Advertisement

- Sweden

- /

- Consumer Durables

- /

- OM:BONAV B

Analysts Have Made A Financial Statement On Bonava AB (publ)'s (STO:BONAV B) First-Quarter Report

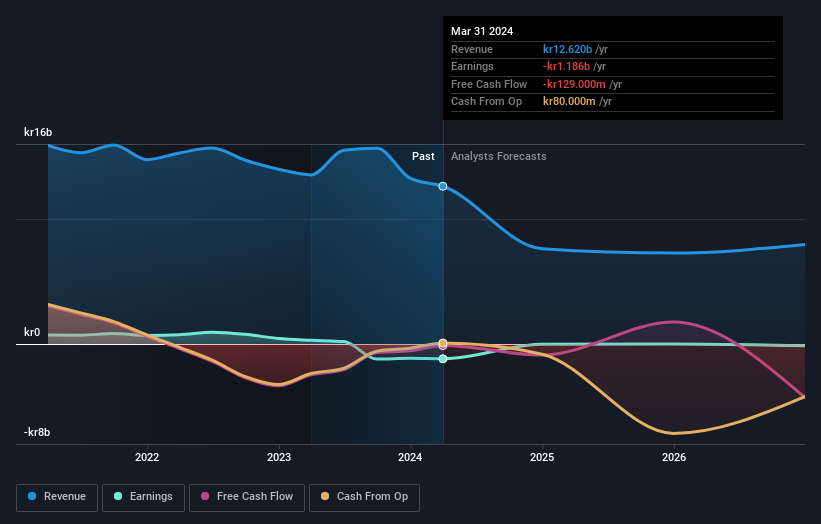

Bonava AB (publ) (STO:BONAV B) shareholders are probably feeling a little disappointed, since its shares fell 4.6% to kr10.07 in the week after its latest quarterly results. Revenues of kr1.3b beat expectations by a respectable 9.1%, although statutory losses per share increased. Bonava lost kr0.87, which was 185% more than what the analysts had included in their models. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

See our latest analysis for Bonava

After the latest results, the consensus from Bonava's three analysts is for revenues of kr7.63b in 2024, which would reflect a substantial 40% decline in revenue compared to the last year of performance. Per-share statutory losses are expected to explode, reaching kr0.077 per share. Yet prior to the latest earnings, the analysts had been anticipated revenues of kr7.40b and earnings per share (EPS) of kr0.22 in 2024. While they've upgraded their revenue numbers for next year, the consensus also expects losses to increase, perhaps due to the investments required to fund that growth In any event, it's not clear that these new estimates are particularly bullish.

The consensus price target stayed unchanged at kr17.25, seeming to suggest that higher forecast losses are not expected to have a long term impact on the valuation. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Bonava, with the most bullish analyst valuing it at kr25.00 and the most bearish at kr9.50 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. Over the past five years, revenues have declined around 2.5% annually. Worse, forecasts are essentially predicting the decline to accelerate, with the estimate for an annualised 49% decline in revenue until the end of 2024. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 1.1% per year. So while a broad number of companies are forecast to grow, unfortunately Bonava is expected to see its revenue affected worse than other companies in the industry.

The Bottom Line

The biggest low-light for us was that the forecasts for Bonava dropped from profits to a loss next year. Fortunately, they also upgraded their revenue estimates, although our data indicates it is expected to perform worse than the wider industry. The consensus price target held steady at kr17.25, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have forecasts for Bonava going out to 2026, and you can see them free on our platform here.

We don't want to rain on the parade too much, but we did also find 3 warning signs for Bonava that you need to be mindful of.

Valuation is complex, but we're here to simplify it.

Discover if Bonava might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:BONAV B

Bonava

Operates as a residential developer in Germany, Sweden, Finland, Norway, Estonia, Latvia, and Lithuania.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor