Advertisement

Thule Group (OM:THULE) Margin Compression Challenges Bullish Earnings Growth Narratives

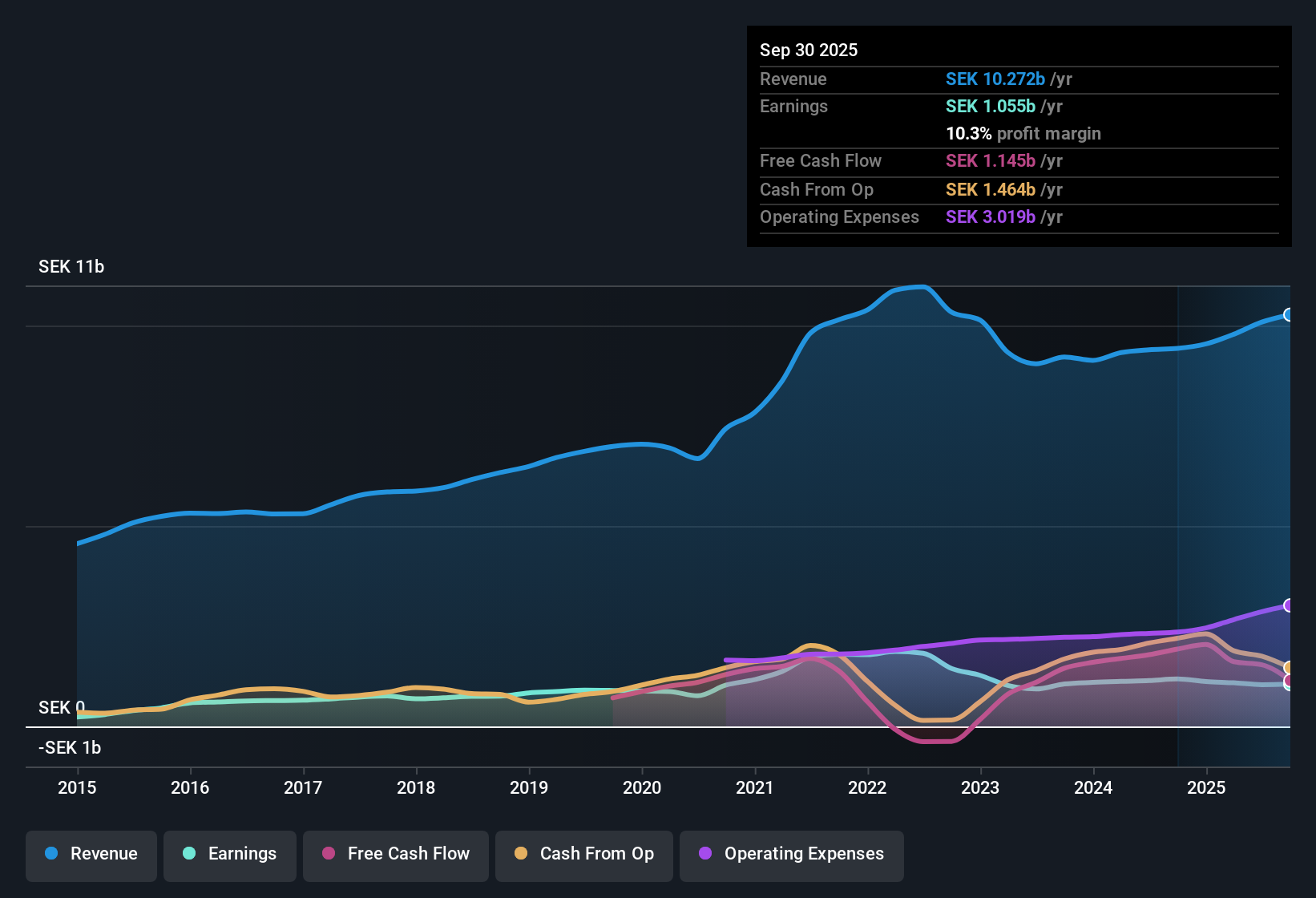

Thule Group FY 2025 Earnings Snapshot

Thule Group (OM:THULE) has wrapped up FY 2025 with Q4 revenue of SEK 1.8b and basic EPS of SEK 0.19, alongside trailing twelve month revenue of SEK 10.4b and EPS of SEK 10.33. The company reported quarterly revenue of SEK 2.7b in Q1 2025, SEK 3.4b in Q2, SEK 2.5b in Q3 and SEK 1.8b in Q4, while EPS over the same periods came in at SEK 2.47, SEK 4.75, SEK 2.91 and SEK 0.19. This provides context for investors assessing how margins have developed over the year.

See our full analysis for Thule Group.With the numbers on the table, the next step is to see how this earnings profile lines up with the prevailing narratives around Thule Group and where those stories get confirmed or questioned.

See what the community is saying about Thule Group

Margins Ease Back From 12.5% To 10.3%

- Over the last 12 months, Thule Group earned SEK 1,114 million on SEK 10.4b of revenue, which equates to a 10.3% net profit margin compared with 12.5% a year earlier.

- Analysts' consensus view sees product mix helping margins over time, and the current 10.3% margin gives a reference point for that claim.

- The consensus narrative points to a gross margin of 44.8% supported by higher margin products like Quad Lock and new launches, while the reported net margin at 10.3% shows that operating costs and other items are still taking a meaningful slice of profits.

- Consensus also highlights efforts to reduce inventory by SEK 200 million and drive supply chain efficiencies, and investors can watch whether those operational moves show up in a higher net margin versus the current 10.3% level.

Top Line Near SEK 10.4b, With Mixed Quarterly Pattern

- On a trailing basis, revenue came in at SEK 10.4b, built from quarterly sales that ranged from SEK 3,403 million in Q2 2025 to SEK 1,835 million in Q4 2025.

- Bulls argue that focused product categories and acquisitions could support revenue growth, and the current pattern gives some checks on that story.

- The consensus narrative talks about revenue growth potential from areas like bike carriers and North American pickup trucks, yet Q4 2025 revenue at SEK 1,835 million is only modestly above Q4 2024 at SEK 1,678 million, suggesting that any benefit from the new focus is not yet clearly visible in these year on year numbers.

- Analysts also reference ongoing new product launches winning design awards as a possible revenue driver, and investors can compare that optimism with the trailing 12 month revenue progression from SEK 9,541 million in Q4 2024 to SEK 10,429 million in Q4 2025 to see how much is already reflected.

Valuation Gap: P/E 25.3x vs DCF Fair Value

- The shares trade on a P/E of 25.3x against a DCF fair value of SEK 415.62 per share, while the current share price is SEK 238.40 and the allowed analyst price target is SEK 282.86.

- Bears focus on weaker recent earnings trends when they look at these valuation signals.

- Trailing earnings of SEK 1,114 million compare with a five year pattern where earnings declined on average by 8.3% per year, so some investors may question how quickly the business can grow into a DCF fair value of SEK 415.62 or an analyst target of SEK 282.86 from a share price of SEK 238.40.

- Critics also point out that net margin has eased from 12.5% to 10.3% over the last year and that debt is flagged as high in recent analysis, which can make a 25.3x P/E look demanding next to the European Leisure average of 23.5x even if it is lower than the 64.7x peer average.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Thule Group on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers differently? Take a couple of minutes to test your own thesis against this earnings story and shape it into a clear view, then Do it your way.

A great starting point for your Thule Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

See What Else Is Out There

Thule Group is operating with easing net margins, high debt and a 25.3x P/E that some investors view as demanding in light of recent earnings trends.

If that combination of pressured margins and higher leverage feels uncomfortable, you may want to compare it with solid balance sheet and fundamentals stocks screener (381 results) that emphasize financial strength and resilience.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Thule Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:THULE

Thule Group

Operates as a sports and outdoor company in Europe, North America, and internationally.

Good value average dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3078.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative