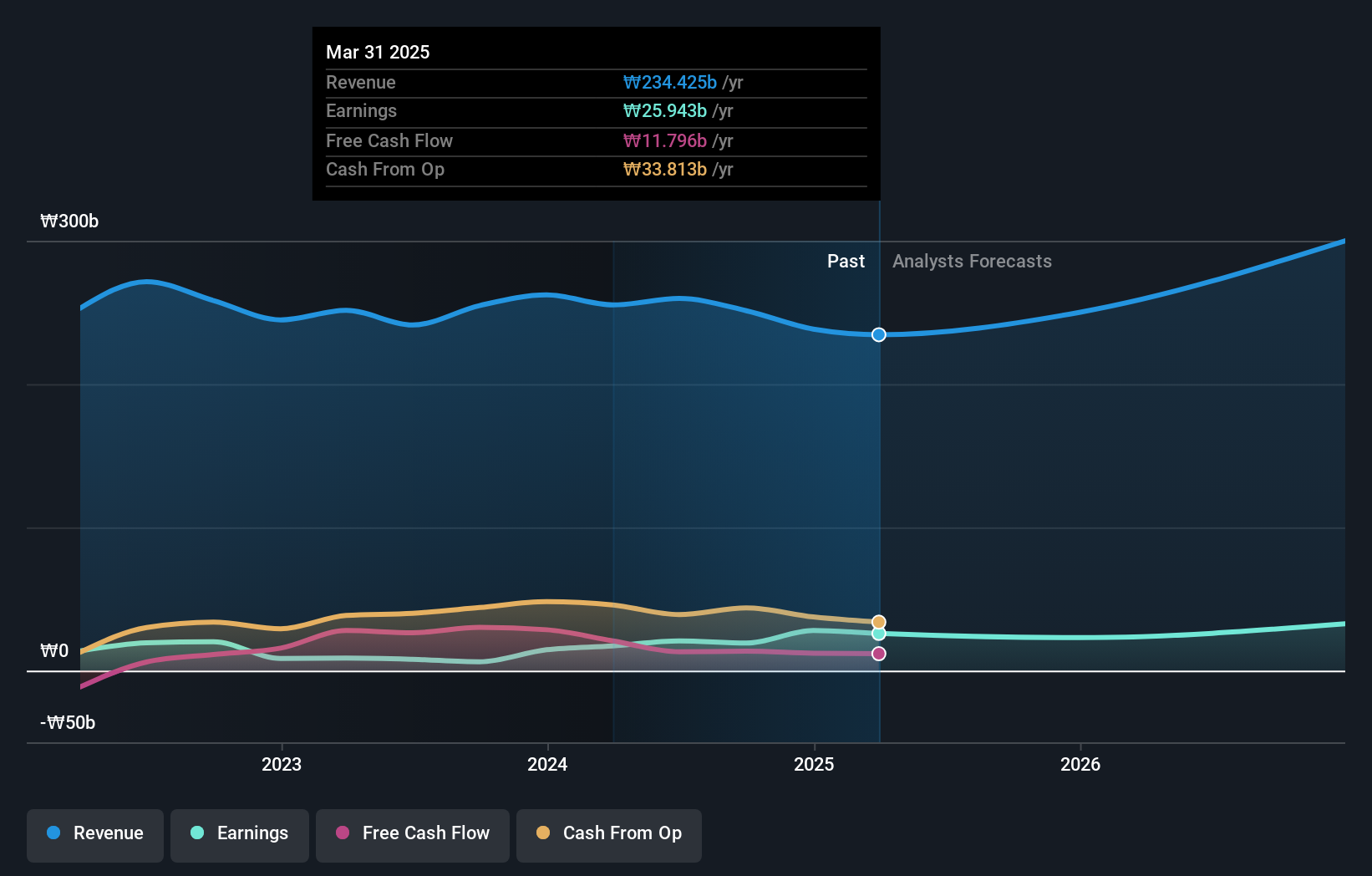

Synopex (KOSDAQ:A025320)

Simply Wall St Value Rating: ★★★★★★

Overview: Synopex Inc. is a company that manufactures and sells flexible printed circuit board (FPCB) products and electronic components both in South Korea and internationally, with a market capitalization of ₩526.12 billion.

Operations: Synopex's revenue is primarily derived from the sale of flexible printed circuit board (FPCB) products and electronic components.

Synopex's recent performance highlights its potential as an intriguing investment, with earnings growth outpacing the electronics industry at 212.9%. The company has successfully reduced its debt-to-equity ratio from 55% to 22.3% over five years, indicating improved financial health. Despite a drop in quarterly sales to KRW 59,686 million from KRW 68,213 million last year, net income for the nine months rose to KRW 15 billion compared to KRW 10 billion previously. Synopex also boasts high-quality earnings and robust interest coverage of EBIT at a multiple of nearly forty-four times its interest payments.

- Dive into the specifics of Synopex here with our thorough health report.

Gain insights into Synopex's historical performance by reviewing our past performance report.

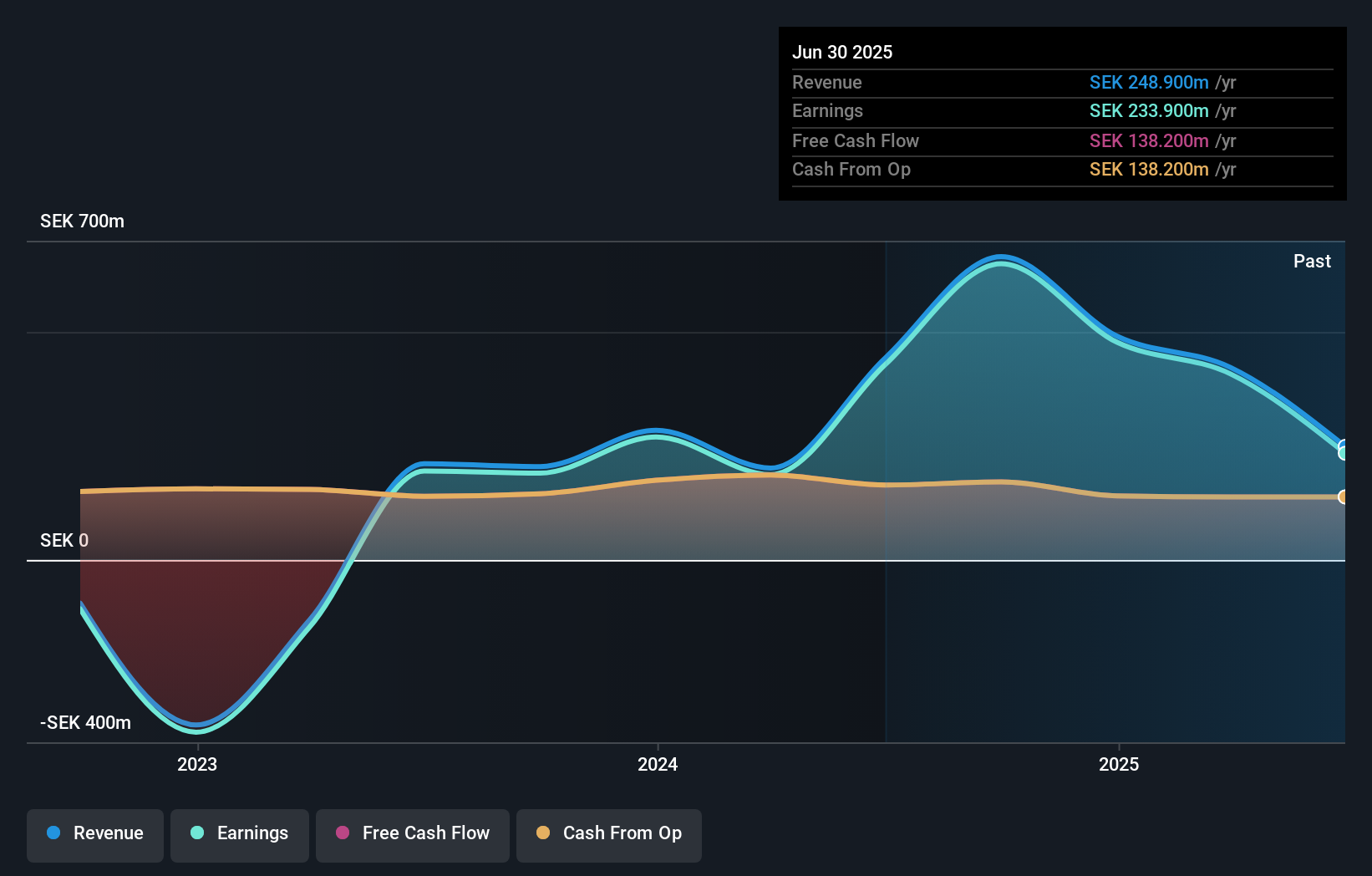

AB Traction (OM:TRAC B)

Simply Wall St Value Rating: ★★★★★★

Overview: AB Traction is a private equity firm that focuses on distressed, middle market, later stage, mature, bridge, recapitalization, buyouts and PIPES investments with a market cap of SEK4.22 billion.

Operations: The firm generates revenue primarily from active listed holdings (SEK275.60 million) and financial investments (SEK309.80 million), with a smaller contribution from unlisted holdings (SEK79.30 million).

AB Traction showcases a strong financial turnaround, reporting a net income of SEK 10.7 million for Q3 2024, compared to a hefty net loss of SEK 210 million the previous year. This improvement is reflected in basic earnings per share from continuing operations at SEK 0.72, up from a loss per share of SEK 14.2 last year. Over the past year, earnings have surged by an impressive 241%, outpacing industry growth significantly. The company operates debt-free and is trading at approximately 7.8% below its estimated fair value, indicating potential undervaluation in the market context as it continues to grow profitably without debt concerns.

- Unlock comprehensive insights into our analysis of AB Traction stock in this health report.

Explore historical data to track AB Traction's performance over time in our Past section.

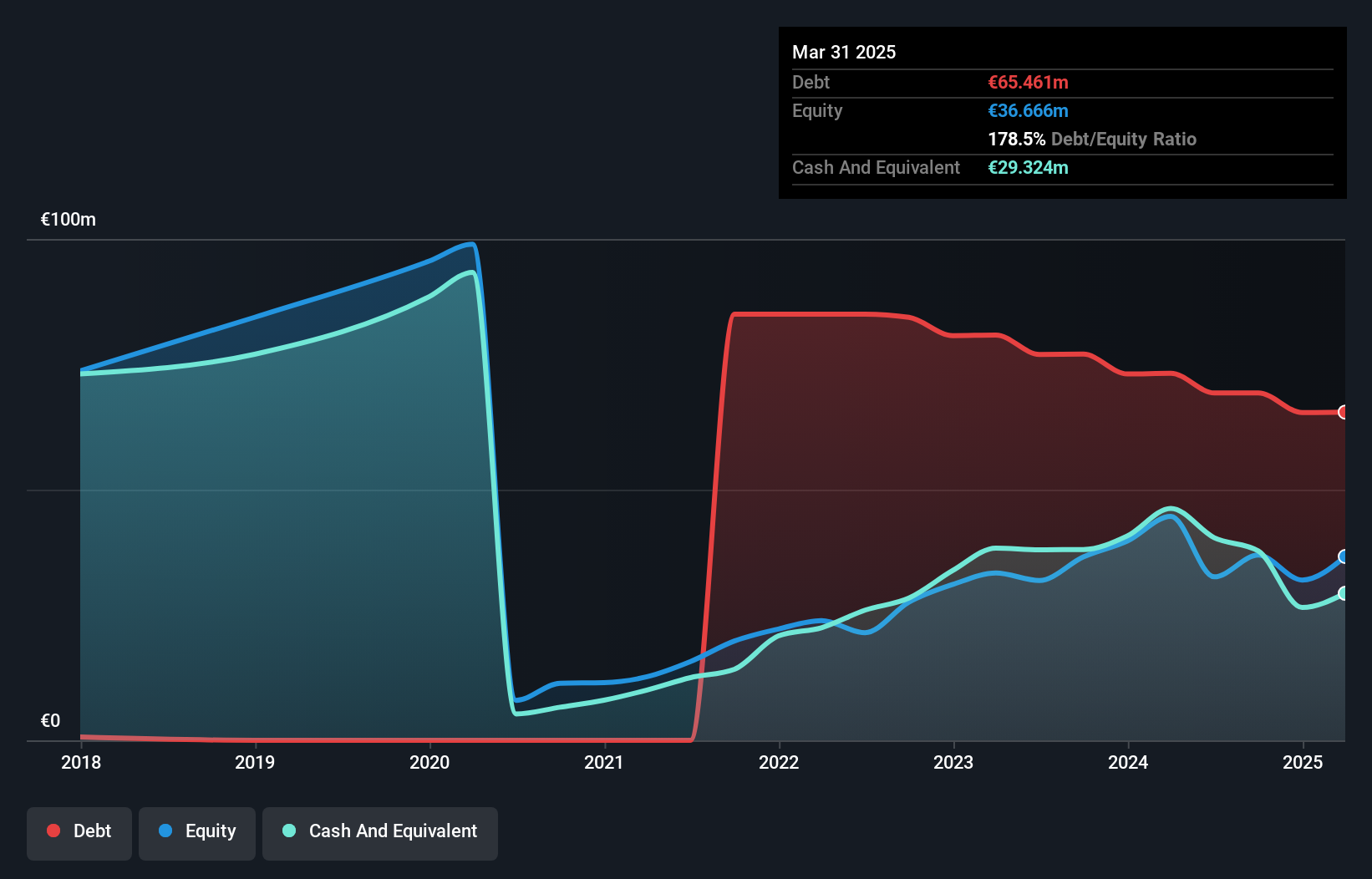

PharmaSGP Holding (XTRA:PSG)

Simply Wall St Value Rating: ★★★★★☆

Overview: PharmaSGP Holding SE is a company that produces and distributes over-the-counter drugs and healthcare products in Germany, with a market capitalization of €304.55 million.

Operations: PharmaSGP Holding SE generates revenue primarily from its pharmaceuticals segment, totaling €109.76 million.

PharmaSGP Holding, a modestly sized player in the pharmaceutical sector, has shown financial resilience with positive shareholder equity after five years of improvement. Trading at 73% below its estimated fair value, it seems undervalued. Over the past five years, earnings have grown by 3% annually and are expected to increase by nearly 14% per year moving forward. The company's net debt to equity ratio is high at 89%, yet interest payments are well covered with an EBIT coverage of over eight times. Recent half-year results show sales climbing to €58 million from €50 million last year, while net income rose to €8.68 million from €6.86 million, indicating robust performance despite industry challenges.

- Click to explore a detailed breakdown of our findings in PharmaSGP Holding's health report.

Assess PharmaSGP Holding's past performance with our detailed historical performance reports.

Make It Happen

- Discover the full array of 4638 Undiscovered Gems With Strong Fundamentals right here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A025320

Synopex

Manufactures and sells FPCB products and electronic components in South Korea and internationally.

Flawless balance sheet with solid track record.

Market Insights

Community Narratives