Advertisement

European Equity Opportunities That May Be Undervalued In November 2025

Simply Wall St

Reviewed by Simply Wall St

As European markets grapple with concerns over inflated AI stock valuations and the impact of U.S. interest rate expectations, the pan-European STOXX Europe 600 Index has seen a decline, reflecting broader market unease. In this environment, identifying potentially undervalued stocks can be crucial for investors looking to capitalize on opportunities that may offer value amidst prevailing economic uncertainties.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Nokian Panimo Oyj (HLSE:BEER) | €2.45 | €4.88 | 49.8% |

| Mo-BRUK (WSE:MBR) | PLN306.50 | PLN599.59 | 48.9% |

| Micro Systemation (OM:MSAB B) | SEK65.00 | SEK127.47 | 49% |

| Kitron (OB:KIT) | NOK59.25 | NOK116.55 | 49.2% |

| HMS Bergbau (XTRA:HMU) | €52.50 | €103.54 | 49.3% |

| Esautomotion (BIT:ESAU) | €3.12 | €6.10 | 48.8% |

| Elekta (OM:EKTA B) | SEK58.50 | SEK114.24 | 48.8% |

| EcoUp Oyj (HLSE:ECOUP) | €1.34 | €2.64 | 49.2% |

| B&S Group (ENXTAM:BSGR) | €5.94 | €11.83 | 49.8% |

| Allcore (BIT:CORE) | €1.355 | €2.65 | 48.8% |

Let's explore several standout options from the results in the screener.

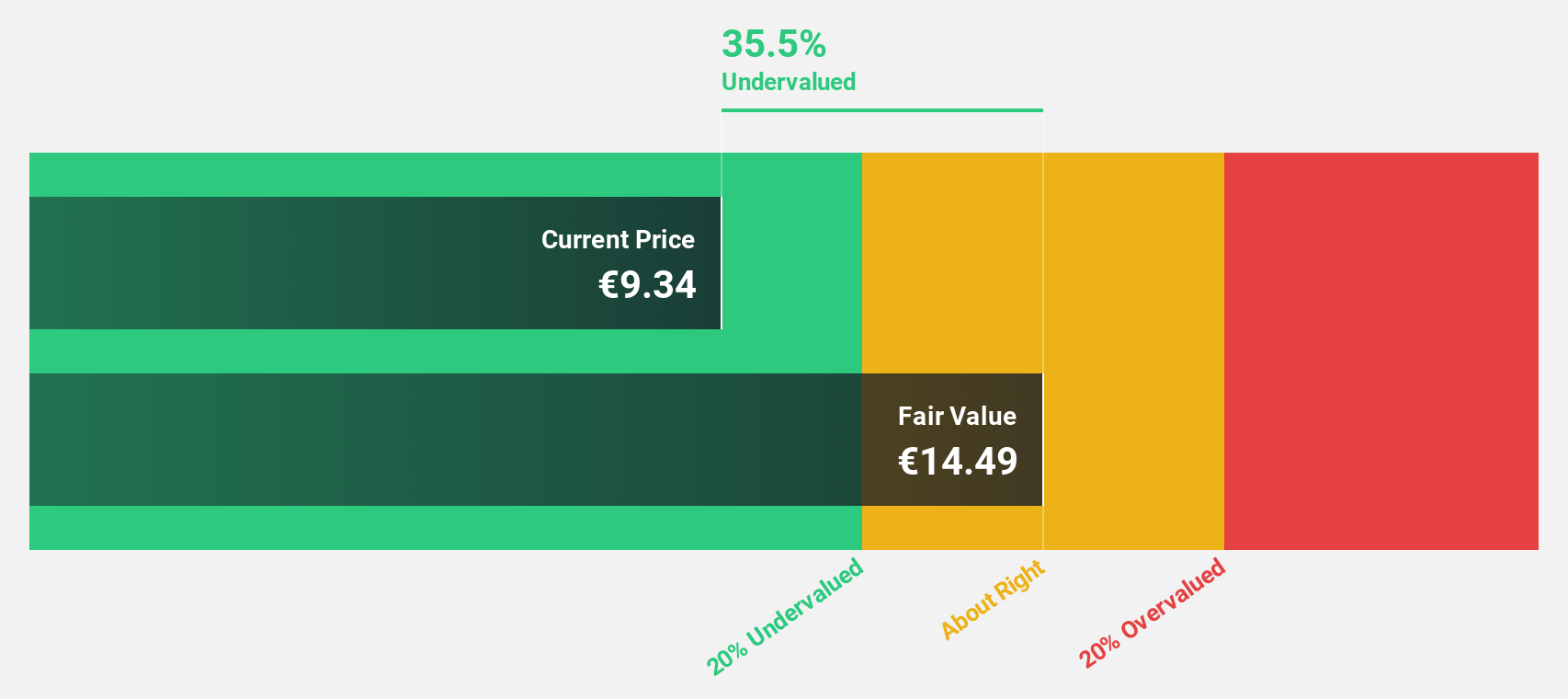

BFF Bank (BIT:BFF)

Overview: BFF Bank S.p.A. operates in non-recourse factoring and credit management for public administration bodies and private hospitals across several European countries, with a market cap of €2.06 billion.

Operations: The company generates revenue of €397.58 million from its financial services in the commercial sector.

Estimated Discount To Fair Value: 20.2%

BFF Bank is trading at €10.91, below its estimated fair value of €13.68, indicating potential undervaluation based on cash flows. The bank's earnings are expected to grow annually by 17.1%, outpacing the Italian market's growth rate of 9.9%. Despite a high return on equity forecasted at 26.5% in three years and revenue growth surpassing the Italian market, challenges include a high debt level and an unstable dividend history, with profit margins declining from last year.

- According our earnings growth report, there's an indication that BFF Bank might be ready to expand.

- Click to explore a detailed breakdown of our findings in BFF Bank's balance sheet health report.

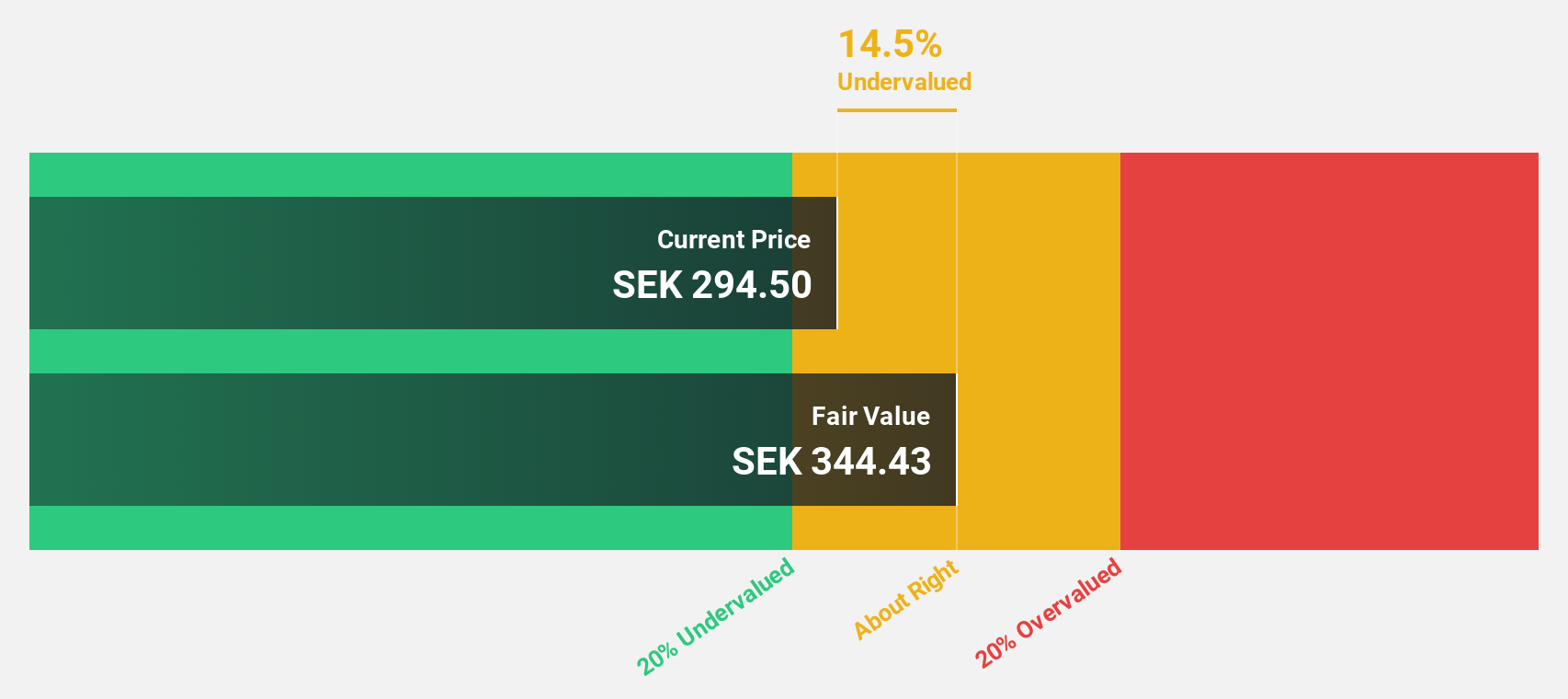

Beijer Alma (OM:BEIA B)

Overview: Beijer Alma AB (publ) operates in component manufacturing and industrial trading across Sweden, the Nordic region, Europe, North America, Asia, and internationally with a market cap of SEK16.87 billion.

Operations: The company's revenue segments include Lesjöfors, generating SEK5.08 billion, and Beijer Tech, contributing SEK2.62 billion.

Estimated Discount To Fair Value: 15%

Beijer Alma is trading at SEK280, 15% below its estimated fair value of SEK329.4, suggesting undervaluation based on cash flows. Earnings are projected to grow significantly at 23.6% annually, outpacing the Swedish market's growth rate of 13.5%. However, challenges include a decline in profit margins from last year and high debt levels. Recent earnings reports show increased sales but decreased net income and earnings per share compared to the previous year.

- Our comprehensive growth report raises the possibility that Beijer Alma is poised for substantial financial growth.

- Get an in-depth perspective on Beijer Alma's balance sheet by reading our health report here.

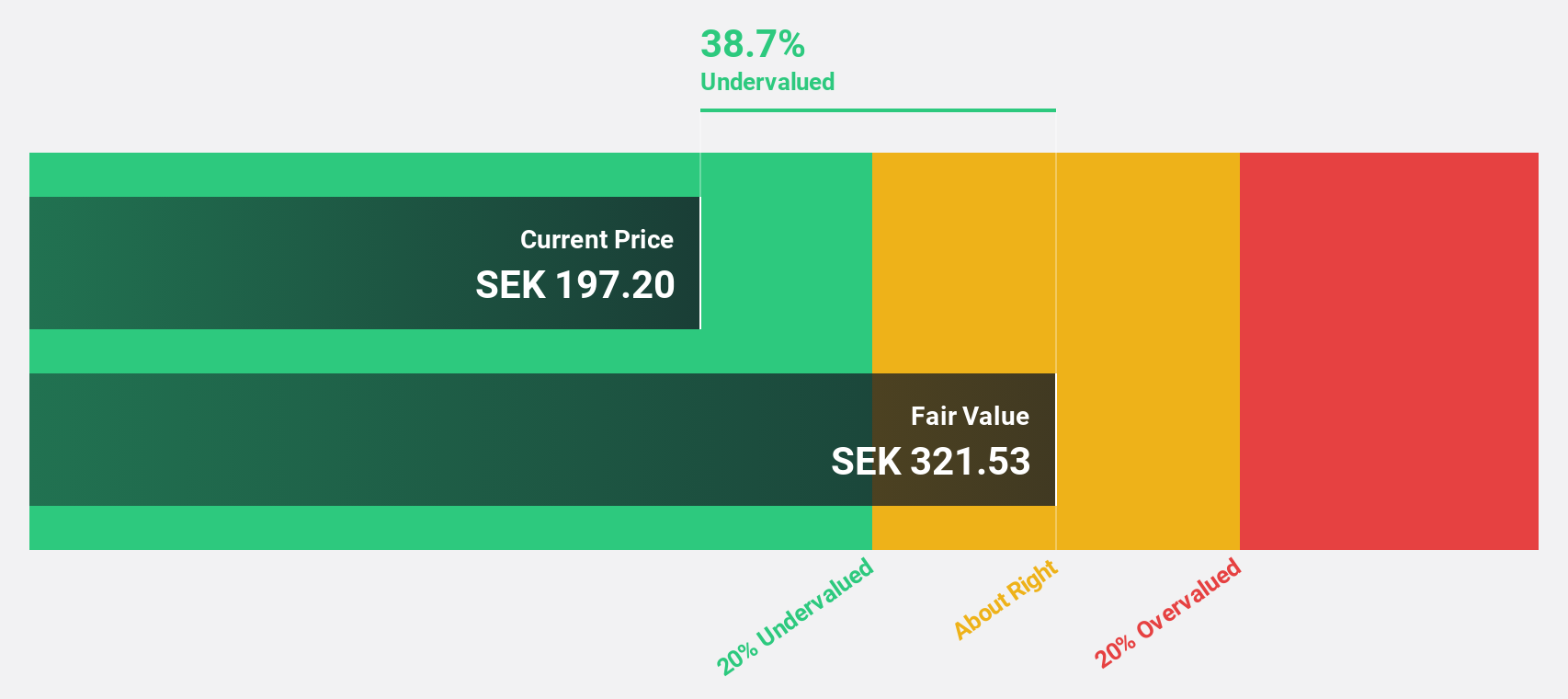

MilDef Group (OM:MILDEF)

Overview: MilDef Group AB (publ) develops, manufactures, and sells rugged IT solutions across several countries including Sweden, Norway, and the United States, with a market cap of SEK6.45 billion.

Operations: The company's revenue is primarily derived from its Computer Hardware segment, which generated SEK1.68 billion.

Estimated Discount To Fair Value: 38.5%

MilDef Group is trading at SEK136.9, significantly below its estimated fair value of SEK222.55, highlighting potential undervaluation based on cash flows. Recent earnings reports show a substantial increase in sales and net income compared to the previous year, with sales reaching SEK 539.7 million for Q3 2025. The company is expanding capacity with a new facility in Rosersberg and has secured major contracts, including a SEK 320 million order under a long-term NATO agreement.

- Insights from our recent growth report point to a promising forecast for MilDef Group's business outlook.

- Click here to discover the nuances of MilDef Group with our detailed financial health report.

Summing It All Up

- Gain an insight into the universe of 200 Undervalued European Stocks Based On Cash Flows by clicking here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Beijer Alma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:BEIA B

Beijer Alma

Engages in component manufacturing and industrial trading businesses in Sweden, rest of Nordic Region, rest of Europe, North America, Asia, and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$120.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k1.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative