- Hong Kong

- /

- Medical Equipment

- /

- SEHK:2190

3 Growth Companies With Insider Ownership Up To 25%

Reviewed by Simply Wall St

In a week marked by busy earnings reports and mixed economic signals, global markets have shown varied performances, with major indices like the Nasdaq Composite and S&P MidCap 400 reaching record highs before retreating. Amidst these fluctuations, growth stocks lagged behind value shares, reflecting cautious sentiment from key technology companies' earnings. In such an environment, identifying growth companies with substantial insider ownership can be appealing to investors seeking alignment between management interests and shareholder value. This article will explore three growth companies where insiders hold up to 25% ownership, potentially offering insights into their commitment to long-term success.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 21.5% |

| Medley (TSE:4480) | 34% | 30.4% |

| Pharma Mar (BME:PHM) | 11.8% | 56.4% |

| Findi (ASX:FND) | 34.8% | 64.8% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

| Alkami Technology (NasdaqGS:ALKT) | 11.2% | 98.6% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Brightstar Resources (ASX:BTR) | 14.8% | 84.6% |

Let's explore several standout options from the results in the screener.

Pricol (NSEI:PRICOLLTD)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Pricol Limited, along with its subsidiaries, manufactures and sells instrument clusters and other automobile components to original equipment manufacturers and replacement markets both in India and internationally, with a market cap of ₹58.16 billion.

Operations: Revenue Segments (in millions of ₹): Instrument Clusters: 8,500; Sensors & Actuators: 3,200; Pumps & Mechanical Products: 4,700; Telematics & Connected Vehicles: 2,600.

Insider Ownership: 25.5%

Pricol Limited demonstrates potential as a growth company with strong insider ownership, driven by expected earnings growth of 24.6% annually over the next three years, outpacing the Indian market. Recent earnings show robust performance with significant year-over-year increases in sales and net income. The company's strategic focus on inorganic growth through acquisitions and its expansion in the four-wheeler segment contribute to its promising outlook, supported by a solid order book and ongoing product development initiatives.

- Click to explore a detailed breakdown of our findings in Pricol's earnings growth report.

- According our valuation report, there's an indication that Pricol's share price might be on the expensive side.

Fawaz Abdulaziz Al Hokair (SASE:4240)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Fawaz Abdulaziz Al Hokair & Company operates as a franchise retailer of fashion products across several countries, including Saudi Arabia and the United States, with a market capitalization of SAR1.47 billion.

Operations: The company's revenue segments include Fashion Retail at SAR4.64 billion, F&B at SAR359.85 million, and Indoor Entertainment at SAR69.75 million.

Insider Ownership: 15.2%

Fawaz Abdulaziz Al Hokair & Company faces challenges with negative shareholders' equity and high debt levels, yet it trades at a good value relative to peers. Despite volatile share prices, earnings are forecast to grow significantly at 114.7% annually, surpassing market expectations for profitability within three years. The recent CEO appointment of Salim Fakhouri could bring strategic direction given his extensive regional experience in fashion retail across the Middle East and North Africa.

- Dive into the specifics of Fawaz Abdulaziz Al Hokair here with our thorough growth forecast report.

- Our valuation report here indicates Fawaz Abdulaziz Al Hokair may be undervalued.

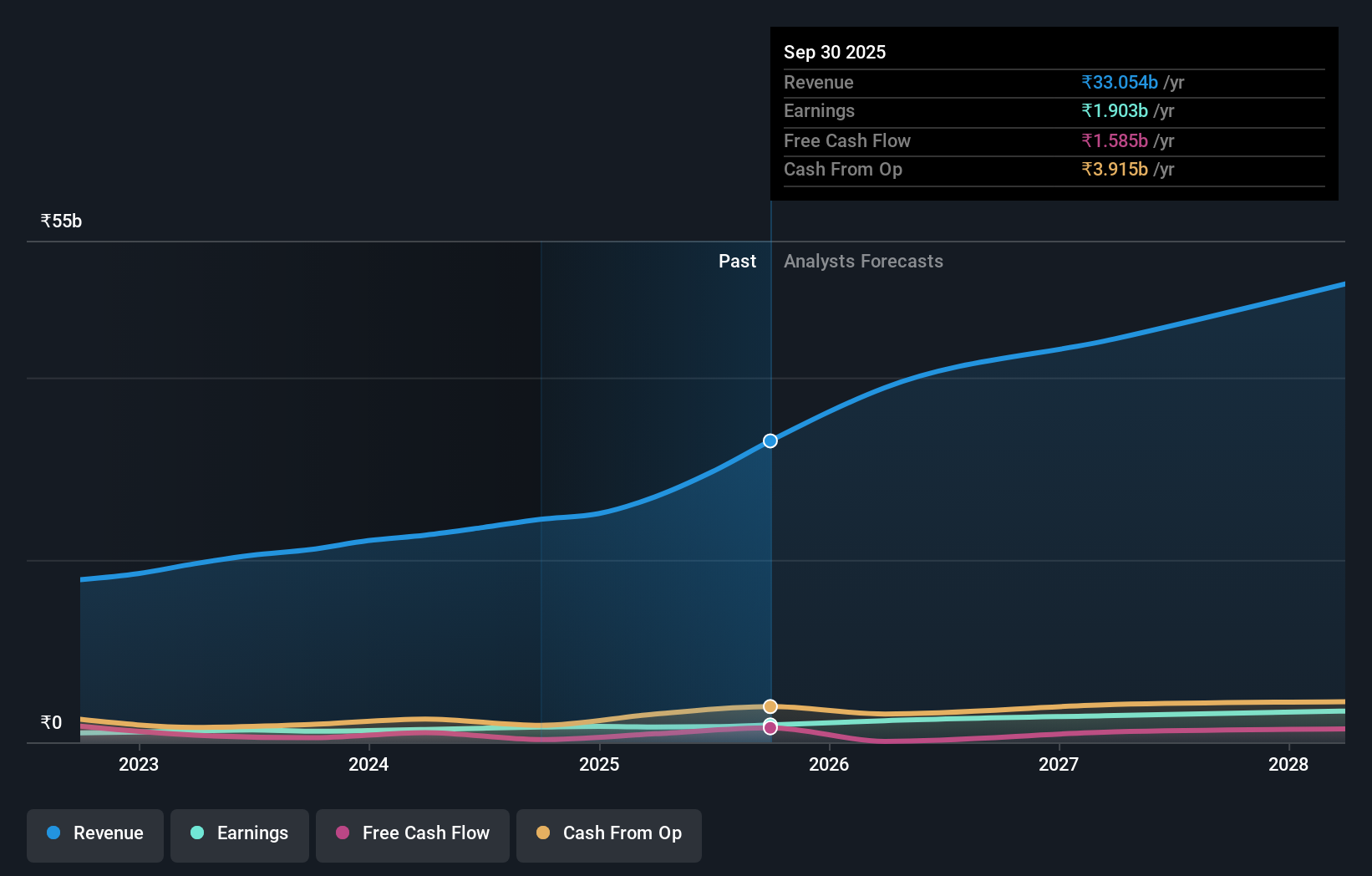

Zylox-Tonbridge Medical Technology (SEHK:2190)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zylox-Tonbridge Medical Technology Co., Ltd. is a medical device company that offers neuro- and peripheral-vascular interventional devices in the People's Republic of China and internationally, with a market cap of HK$3.48 billion.

Operations: The company generates revenue of CN¥663.61 million from the sale of interventional surgical devices for neurovascular and peripheral-vascular applications.

Insider Ownership: 18.8%

Zylox-Tonbridge Medical Technology is positioned for significant growth, with earnings expected to increase by 69.8% annually, outpacing the Hong Kong market. Revenue growth is also projected at 23.8% per year. The company recently became profitable and trades well below its estimated fair value, suggesting potential upside. A share buyback program aims to enhance net assets and earnings per share, reflecting confidence in future performance despite a forecasted low return on equity of 6.6%.

- Take a closer look at Zylox-Tonbridge Medical Technology's potential here in our earnings growth report.

- The valuation report we've compiled suggests that Zylox-Tonbridge Medical Technology's current price could be quite moderate.

Next Steps

- Take a closer look at our Fast Growing Companies With High Insider Ownership list of 1537 companies by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade Zylox-Tonbridge Medical Technology, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Zylox-Tonbridge Medical Technology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2190

Zylox-Tonbridge Medical Technology

A medical device company, provides neuro- and peripheral-vascular interventional medical devices the People’s Republic of China and internationally.

Flawless balance sheet with high growth potential.

Market Insights

Community Narratives