- Saudi Arabia

- /

- Media

- /

- SASE:4071

Arabian Contracting Services Company's (TADAWUL:4071) Share Price Could Signal Some Risk

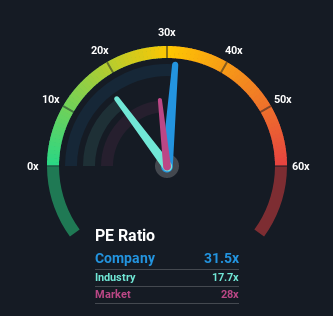

With a price-to-earnings (or "P/E") ratio of 31.5x Arabian Contracting Services Company (TADAWUL:4071) may be sending bearish signals at the moment, given that almost half of all companies in Saudi Arabia have P/E ratios under 27x and even P/E's lower than 19x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's lofty.

Recent times have been quite advantageous for Arabian Contracting Services as its earnings have been rising very briskly. It seems that many are expecting the strong earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

View our latest analysis for Arabian Contracting Services

How Is Arabian Contracting Services' Growth Trending?

In order to justify its P/E ratio, Arabian Contracting Services would need to produce impressive growth in excess of the market.

If we review the last year of earnings growth, the company posted a terrific increase of 141%. The latest three year period has also seen an excellent 44% overall rise in EPS, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 16% shows it's noticeably less attractive on an annualised basis.

With this information, we find it concerning that Arabian Contracting Services is trading at a P/E higher than the market. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with recent growth rates.

What We Can Learn From Arabian Contracting Services' P/E?

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Arabian Contracting Services currently trades on a much higher than expected P/E since its recent three-year growth is lower than the wider market forecast. Right now we are increasingly uncomfortable with the high P/E as this earnings performance isn't likely to support such positive sentiment for long. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Having said that, be aware Arabian Contracting Services is showing 2 warning signs in our investment analysis, and 1 of those shouldn't be ignored.

Of course, you might also be able to find a better stock than Arabian Contracting Services. So you may wish to see this free collection of other companies that sit on P/E's below 20x and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:4071

Arabian Contracting Services

Engages in printing business in Saudi Arabia.

Exceptional growth potential and fair value.

Market Insights

Community Narratives