Advertisement

- Sweden

- /

- Trade Distributors

- /

- OM:BEGR

BE Group AB (publ) Just Missed EPS By 19%: Here's What Analysts Think Will Happen Next

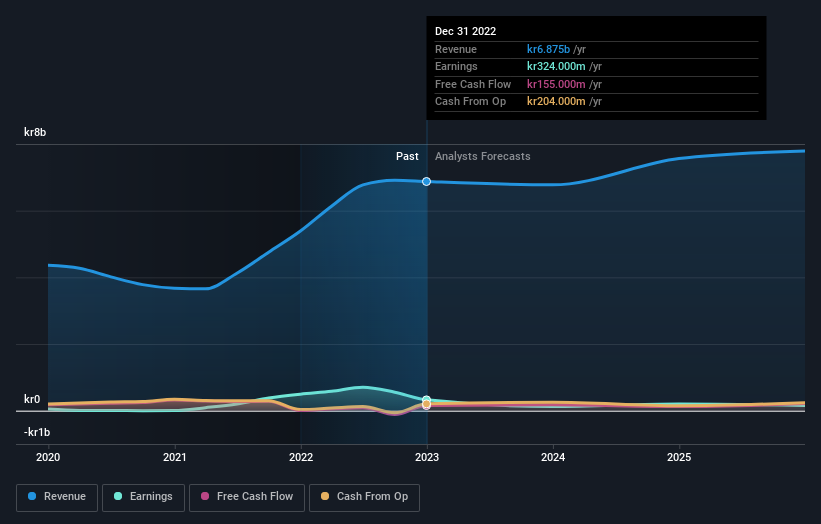

Last week saw the newest full-year earnings release from BE Group AB (publ) (STO:BEGR), an important milestone in the company's journey to build a stronger business. It was not a great result overall. While revenues of kr6.9b were in line with analyst predictions, earnings were less than expected, missing statutory estimates by 19% to hit kr24.96 per share. Following the result, the analyst has updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we collected the latest post-earnings statutory consensus estimate to see what could be in store for next year.

See our latest analysis for BE Group

Following last week's earnings report, BE Group's sole analyst are forecasting 2023 revenues to be kr6.77b, approximately in line with the last 12 months. Statutory earnings per share are expected to nosedive 61% to kr9.79 in the same period. In the lead-up to this report, the analyst had been modelling revenues of kr6.74b and earnings per share (EPS) of kr13.60 in 2023. The analyst seem to have become more bearish following the latest results. While there were no changes to revenue forecasts, there was a large cut to EPS estimates.

It might be a surprise to learn that the consensus price target was broadly unchanged at kr119, with the analyst clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the BE Group's past performance and to peers in the same industry. We would highlight that sales are expected to reverse, with a forecast 1.5% annualised revenue decline to the end of 2023. That is a notable change from historical growth of 7.7% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 3.8% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - BE Group is expected to lag the wider industry.

The Bottom Line

The biggest concern is that the analyst reduced their earnings per share estimates, suggesting business headwinds could lay ahead for BE Group. On the plus side, there were no major changes to revenue estimates; although forecasts imply revenues will perform worse than the wider industry. The consensus price target held steady at kr119, with the latest estimates not enough to have an impact on their price target.

With that in mind, we wouldn't be too quick to come to a conclusion on BE Group. Long-term earnings power is much more important than next year's profits. We have analyst estimates for BE Group going out as far as 2025, and you can see them free on our platform here.

You should always think about risks though. Case in point, we've spotted 3 warning signs for BE Group you should be aware of, and 1 of them is a bit unpleasant.

Valuation is complex, but we're here to simplify it.

Discover if BE Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OM:BEGR

BE Group

Operates as a trading and service company in steel, stainless steel, and aluminum products in Sweden, Poland, Finland, and Baltics.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor