Advertisement

- Sweden

- /

- Construction

- /

- OM:INSTAL

Instalco AB (publ) Just Missed Earnings - But Analysts Have Updated Their Models

Last week, you might have seen that Instalco AB (publ) (STO:INSTAL) released its second-quarter result to the market. The early response was not positive, with shares down 6.4% to kr48.02 in the past week. Revenues were in line with forecasts, at kr3.7b, although statutory earnings per share came in 15% below what the analysts expected, at kr0.47 per share. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Check out our latest analysis for Instalco

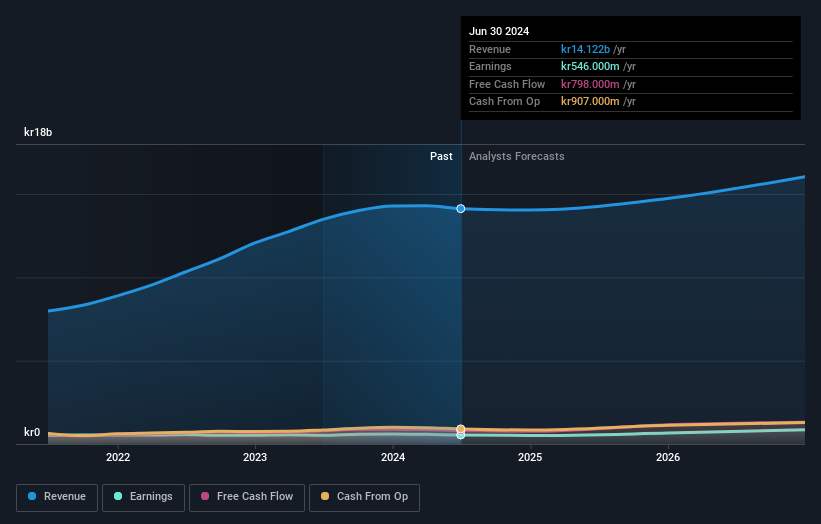

Taking into account the latest results, Instalco's four analysts currently expect revenues in 2024 to be kr14.0b, approximately in line with the last 12 months. Statutory earnings per share are expected to decrease 6.9% to kr1.93 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of kr14.0b and earnings per share (EPS) of kr1.99 in 2024. The analysts seem to have become a little more negative on the business after the latest results, given the small dip in their earnings per share numbers for next year.

The consensus price target held steady at kr52.25, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values Instalco at kr58.00 per share, while the most bearish prices it at kr40.00. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Instalco's past performance and to peers in the same industry. These estimates imply that revenue is expected to slow, with a forecast annualised decline of 1.2% by the end of 2024. This indicates a significant reduction from annual growth of 22% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 6.7% annually for the foreseeable future. It's pretty clear that Instalco's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting that it's tracking in line with expectations. Although our data does suggest that Instalco's revenue is expected to perform worse than the wider industry. The consensus price target held steady at kr52.25, with the latest estimates not enough to have an impact on their price targets.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Instalco going out to 2026, and you can see them free on our platform here..

Plus, you should also learn about the 1 warning sign we've spotted with Instalco .

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:INSTAL

Instalco

Provides installation services in the electrical, heating and plumbing, ventilation, technical consulting, and industrial areas in Sweden and rest of the Nordics.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|90.8% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|15.9% undervalued

MA

Community Contributor