Advertisement

- Sweden

- /

- Hospitality

- /

- OM:EVO

Why Evolution AB (publ) (STO:EVO) Could Be Worth Watching

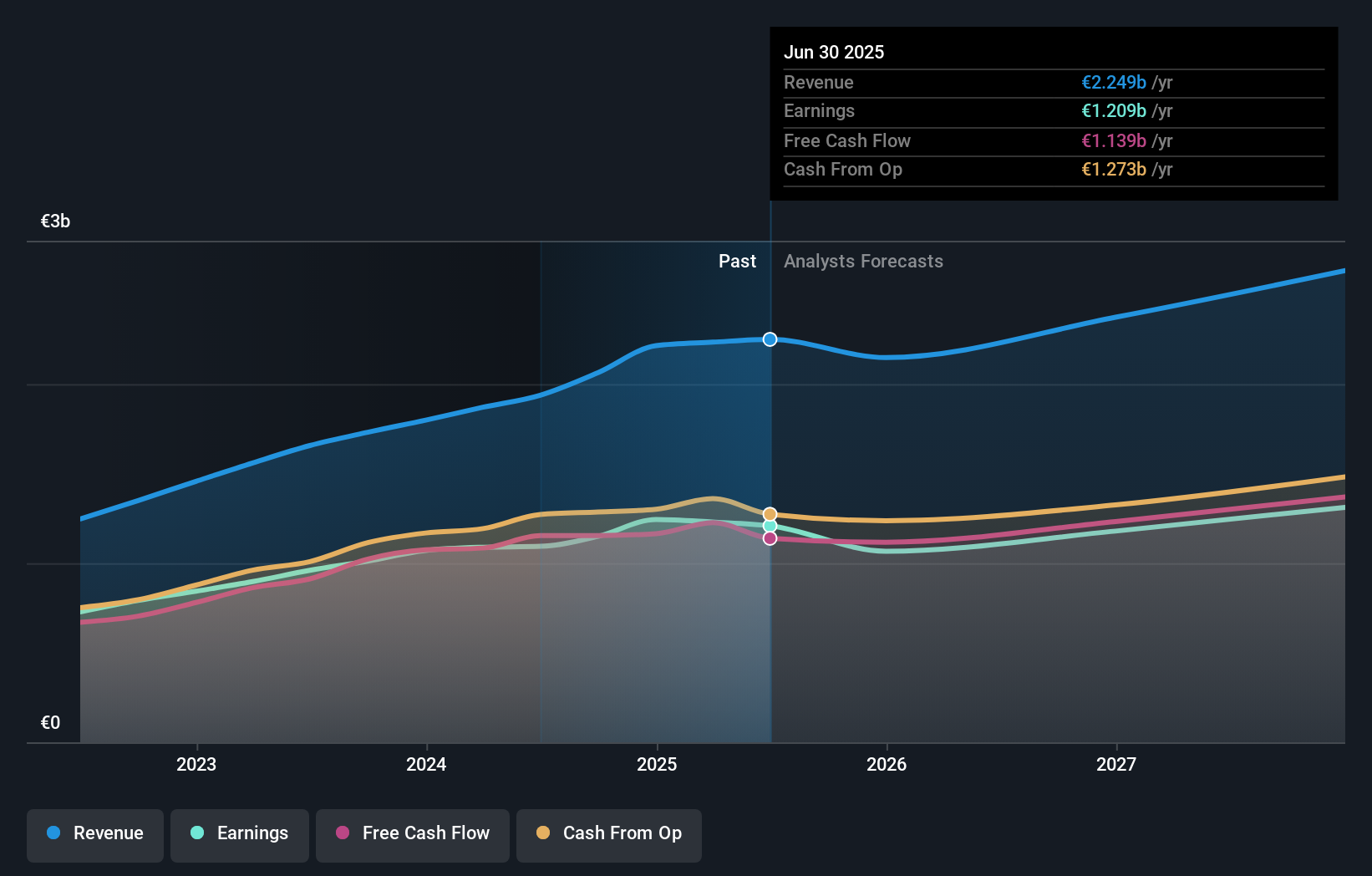

Let's talk about the popular Evolution AB (publ) (STO:EVO). The company's shares saw a significant share price rise of 23% in the past couple of months on the OM. The recent rally in share prices has nudged the company in the right direction, though it still falls short of its yearly peak. As a large-cap stock with high coverage by analysts, you could assume any recent changes in the company’s outlook is already priced into the stock. But what if there is still an opportunity to buy? Let’s take a look at Evolution’s outlook and value based on the most recent financial data to see if the opportunity still exists.

Is Evolution Still Cheap?

According to our price multiple model, which makes a comparison between the company's price-to-earnings ratio and the industry average, the stock price seems to be justfied. We’ve used the price-to-earnings ratio in this instance because there’s not enough visibility to forecast its cash flows. The stock’s ratio of 12.11x is currently trading slightly below its industry peers’ ratio of 12.11x, which means if you buy Evolution today, you’d be paying a decent price for it. And if you believe that Evolution should be trading at this level in the long run, then there’s not much of an upside to gain over and above other industry peers. Furthermore, it seems like Evolution’s share price is quite stable, which means there may be less chances to buy low in the future now that it’s priced similarly to industry peers. This is because the stock is less volatile than the wider market given its low beta.

See our latest analysis for Evolution

What does the future of Evolution look like?

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company's future expectations. Though in the case of Evolution, it is expected to deliver a relatively unexciting earnings growth of 8.8%, which doesn’t help build up its investment thesis. Growth doesn’t appear to be a main reason for a buy decision for the company, at least in the near term.

What This Means For You

Are you a shareholder? It seems like the market has already priced in EVO’s growth outlook, with shares trading around industry price multiples. However, there are also other important factors which we haven’t considered today, such as the track record of its management team. Have these factors changed since the last time you looked at EVO? Will you have enough conviction to buy should the price fluctuate below the industry PE ratio?

Are you a potential investor? If you’ve been keeping an eye on EVO, now may not be the most advantageous time to buy, given it is trading around industry price multiples. However, the positive growth outlook may mean it’s worth diving deeper into other factors in order to take advantage of the next price drop.

It can be quite valuable to consider what analysts expect for Evolution from their most recent forecasts. At Simply Wall St, we have the analysts estimates which you can view by clicking here.

If you are no longer interested in Evolution, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

Valuation is complex, but we're here to simplify it.

Discover if Evolution might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:EVO

Evolution

Develops, produces, markets, and licenses live casino and slots solutions to gaming operators in Europe, Asia, North America, Latin America, and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.559.3% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$4811.0% overvalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

29 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8212.9% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

BR

Bravosatya on Meta Platforms ·

Meta Platforms - Zuckerberg’s investment decisions are impulsive or Prudent?

Fair Value:US$730.0222.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JU

julio on FIGS ·

Figs valuation

Fair Value:US$14.3928.9% undervalued

20 followersusers have followed this narrative

6 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on MIRAI ·

Improving NOI growth visibility on wider rent gap

Fair Value:JP¥77.06k46.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75031.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.9% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.2% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative