Advertisement

- Saudi Arabia

- /

- Real Estate

- /

- SASE:4323

We Think Sumou Real Estate's (TADAWUL:4323) Solid Earnings Are Understated

Despite posting healthy earnings, Sumou Real Estate Company's (TADAWUL:4323 ) stock has been quite weak. Along with the solid headline numbers, we think that investors have some reasons for optimism.

See our latest analysis for Sumou Real Estate

Zooming In On Sumou Real Estate's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

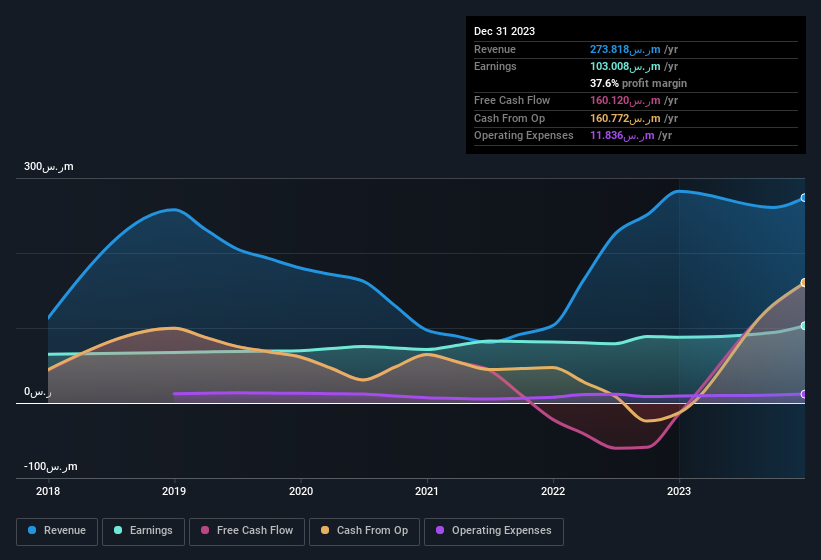

Over the twelve months to December 2023, Sumou Real Estate recorded an accrual ratio of -0.13. Therefore, its statutory earnings were quite a lot less than its free cashflow. Indeed, in the last twelve months it reported free cash flow of ر.س160m, well over the ر.س103.0m it reported in profit. Given that Sumou Real Estate had negative free cash flow in the prior corresponding period, the trailing twelve month resul of ر.س160m would seem to be a step in the right direction.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Sumou Real Estate.

Our Take On Sumou Real Estate's Profit Performance

As we discussed above, Sumou Real Estate has perfectly satisfactory free cash flow relative to profit. Because of this, we think Sumou Real Estate's earnings potential is at least as good as it seems, and maybe even better! And on top of that, its earnings per share have grown at 44% per year over the last three years. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. So while earnings quality is important, it's equally important to consider the risks facing Sumou Real Estate at this point in time. Every company has risks, and we've spotted 2 warning signs for Sumou Real Estate you should know about.

This note has only looked at a single factor that sheds light on the nature of Sumou Real Estate's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:4323

Sumou Real Estate

Engages in the construction of residential and non-residential properties in Saudi Arabia.

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor