Advertisement

NCC AB (publ) (STO:NCC B) will pay a dividend of SEK3.00 on the 9th of November. This makes the dividend yield 6.5%, which will augment investor returns quite nicely.

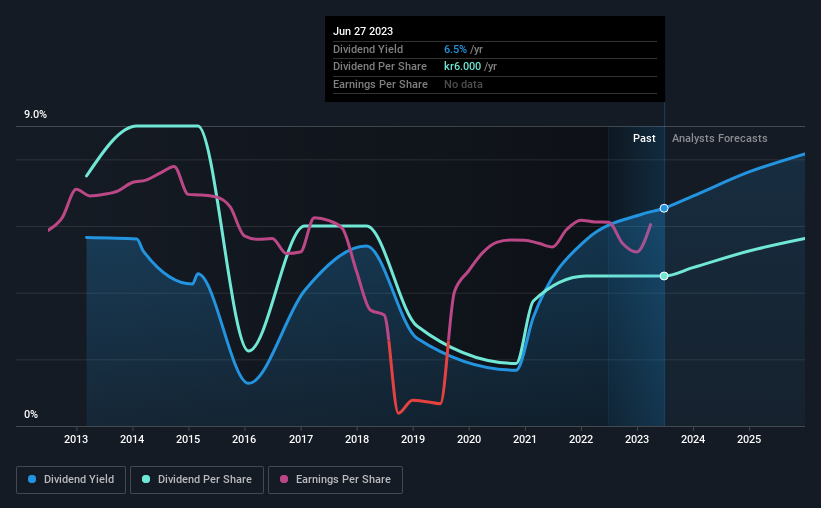

See our latest analysis for NCC

NCC's Earnings Easily Cover The Distributions

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Based on the last payment, NCC's earnings were much higher than the dividend, but it wasn't converting those earnings into cash flow. In general, we consider cash flow to be more important than earnings, so we would be cautious about relying on the sustainability of this dividend.

Over the next year, EPS is forecast to fall by 2.2%. If the dividend continues along recent trends, we estimate the payout ratio could be 36%, which we consider to be quite comfortable, with most of the company's earnings left over to grow the business in the future.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2013, the dividend has gone from SEK10.00 total annually to SEK6.00. Doing the maths, this is a decline of about 5.0% per year. Generally, we don't like to see a dividend that has been declining over time as this can degrade shareholders' returns and indicate that the company may be running into problems.

The Dividend Looks Likely To Grow

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. NCC has impressed us by growing EPS at 34% per year over the past five years. NCC is clearly able to grow rapidly while still returning cash to shareholders, positioning it to become a strong dividend payer in the future.

Our Thoughts On NCC's Dividend

In summary, while it's good to see that the dividend hasn't been cut, we are a bit cautious about NCC's payments, as there could be some issues with sustaining them into the future. With cash flows lacking, it is difficult to see how the company can sustain a dividend payment. We would be a touch cautious of relying on this stock primarily for the dividend income.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. To that end, NCC has 3 warning signs (and 2 which are a bit concerning) we think you should know about. Is NCC not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if NCC might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:NCC B

NCC

Operates as a construction company in Sweden, Norway, Denmark, and Finland.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor