Advertisement

- Sweden

- /

- Consumer Durables

- /

- OM:PRFO

Profoto Holding (STO:PRFO) Has Announced That Its Dividend Will Be Reduced To SEK3.75

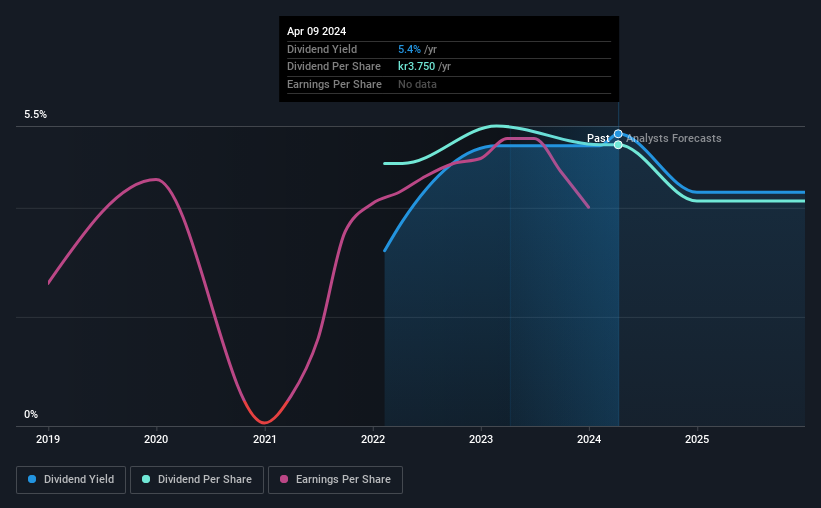

Profoto Holding AB (publ) (STO:PRFO) has announced that on 21st of May, it will be paying a dividend ofSEK3.75, which a reduction from last year's comparable dividend. This means the annual payment is 5.4% of the current stock price, which is above the average for the industry.

See our latest analysis for Profoto Holding

Profoto Holding's Dividend Is Well Covered By Earnings

If the payments aren't sustainable, a high yield for a few years won't matter that much. Before making this announcement, the company's dividend was much higher than its earnings. Without profits and cash flows increasing, it would be difficult for the company to continue paying the dividend at this level.

Over the next year, EPS is forecast to expand by 4.9%. If the dividend continues along recent trends, we estimate the payout ratio could reach 92%, which is on the higher side, but certainly still feasible.

Profoto Holding Doesn't Have A Long Payment History

Looking back, the dividend has been stable, but the company hasn't been paying a dividend for very long so we can't be confident that the dividend will remain stable through all economic environments. Since 2022, the annual payment back then was SEK3.50, compared to the most recent full-year payment of SEK3.75. This implies that the company grew its distributions at a yearly rate of about 3.5% over that duration. It's good to see at least some dividend growth. Yet with a relatively short dividend paying history, we wouldn't want to depend on this dividend too heavily.

Profoto Holding's Dividend Might Lack Growth

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. It's encouraging to see that Profoto Holding has been growing its earnings per share at 11% a year over the past five years. However, the payout ratio is very high, not leaving much room for growth of the dividend in the future.

Profoto Holding's Dividend Doesn't Look Sustainable

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. Strong earnings growth means Profoto Holding has the potential to be a good dividend stock in the future, despite the current payments being at elevated levels. This company is not in the top tier of income providing stocks.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. To that end, Profoto Holding has 2 warning signs (and 1 which can't be ignored) we think you should know about. Is Profoto Holding not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:PRFO

Profoto Holding

Provides lighting equipment for professional photographers, cinematographers, and studios in Sweden and internationally.

Undervalued with high growth potential.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor