Advertisement

EQT AB (publ)'s (STO:EQT) dividend will be increasing from last year's payment of the same period to €1.80 on 3rd of June. This takes the annual payment to 1.0% of the current stock price, which unfortunately is below what the industry is paying.

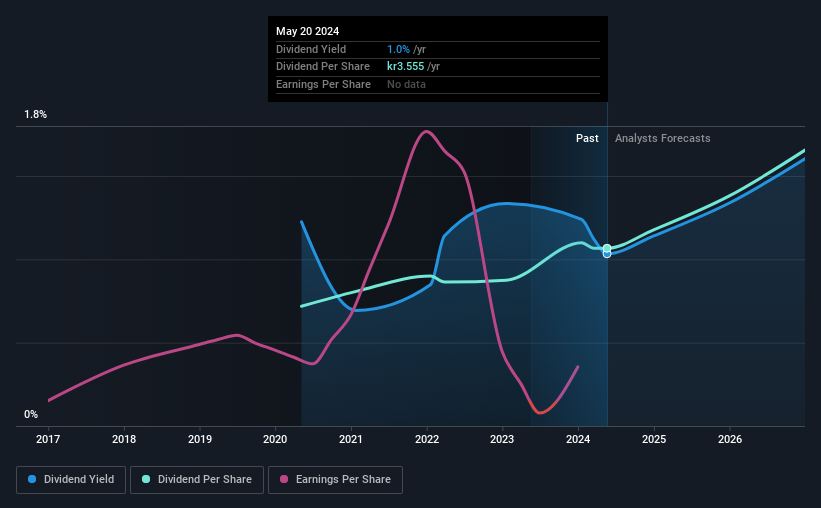

View our latest analysis for EQT

EQT Doesn't Earn Enough To Cover Its Payments

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. Before making this announcement, EQT's dividend was higher than its profits, but the free cash flows quite comfortably covered it. Given that the dividend is a cash outflow, we think that cash is more important than accounting measures of profit when assessing the dividend, so this is a mitigating factor.

Over the next year, EPS is forecast to grow rapidly. If the dividend continues along recent trends, we estimate the payout ratio could reach 240%, which is unsustainable.

EQT's Dividend Has Lacked Consistency

Even in its short history, we have seen the dividend cut. The annual payment during the last 4 years was €0.206 in 2020, and the most recent fiscal year payment was €0.306. This works out to be a compound annual growth rate (CAGR) of approximately 10% a year over that time. It is great to see strong growth in the dividend payments, but cuts are concerning as it may indicate the payout policy is too ambitious.

Dividend Growth May Be Hard To Come By

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. Over the past five years, it looks as though EQT's EPS has declined at around 9.6% a year. If the company is making less over time, it naturally follows that it will also have to pay out less in dividends. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this can turn into a longer term trend.

EQT's Dividend Doesn't Look Sustainable

In summary, while it's always good to see the dividend being raised, we don't think EQT's payments are rock solid. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Taking the debate a bit further, we've identified 3 warning signs for EQT that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if EQT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:EQT

EQT

A global private equity & venture capital firm specializing in private capital and real asset segments.

High growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|37.8% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor